Oct 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The harder life is for a man when he is young, the easier it will be in the future.” – Aleksandr I. Solzhenitsyn

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After across-the-board declines yesterday, futures are looking to regroup this morning as the S&P 500 and Nasdaq are both on pace to open higher by about 0.2%. Treasury yields are modestly higher, and gold went through 4,000 like a hot knife through butter. Along with the increase in gold, other precious metals are also up even more, with platinum spiking over 2% while Palladium is up 4.5%! Even crude oil is trading higher this morning as WTI gains 1.5% to $62.70 per barrel. Finally, after a rough day in the crypto space yesterday, Bitcoin is up 1% while Ethereum is marginally higher at just under $4,500.

In Asia, China remains closed, but Japan, Hong Kong, and India are all lower after Japan’s October Tankan Index declined relative to September. In Europe, the tone is much more positive with the STOXX 600 rallying 0.7% and broad-based strength across the continent. In Germany, Industrial Production declined 4.3% m/m in August versus forecasts for a drop of just 1.0%, so whatever you think about growth in the US, Europe isn’t doing much better.

Sometimes the market moves just because investors are looking for an excuse to buy or sell. Yesterday could have been a case of the latter. The S&P 500 headed into yesterday with seven days in a row of gains, while the Nasdaq traded higher in six of the prior seven days, but those streaks didn’t even begin to illustrate how hot some sectors of the market have become, and you can’t fault investors for getting a little nervous. In fact, it’s very encouraging! Just as the quote above says, a little pain is good for the soul.

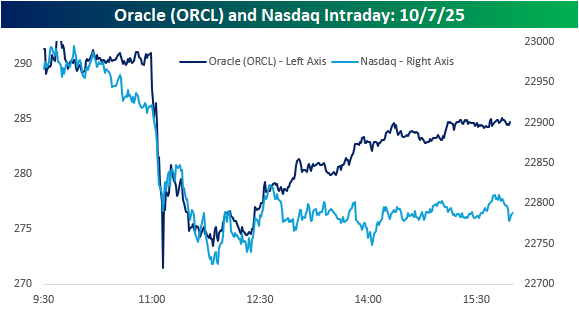

With investors already nervous, a report from The Information suggesting that margins in Oracle’s (ORCL) cloud business were thinner than expected was just the excuse they needed to take some profits. The report suggested that gross margins on the $900 million in revenue that the company generated from its Nvidia (NVDA) cloud business were just 14%, which is less than a quarter of the company’s overall gross margin of 70%.

Within minutes of the story being published, ORCL shares plunged 7% and the Nasdaq traded down over 1%. As shown in the chart below, while the magnitude of their respective moves after the report was published were different, the patterns were basically identical. Within 90 minutes, though, shares of ORCL started to rebound as “sources familiar with the situation” said The Information article was off base. By the end of the day, shares had erased more than half of their initial decline, finishing the day down 2.5%. The Nasdaq, however, didn’t bounce. While the declines didn’t intensify in the afternoon, the index finished right near where it traded after the initial release of the ORCL story.

There are multiple ways to read the divergence between ORCL and the Nasdaq intraday yesterday, and they could all be wrong. But one way to look at it is that investors looking for an excuse to take profits got just what they needed with the ORCL story, and once they rang the register, they were in no hurry to get back in. As the saying goes, “Nobody ever lost money taking a profit.”

Oct 7, 2025

This content is for members only

Oct 7, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We learn from history that we don’t learn from history!” – Desmond Tutu

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s not a lot going on in the futures market this morning, and once again, it will be another day without any economic data as the government remains closed. At this point, very few people have been affected by the shutdown, but as paydays come and go, the switchboards in DC will start heating up.

While there’s no economic data on the calendar, plenty of Fed officials are likely to speak, including Fed governors Bowman and Miran as well as Atlanta Fed President Bostic and Minneapolis Fed President Kashkari. The next Fed meeting is just three weeks away, and markets currently expect a 93% chance of another 25 basis point rate cut.

In Asian markets overnight, it was a quiet session. China and South Korea were closed while Japan finished marginally higher after trading up over 1% earlier in the session. The Yen weakened against the dollar again following the weekend election results as the likelihood of rate hikes declines, although a 30-year auction with a relatively high bid-to-cover ratio calmed some investor nerves.

European stocks are trading higher but by modest amounts, with the STOXX 600 trading up 0.2% with Italy (+0.6%) and France (+0.4%) leading the gains. German stocks aren’t performing as well following an unexpected decline in August Factory Orders (-0.8% vs 1.2%).

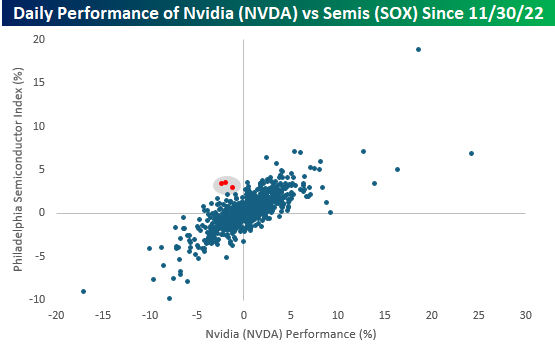

If you just looked at the performance of Nvidia (NVDA), which fell 1.1% yesterday, you probably would have thought semis had a bad day as well. You would have thought wrong. While NVDA was down, the Philadelphia Semiconductor Index (SOX) finished up 2.9%, and 24 of the index’s 30 components finished higher on the day. The scatter chart below compares the performance of NVDA (x-axis) to the SOX on every day since the launch of ChatGPT on 11/30/22, and during these 714 trading days, there have only been three where the SOX was up over 2.5% and NVDA traded down at least 1% on the day. In the post ChatGPT world, the SOX usually doesn’t rally without NVDA.

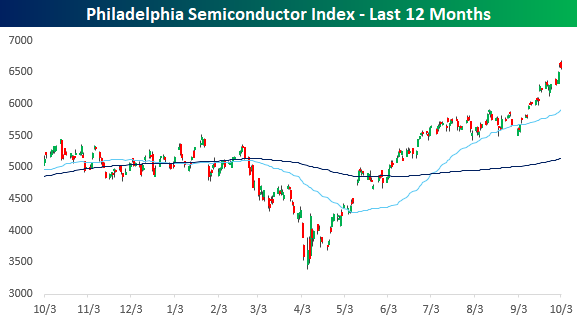

Given the broad strength in semis yesterday, the SOX continued it’s breakout from the summer consolidation and rallied to new highs yesterday. In the process, its price is now higher than the price of the S&P 500, something that only happened on a handful of other days back in 2004.

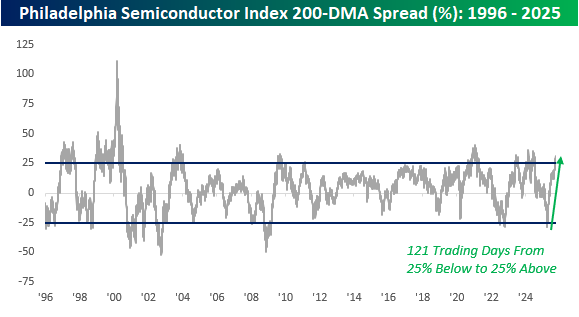

After yesterday’s rally, the SOX is now more than 31% above its 200-DMA. While that’s not unheard of for a volatile index like the SOX, the move from extreme oversold in April to extreme overbought now has been swift. In the span of 121 trading days, the SOX went from more than 25% below its 200-DMA to more than 25% above it. These kinds of reversals in the index have been uncommon.

Oct 6, 2025

Japanese stocks surged over 4% to start the week after Sanae Takaichi was elected to lead Japan’s ruling party, positioning her to become the country’s first female prime minister. Last night’s rally propelled the Nikkei above 46,000 for the first time and extended the rally from the April lows to more than 56%!

The 4% gain in the Nikkei, however, is somewhat misleading, particularly for US investors. This is because Takaichi is seen as a fiscal dove; she once called recent Bank of Japan (BoJ) rate hikes “stupid,” and one of her advisers has publicly stated the BoJ shouldn’t raise rates this fall. Given her preference for expansionist monetary policy, the Yen plunged nearly 2% against the dollar immediately following the news. As a result, the Nikkei’s 4% gain in nominal terms is nearly cut in half on a dollar-adjusted basis. Still, even a 2% rally is impressive!

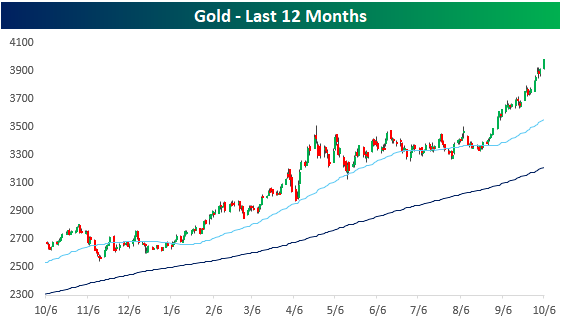

With one of the world’s five largest economies now being led by a noted fiscal dove who favors easy monetary policy and expanded government spending, investors concerned about profligacy are flocking to gold, continuing the massive breakout from its period of summer consolidation. As of early Monday afternoon trading, gold was less than 1% from crossing $4,000 for the first time.

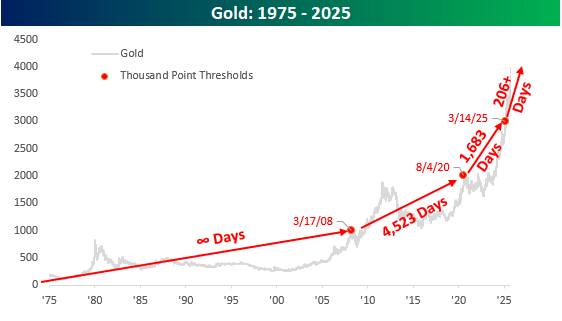

The chart below shows gold’s long-term performance, noting the first time it closed above each thousand-point threshold. While every thousand points represents a smaller percentage gain relative to gold’s overall price, it’s still worth highlighting how each one has been crossed in closer proximity to the last. It took infinity days for gold to first close above $1,000. The next thousand took 4,523 days, and then it took less than half that time to first cross $3,000. Now, less than seven months later, here comes $4,000. Simple math says that each subsequent thousand-point threshold will be crossed more quickly, and the more that governments around the world take a “buy now, pay later” approach to governing, the faster each domino will fall by the wayside.

Oct 6, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A minute’s success pays the failure of years.” – Robert Browning

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If futures are any indication, today would be the S&P 500’s seventh straight day of gains as positive international markets, M&A news, and the government shutdown continue to provide an upside lift to equities. Overnight, the Nikkei rallied more than 4.7% for its best day since April after the election of Takaichi as the new leader of the LDP. Takaichi is a noted dove, and her advisers have already come out against a fall rate hike by the BoJ. The rally in Japanese stocks has been accompanied by rising yields and a weak yen, so despite the big gain on a nominal basis, the EWJ ETF is only up a bit more than 1%.

In Europe, the tone isn’t as positive, but the STOXX 600 is still in positive territory with a gain of 0.1%. At the country level, Germany and the UK are higher, while France, Italy, and Spain are all lower. France is notably weak, with a decline of 1.3% as PM Lecornu resigned, continuing the trend of political turmoil in the country.

Getting back to the US, the data calendar is light today and for the remainder of the week (with or without a shutdown), and earnings season won’t really start until next week, although we’ll hear from Constellation Brands (STZ) after the close today and then Delta (DAL) and Pepsi (PEP) on Thursday.

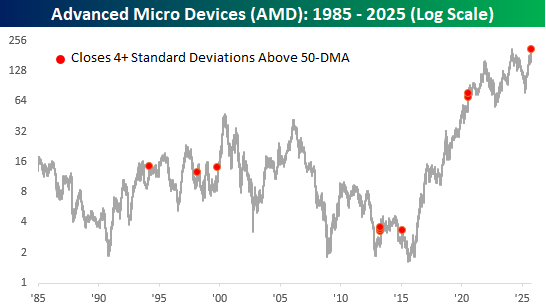

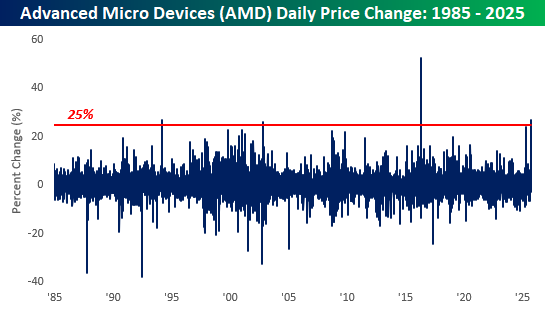

Shares of Advanced Micro Devices (AMD) are on pace to trade more than 25% higher this morning on news of its chip supply deal and equity investment with OpenAI. If AMD manages to finish the day with a gain of 27% or more (a percentage level it has reached throughout the morning), it will rank as the second-largest one-day gain for the stock since at least 1985.

With today’s gain, shares of AMD will also be trading at “extremely extreme” overbought levels. Over the last 45 years, there have only been a handful of other days when the stock traded four or more standard deviations above its 50-DMA, and if the stock holds onto these gains throughout the trading session, today would be another one.