Sep 11, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We just need every single person in this country to think about where we are and where we want to be. To ask ourselves, is this it?” – Spencer Cox

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Between the 24th anniversary of 9/11 and the political violence in Utah, there’s a lot to think about this morning before even considering the markets. The big news of the day will obviously be the August CPI report, along with jobless claims, which are just hitting the tape as we send this. Overnight, Asia had a mixed session with the Nikkei up over 1%, while Chinese equities also surged 1.7% following reports that the government will provide more stimulus for state-backed banks. On the trade front, though, Mexico said it will increase tariffs on vehicle imports from Asia to 50% from 20%.

In Europe this morning, the STOXX 600 is up 0.4% and every major country equity benchmark is also trading in the green. As expected, the ECB left rates unchanged.

In the US, equity futures were modestly higher heading into the data, while treasury yields were up about 2 bps across the curve. Crude oil and gold were fractionally lower, while cryptocurrencies were broadly higher, with Ethereum up over 3%.

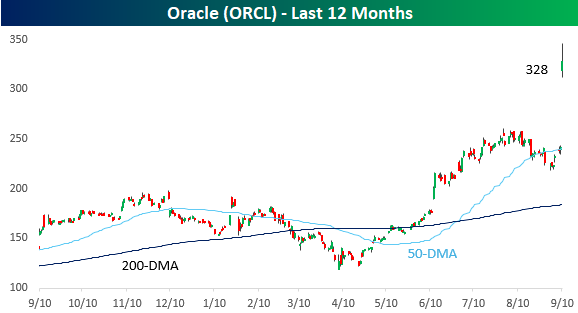

Yesterday’s surge in Oracle (ORCL) was unbelievable. If you saw the chart pattern below for a small-cap stock, it would look impressive, but when one of the largest companies in the world experiences a breakout like that, it’s jaw-dropping.

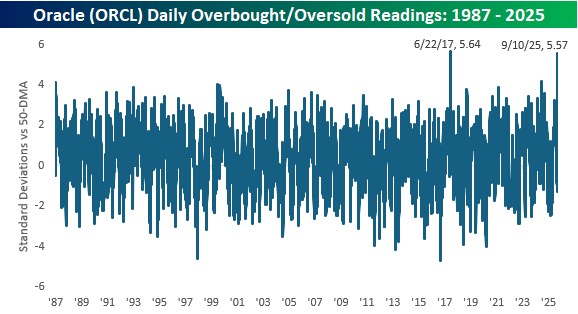

With yesterday’s surge, shares of ORCL reached ludicrously short-term overbought levels by closing 5.57 standard deviations above its 50-day moving average (DMA). As crazy as that level is, it’s not even the most overbought reading ORCL has ever registered. As shown in the chart below, back on 6/22/17, ORCL shares closed 5.64 standard deviations above their 50-DMA after the company reported an earnings report which showed strong growth in its cloud business.

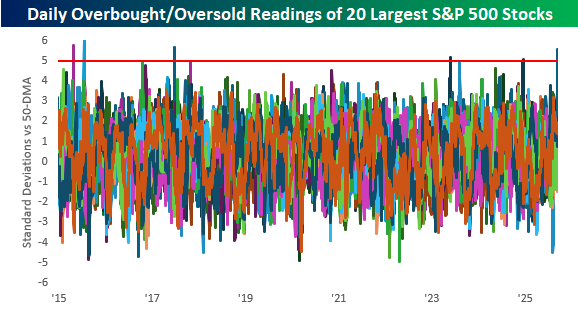

The chart below looks like a mess, and we don’t expect you to get too much insight from it. What it shows is the daily overbought/oversold readings for the 20 largest stocks in the S&P 500 over the last ten years. The point here is to show that it’s incredibly uncommon for large and mega-cap stocks to reach overbought levels like ORCL did yesterday. It’s only happened a handful of other times!

Sep 10, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I believe people have to follow their dreams – I did.” – Larry Ellison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Between Oracle’s (ORCL) 30%+ surge this morning and a weaker-than-expected PPI report, you would expect futures to be higher, but maybe the biggest surprise is that they aren’t up more. Both the S&P 500 and Nasdaq are indicated to open up 0.5%, and given it’s still September, bulls will take all they can get. Treasury yields are little changed, commodities are fractionally higher, and crypto is seeing the largest gains as Bitcoin and Ethereum are both up over 1.5%.

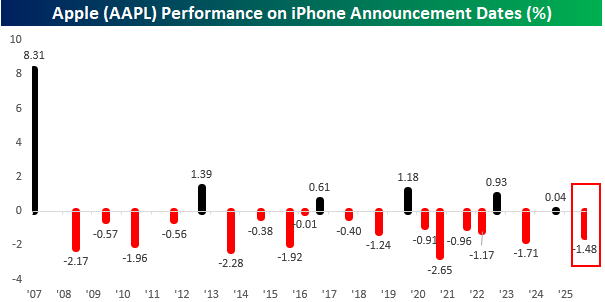

The market’s focus has now shifted to the upcoming inflation data, but yesterday, Apple (AAPL) was a focus with the launch of the latest iPhone models. As noted in our Chart of the Day from Monday, AAPL’s performance on the day of iPhone announcements has been weak, and yesterday was no exception as the stock fell 1.48%. As shown in the chart, for all the gains AAPL has had in the iPhone era, one of the worst days to own the stock has been on these announcement days.

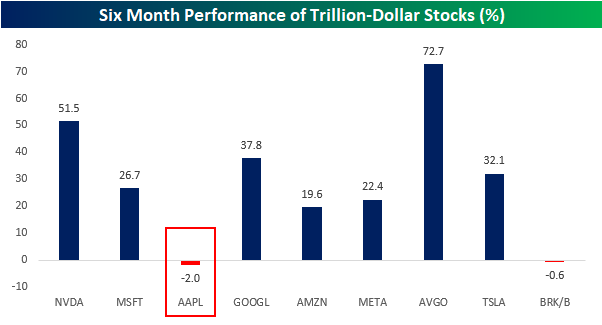

Normally, AAPL’s stock performs well in the lead-up to iPhone announcements, but that hasn’t been the case this year. Over the last six months, the stock has declined 2%, which is weaker than any of the other nine trillion-dollar S&P 500 stocks. The only other one that is down during this stretch is Berkshire Hathaway (BRK/b), which also happens to be one of the company’s largest shareholders.

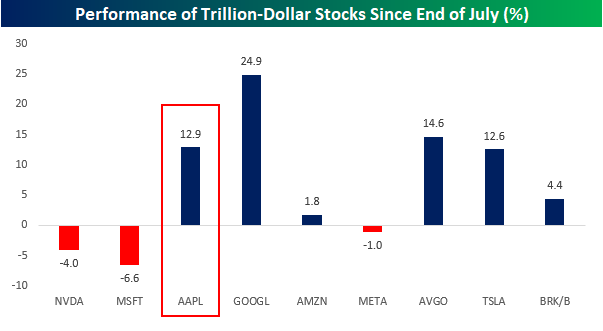

More recently, though, AAPL has started to turn the corner. Since the start of August, the stock has rallied 12.9% which ranks as the fourth-best among the trillion-dollar stocks, trailing Alphabet (GOOGL), Broadcom (AVGO), and Tesla (TSLA).

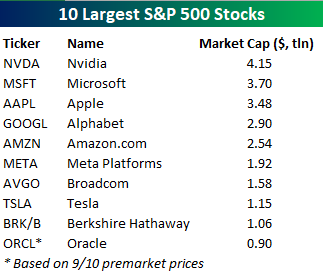

Speaking of the largest stocks, the trillion-dollar club may be on the verge of getting a new member. As of yesterday’s close, shares of Oracle (ORCL) had a market cap of $680 billion. After reporting a blowout earnings report, though, the stock is trading nearly 32% higher in the pre-market, which would take its market cap up just shy of $900 billion, catapulting it from the 13th largest stock in the S&P 500 and into the top ten list. It’s hard to comprehend just how large a move ORCL is having in reaction to its earnings. Only 42 companies in the S&P 500 have a larger market cap than ORCL’s market cap increase since the close yesterday, and it’s also larger than the entire market cap of Disney (DIS). Less than 0.35% of all earnings reports since 2001 have seen a stock rally more than 31% in reaction to earnings, and in those rare instances, the gains have been typically in small and micro-cap stocks.

Sep 9, 2025

This content is for members only

Sep 9, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Wrong does not cease to be wrong because the majority share in it.” – Leo Tolstoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After modest gains in US equities to start the week, futures have a positive bias this morning ahead of a relatively quiet day for economic data. The only report on the calendar is the NFIB Small Business Confidence report for August, which came in slightly better than forecasts, rising from 100.3 to 100.8.

An even bigger news story today will be the Preliminary Benchmark Payrolls Revision from the BLS. While the data is even more backward-looking than most other economic data, the headline number is expected to show a large downward revision to the number of jobs created between April 2024 and March 2025. Economists forecast the downward revision to anywhere between a loss of 450K to 900K, so you can guarantee that at the very least, both sides of the political aisle will seize on the headlines.

Finally, Apple (AAPL) will hold its ‘awe-dropping’ iPhone event at 1 PM eastern, where a new line of phones, along with updated iPads, watches, and AirPods, are expected. If you didn’t see it yesterday, make sure to check out yesterday’s Chart of the Day, where we looked at the stock’s performance around prior iPhone launch events.

Besides the modestly positive tone in equities, treasury yields are slightly higher, but the 10-year is still under 4.07%, and WTI, while higher by about 1%, is still below $63 per barrel. In the metals market, performance is mixed with modest gains in gold and platinum, while silver is slightly lower. Lastly, crypto is higher across the board with Bitcoin, Ethereum, and Solana all up by close to 1%.

Outside of the US, Asian equities were mixed overnight. The Nikkei broke a streak of three straight days of at least 1%+ gains with a decline of 0.4%, while China’s Shanghai Composite fell 0.5%. European stocks are hanging on to small gains (0.14%). Germany is the biggest outlier with a decline of 0.4% while other countries in the region are offsetting those losses.

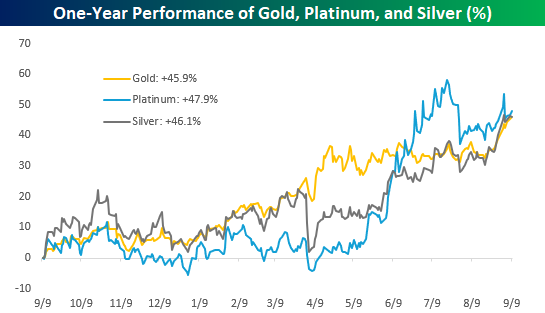

When it comes to precious metals and crypto, the first asset that immediately comes to mind for most people is gold, and given its recent performance, deservedly so. However, when you look at gold’s performance in comparison to other major precious metals like platinum and silver, their performances are nearly identical. Over the last year, gold has gained 45.9% while platinum and silver have rallied 47.9% and 46.1%, respectively. Their paths haven’t necessarily been identical, but they’ve ended up at the same place.

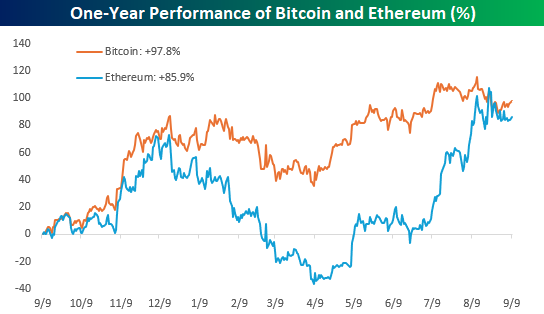

In the crypto space, Bitcoin is effectively the gold standard, and for most ‘investors’, it is the crypto market. Here again, Bitcoin’s performance hasn’t been much different than the ‘silver’ of that market – Ethereum. Here again, the paths of the two cryptos haven’t necessarily been the same, but they’ve essentially ended up at the same place. While Bitcoin is up 97.8% over the last year, Ethereum’s 85.9% gain isn’t far behind, especially for an asset class as volatile as crypto.

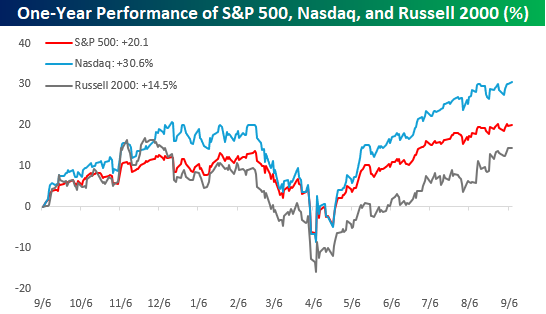

While the major metals and cryptos have had similar performances to each other over the last year, the same can’t be said for equities. While their trading patterns have been similar over the last year, the Russell 2000’s 14.5% gain comes up well short of the S&P 500’s 20.1% gain and pales in comparison to the Nasdaq’s gain of over 30%. While precious metals and, to a lesser degree, the leading cryptos have been almost interchangeable in their performance over the last year, equities, the most liquid of the three asset classes, have seen more varied returns.

Sep 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Time lost can never be recovered.” – Erik Larson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

In terms of economic activity, last week’s ISM Services report was better than expected and firmly in growth territory at 52.0, but the ISM Manufacturing and August payrolls reports both missed expectations, lending some credence to the idea that the economy is showing signs of slowing. This week, the focus will shift to inflation with Wednesday’s PPI and Thursday’s CPI reports for August. Secondary indicators of inflation have shown some upward pressure, so the market is clearly more concerned with these indicators coming in hot. How hot is the question? While a September cut next week is likely a done deal, the pace of cuts moving forward from there will hinge in large part on how ‘bad’ the inflation data is. Come Thursday morning, the market will either be only thinking about stagflation or three cuts between now and year-end.

It’s been a slow start to the week stateside, and the only economic report on the calendar this morning is the NY Fed’s Survey of Consumer Expectations, and the focus of that will be inflation expectations. Futures are modestly higher, along with crude oil, gold, and crypto.

Asian equities started off the week positive. The Nikkei rallied 1.5% closing just shy of a new high, while China was up a little less than 0.5%. Japanese GDP for Q2 came in better than expected, and China’s trade surplus handily beat expectations.

In Europe, equities kicked off the week on a positive note. The STOXX 600 is up about 0.3% as Spain and Germany lead the way higher. Investor sentiment from Sentix came in weaker than expected and declined modestly from August, but Industrial Production in Germany managed to exceed forecasts with a slightly better than expected increase.

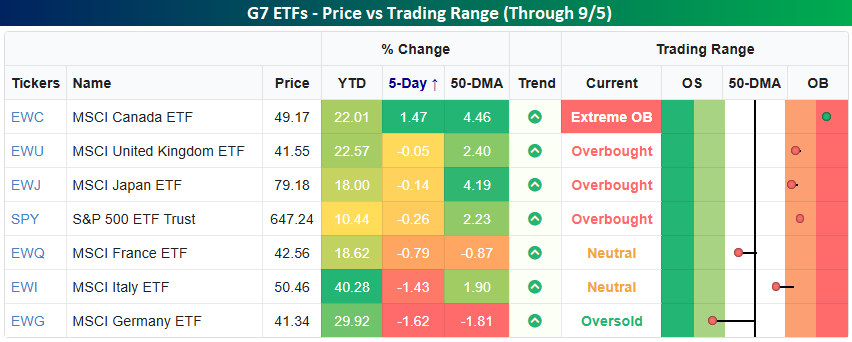

Last week was literally a middle-of-the-road week for the S&P 500. As shown in the snapshot of the ETFs tracking the equity markets of each of the G7 countries, the SPDR S&P 500 ETF’s decline of 0.26% from the close on 8/28 (due to last Monday’s Labor Day holiday) was right in the middle relative to the other six country ETFs. Canada (EWC) was the big winner of the group with a gain of 1.47% while every other ETF traded lower. Performance in the UK (EWU) and Japan (EWJ) was less bad than the US, while Germany (EWG) and Italy (EWI) both declined over 1%, and France (EWQ) fell 0.79%.

With respect to their trading ranges, Germany is the only country in the G7 trading at oversold levels, while France is the only other one trading below its 50-DMA. At the other end of the spectrum, the US and the three other countries that outperformed it last week are all at overbought or ‘extreme’ overbought levels (2+ standard deviations above their 50-DMAs).

While the US was right in the middle of the road last week, with its 10.44% YTD gain, it is still easily the weakest performer among the G7. In fact, the next closest performer is Japan with a gain of 18% while Italy is up over 40%!