Aug 29, 2025

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium.

August has recently been a month where negative surprises have a way of interrupting market rallies. This August that wasn’t the case, although it wasn’t for lack of trying on the part of the market gods. Between the trade issues, the tail end of earnings season where reports tend to get weaker, higher inflation readings, the Fed’s Jackson Hole conference, or this week’s attempted firing of Fed Governor Lisa Cook, any of these events could have sparked a volatility fit, but the longer-term history of August calm prevailed, and markets skated through the month with broad based gains, with small-caps leading the way for once. Give it a read!

Aug 29, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Happiness is good health and a bad memory.” – Ingrid Bergman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s all over. With Labor Day falling as early on the calendar as it possibly can, today marks the unofficial last trading day of Summer. Not surprisingly, futures are glum. The S&P 500 is indicated to open 0.3% lower, while Nasdaq futures are down by a more substantial 0.5%. The 10-year yield is trading modestly higher (less than 2bps), and the 4.22% yield is near the lowest level since April. Crude oil is fractionally lower, while natural gas is modestly higher. Gold is seeing modest losses, but cryptocurrencies are down by larger amounts, with Bitcoin down 2% and trading under $110K while Ethereum is down closer to 3% and trading below $4,350.

It may be the last summer Friday of the year, but the economic calendar is packed with data. Starting at 8:30, we’ll get Personal Income and Spending along with PCE and Wholesale Inventories. At 9:45, we’ll get the August Chicago PMI, which is expected to come in at 46.5, and that would be a modest downtick from July’s reading of 47.1. Finally, consumer sentiment from UMich will hit the tape at 10 AM. After a weaker-than-expected preliminary reading on 8/15, the headline reading is expected to remain unchanged at 58.6.

In Asia, the Nikkei was fractionally lower but finished the week higher. Japanese economic data was weak, with both Retail Sales and Industrial Production coming in significantly weaker than expected. While the weakness in those reports was disappointing, Tokyo CPI also came in lower than expected, which was positive. In China, shares of Alibaba (BABA) are higher following reports that the company is rolling out AI chips designed to fill the void left by the ban on Nvidia (NVDA) exports to the country.

Like the picture for US futures, European equities are also firmly lower as the STOXX 600 is trading down 0.5% taking its week-to-date decline to 2%. Country-specific equity benchmarks are also down across the board by similar amounts, although Spain is seeing outsized losses with a decline of over 1%. Banks are notably weak in the region following UK proposals to tax banks to pay down deficits.

Heading into this last trading day of the summer, the S&P 500 has been in rally mode, notching its 20th record closing high of the year, rallying over 2% since last Thursday, and trading well into short-term overbought territory.

One interesting aspect of the rally is that the new highs have come without the Technology sector making new highs in tow. The sector hasn’t exactly been lagging, but it hasn’t made a new high since August 13th.

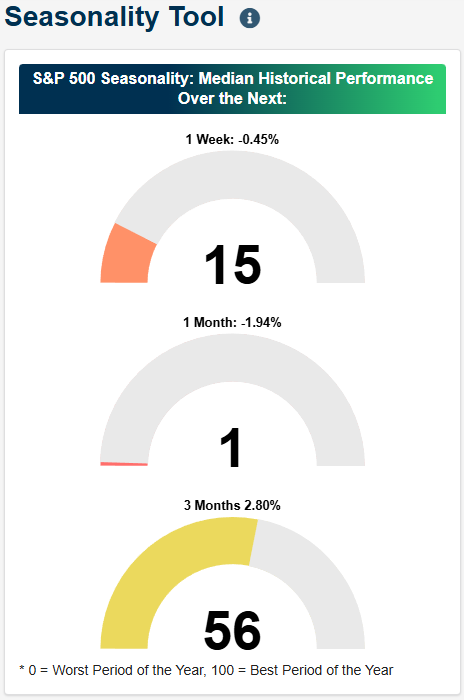

If the rally is to continue in the short term, the market will also need to do it without seasonality working in its favor. As shown in the Seasonality tool on our website, the S&P 500’s median performance over the next week based on the last ten years of data has been a decline of 0.45% which ranks in the 15th percentile of all one-week readings throughout the year. The median one-month performance has been a decline of 1.94% which is among the worst one-month periods of the year! As bad as that is, the median three-month performance is positive at 2.8% which ranks in the 56th percentile of all rolling three-month periods. Historically, the last three months of the year have been positive, but we still have to get through September first!

Aug 28, 2025

Remember back in the day when Apple (AAPL) was the largest company in the world, and you would always hear the phrase, “As goes AAPL, so goes the market”? It was a comment that usually came from bears at times when AAPL’s stock was weak, and they used it as a justification for their bearish sentiment. Reality showed that while AAPL was a large share of the entire market, there were several times when the stock faltered, and the broader market remained strong, and vice versa.

AAPL is no longer the largest company in the world and now trails both Nvidia (NVDA) and Microsoft (MSFT) in terms of market cap, which further illustrates the point that the market can rally without AAPL. Just like with AAPL, the market can rally without NVDA and/or MSFT, too. It can also fall at times when those stocks rally. With a market cap of over $3 trillion, AAPL is still a significant part of the S&P 500, but the two can still move independently of each other. The last 12 months are a perfect example.

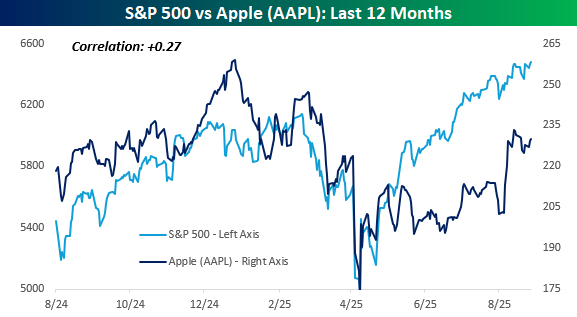

The chart below compares the performance of AAPL versus the S&P 500 over the last year. While the two traded in similar directions late last year, their paths haven’t been very similar in 2025. AAPL hasn’t closed at a record high since late December, while the S&P 500 is on pace today for its 20th record close of the year. Also, back in February, when the S&P 500 was making new highs, AAPL topped out with a lower high. In the rally off the April lows, as well, the S&P 500 surged, but from mid-May through early August, AAPL moved sideways. As a result of their divergent paths, the correlation between the closing prices of AAPL and the S&P 500 over the last year has been just +0.27.

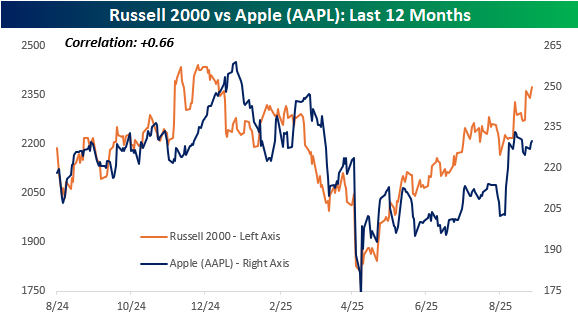

Where things really get interesting is when you compare the performance of AAPL versus the Russell 2000 over the last year. AAPL may be the third-largest stock in the world, but it has tracked the performance of the Russell 2000 much more closely than the S&P 500. Don’t take our word for it, just look at the chart. While the correlation between AAPL and the S&P 500 over the last year has been just 0.27, with the Russell 2000, it has been +0.66!

Whether AAPL trades more like a small cap than a large cap can be debated, but what about AAPL itself? After trading in a sideways range from late March through early August, AAPL finally broke out of that range just over two weeks ago and broke its downtrend from last December’s high in the process. Immediately after that breakout, the stock tested those breakout points, and provided those levels hold in the days ahead, you probably won’t be hearing that the market can’t rally without AAPL much in the weeks ahead.

Aug 28, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is nothing more frightful than ignorance in action.” – Johann Wolfgang von Goethe

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s another quiet morning in the markets despite what has been a busy overnight session for earnings. Of the 33 companies that reported since the close yesterday, just six missed EPS forecasts. On the geo-political front, there have been some ripples as Mexico announced that it will increase tariffs on Chinese imports, while Japan’s trade representative has cancelled a planned trip to the US, which will further delay trade negotiations. Regarding the Fed, the only speaker on the calendar today is Governor Waller after the close.

The economic calendar is busy this morning. Q2 revised GDP came in at 3.3% vs forecasts for 3.1% while Personal Consumption and the GDP Price Index were right in line with forecasts. Initial Jobless Claims came in at 229K, which was 1K lower than estimates. Continuing Claims, which have been drifting higher lately, also came in lower than expected at 1.954 million versus forecasts for 1.966 million.

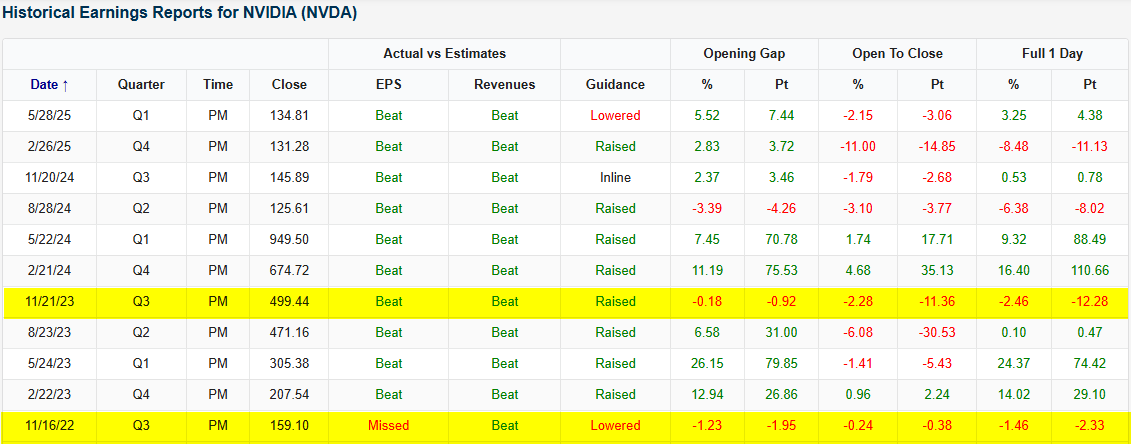

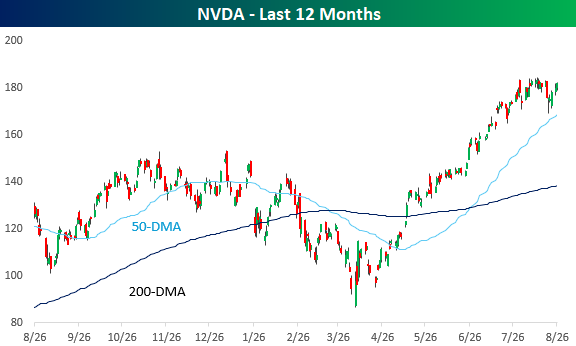

We made it through NVDA’s earnings report. The world’s largest publicly traded company released an uneventful earnings report last night, and while results were better than expected, that hasn’t been enough this earnings season to provide a meaningful boost to a stock’s price. In pre-market trading, NVDA is trading down less than 2%, which is basically a rounding error relative to the stock’s historical reaction to earnings. Over the last 25 years, NVDA’s average one-day reaction to earnings has been a gain or loss of just under 8%. Since the launch of ChatGPT, there have only been two other quarters out of 11 where the stock gapped up or down less than 2% in reaction to earnings, and today will likely be the third time in the last 12. For more than a week, all we heard about was the importance of NVDA’s earnings report and what it would mean for the market. Well, NVDA earnings came, and NVDA earnings went, and the most hyped earnings report in weeks has ended up being a non-event.

NVDA came into last night’s earnings report in a bit of a holding pattern after hitting record highs a couple of weeks ago. The stock has been gradually trending lower in the short term, but remains above its 50-DMA, so provided the stock doesn’t experience a significant move during the trading session, today’s action and last night’s report will have no impact on the stock’s technical picture.

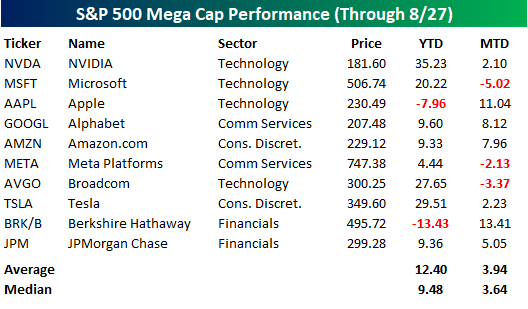

There’s been a lot of talk over the last several weeks regarding rotation within the market, but strength at the top has been consistent. The ten largest stocks in the S&P 500 are up an average of 3.94% (median: 3.64%) so far this month, and just three are in the red. On a YTD basis, the ten stocks are up an average of 12.40% (median: 9.48%), and only two are down.

At the other end of the market cap spectrum within the S&P 500, the ten smallest stocks in the index are slightly underperforming the ten largest stocks this month on an average basis but outperforming on a median basis. Where the big discrepancy shows up is in the YTD column, where the average performance has been a decline of 13.75%, or a performance gap of more than 26 percentage points!

Aug 27, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We’re moving from a world where we have to understand computers to a world where they will understand us.” – Jensen Huang

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you missed yesterday’s CNBC segment discussing recent market rotation, you can watch it by clicking on the image below.

It’s another quiet market morning with futures indicating just a modest gain at the open. Treasury yields are modestly higher across the curve, while crude oil is essentially flat at around $63 per barrel. In contrast, gold and other metals are slightly lower. There’s no economic data on the calendar this morning, and, outside of some earnings from retailers like Abercrombie & Fitch (ANF), Kohl’s (KSS), and Williams-Sonoma (WSM), the earnings calendar is light. Even the endless coverage of the Cook firing has subsided!

The quiet tone will change this afternoon when Nvidia (NVDA) reports after the close. Along with NVDA, we’ll also get reports from HP (HOQ), CrowdStrike (CRWD), NetApp (NTAP), and Urban Outfitters (URBN). The next two days will also be much busier on the economic calendar, so enjoy the calm while it lasts.

In Asia overnight, Japan was slightly higher while China traded lower as Industrial Profits for July fell 1.7% on a YTD basis. Australian stocks finished the session with fractional gains despite a CPI report which came in much higher than expected at 2.8% y/y versus forecasts for an increase of 2.3%.

European stocks are also trading much like US futures with little in the way of gains or losses. The STOXX 600 is up 0.15% with Germany trading slightly lower while France is bouncing back 0.45% from Tuesday’s 1.6% decline.

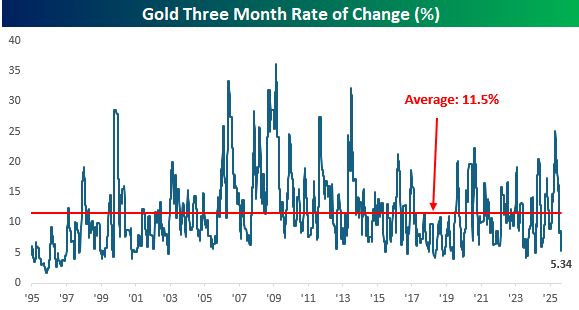

Gold prices are doing little this morning, and the last few months have been like watching paint dry for the yellow metal. After hitting an all-time high just above $3,500 per ounce in early April, gold has made multiple other attempts at breaking out above that level. While they have been unsuccessful, gold hasn’t sold off following those rejections, which has resulted in a relatively narrow range in recent months.

Over the last three months (63 trading days), in fact, the spread between gold’s intraday high and low has been just 5.34%, the narrowest three-day range since March 2024 and ranking in the bottom decile of three-month ranges over the last 30 years. This narrow range also marks a major shift from where this measure was four months ago in April, when the range topped 25% which was the widest since 2013.

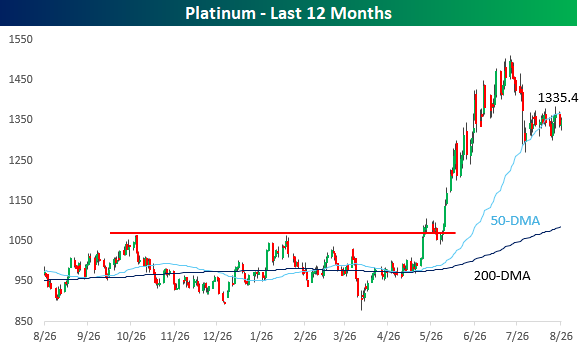

Like gold, platinum had been stuck in a range for several months from the second half of last year, with multiple run-ins with resistance just below $1,070. In late May/early June, though, it broke out of that range with vengeance surging as high as $1,500 before pulling back in July. Since that peak a little over a month ago, platinum has pulled back by about 11% and is now teetering on the 50-DMA, tenuously holding onto support. After such a large rally in such a short period, it’s only natural to see a pullback, so if these levels can hold, in the days ahead, platinum could start to look even more precious in the eyes of investors than it did even back in June.