Bespoke’s Morning Lineup – 9/16/25 – Streaky Semis

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The beautiful thing about learning is nobody can take it away from you.” – B.B. King

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We’re looking at another positive start to the market this morning, with futures modestly higher and the Nasdaq leading the way as mega-caps continue to lead the way. This morning’s economic calendar includes Retail Sales and Import Prices at 8:30, Industrial Production and Capacity Utilization at 9:15, and then Business Inventories and Homebuilder Sentiment at 10. After that, pretty much all of the focus will shift to tomorrow’s announcement from the FOMC, where rates are widely expected to be cut 25 bps.

This morning’s gains follow what was mostly a positive session in Asia. The highlight of the region was South Korea, where the Kospi rallied more than 1% for its 11th straight daily gain. In Europe, the tone isn’t as positive as the STOXX 600 trades down 0.2% even as the ZEW survey of economic sentiment unexpectedly increased, although Industrial Production for the Eurozone rose less than expected (0.3% vs 0.4%).

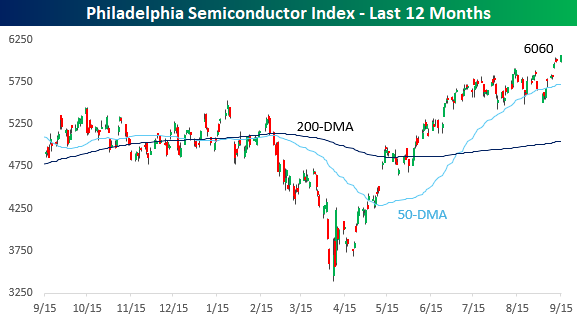

Like the major indices, semiconductor stocks have been lurching to new all-time highs, and when the semis are rallying with the overall market, it’s usually a good sign. After several successful tests of the 50-day moving average (DMA) in the summer, the Philadelphia Semiconductor Index (SOX) finally broke out above resistance last Wednesday.

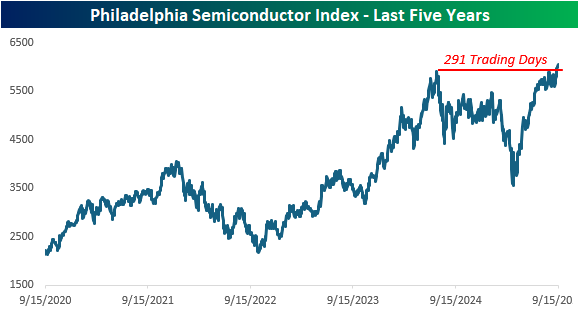

The breakout to new highs also ended a streak of more than a year during which the index had not traded at an all-time high. At 291 trading days, it was the fifth-longest drought without a new high in the SOX’s history, dating back to 199,4, and the sixth-longest that lasted longer than a year. The longest streak was nearly 4,500 trading days ending in January 2018, and the second-longest ended less than two years ago in December 2023 at 488 trading days.

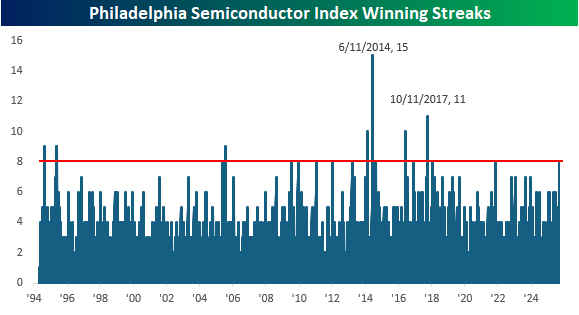

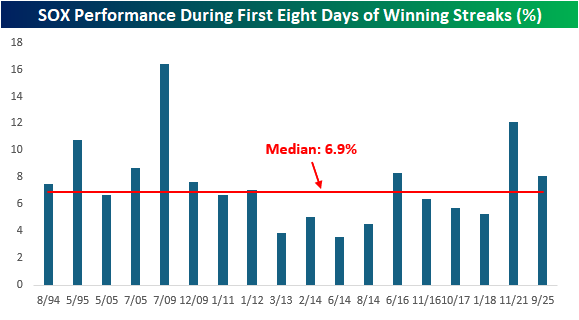

In the process of breaking out to new highs, the SOX has also traded higher for eight straight trading days, trailing the Nasdaq 100’s streak by a day. That eight-day streak is tied for the longest streak since October 2017, when it went more than two weeks in a row without trading lower. The longest streak was three weeks long, ending in early June 2014.

Over the course of the SOX’s eight-day streak, the index has rallied 8.1%, which comes in modestly ahead of the median gain of 6.9% during the first eight days of all 18 streaks and the sixth best overall.

7,8,9…

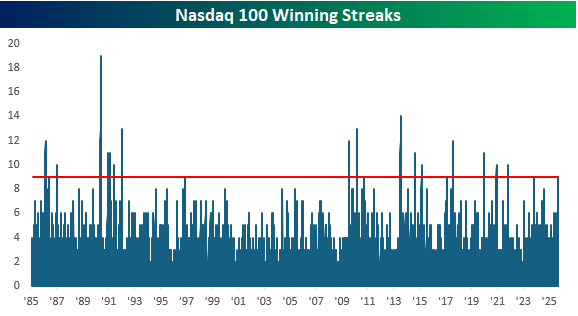

There are still a couple of hours left in the trading day, but with the Nasdaq 100 rallying more than 0.5%, it is on pace for its ninth straight day of gains. After gapping lower to start the month, it looked, on 9/2, like this September would show the weakness that typically accompanies the last month of the third quarter. After successfully testing the 50-day moving average (DMA) that day, though, the Nasdaq 100 has done nothing but trade higher, hitting new highs in the process.

If the Nasdaq 100 does finish the session higher today, it will be its longest winning streak in nearly two years (November 2023) and tied for the longest since November 2021, or nearly four years! The longest daily winning streak in the index’s history was 19 back in May 1990, just two months before a July peak that led to a 33% decline in the subsequent weeks. We also found it notable that while extended winning streaks were relatively uncommon before 2009, they have become far more frequent in the last 15 years. For example, in the 23+ years from 1985 through 2008, there were just nine winning streaks of nine or more days, but in the last 16 years, there have been 13.

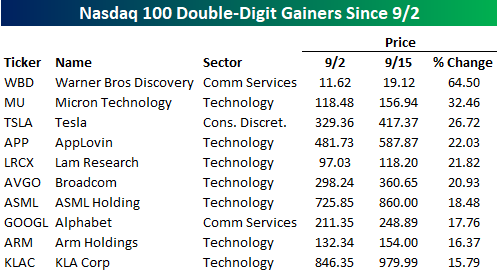

Over the course of the Nasdaq 100’s winning streak, the index’s 4.4% gain has been weaker than its average gain of 7.2% in the first nine trading days of prior streaks lasting nine or more days. As a result, there haven’t been a lot of big winners, and nearly half of the index’s components are lower since the streak began. Of the index’s 100 components, just ten are up 10% or more during the streak, with Warner Bros. Discovery (WBD) leading the way as merger speculation has pushed that stock up 64.5% since the close on 9/2. Besides WBD, seven of the ten stocks listed are from the Technology sector, and while not many stocks are up by double-digit percentages, an unlikely trio of mega-caps made the list with Tesla (TSLA), Broadcom (AVGO), and Alphabet (GOOGL) rallying 26.7%, 20.9%, and 17.8%, respectively.

Bespoke’s Morning Lineup – 9/15/25 – Halfway Through September

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best way to make your dreams come true is to wake up.” – Muhammad Ali

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong week, markets are getting off to a positive start this week ahead of this week’s Fed meeting. The S&P 500 is indicated to open with a gain of 0.25%. Overnight, Asia was mixed, but Europe has been higher across the board. The economic calendar is light to kick off the week, as the Empire Manufacturing report came in weaker than expected. Later on this week, things will pick up with Retail Sales highlighting Tuesday’s schedule and Housing Starts and Building Permits coming on Wednesday, along with the Fed.

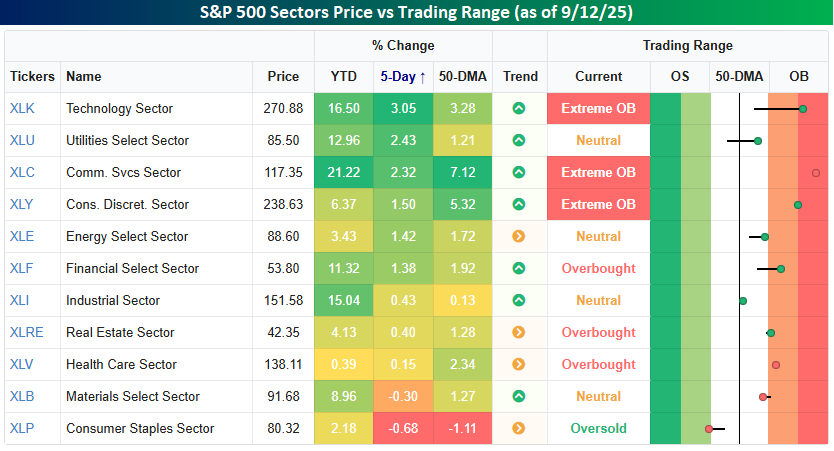

Markets are always forward-looking, and last week they looked forward to this week’s FOMC meeting, where Powell & Co will announce a cut of at least 25 basis points (bps) on Wednesday. Last week, six sectors rallied by at least 1%, including Technology, Utilities, and Communication Services, which rallied more than 2% each. We’ve grown accustomed to seeing Tech and Communication Services rally in unison. However, it’s still hard to get used to seeing the traditionally defensive-oriented Utilities sector rallying alongside those two sectors, but markets are always evolving. On the downside, the only sectors to finish lower last week were Consumer Staples and Materials. They’re also the only two sectors to finish last week below their 50-day moving averages. Consumer Staples is even oversold as well!

Six sectors finished last week at short-term overbought levels heading into this week’s Fed meeting, including three at ‘extreme’ overbought levels. While there is nothing prohibiting overbought sectors from becoming more overbought in the short term, it also sets up the possibility of a sell-the-news reaction to this week’s rate cuts. Just something to be on the lookout for.

Bespoke’s Morning Lineup – 9/12/25 – Highs Keep Adding Up

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A cynic is a man who, when he smells flowers, looks around for a coffin.” – H.L. Mencken

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Well, the market can’t go up every day. Equity futures are on pace to close out the week on a modestly weaker note as the Dow and S&P 500 are indicated to open the session modestly lower. For its part, the Nasdaq is looking at modest gains following strong earnings from Adobe (ADBE), which has that stock trading up 3%. The 10-year yield is two bps higher, but at less than 4.04%, it’s been a good week for longer-term treasuries. Crude oil is up fractionally, along with most precious metals, but silver is up closer to 2%. In crypto, Bitcoin is looking at modest gain as it flirts with $115K, but Ethereum is back above $4,500 with a gain of over 2%, while Solana, the newest flavor of the month in the space, has surged over 5% to $239 and its highest levels since January.

The uneventful tone in the US follows what was mostly a positive session in Asia as Japan and South Korea rallied to new all-time highs. Outside of Australia, all the major averages in the region finished the week with gains of at least 1%, and in most cases more.

In Europe, the tone has been more subdued as the STOXX is trading slightly lower along with most major country benchmarks. For the week, though, returns have also been positive with gains of roughly 1%. One negative item has been growth in the UK, where GDP was unchanged in July, versus forecasts for an increase of 0.4%. Meanwhile, Industrial Production, which was forecast to be unchanged versus June, dropped by 0.9%.

Yesterday’s weaker-than-expected jobless claims report and mostly in-line CPI solidified the case for multiple FOMC rate cuts in the months ahead. The market responded with a very broad-based rally as over 85% of S&P 500 stocks traded higher on the session, and small caps outperformed large caps. The S&P 500’s 0.85% rally took it to another record closing high as the index now pushes up against a trendline that has been in place for the last year. As shown in the chart below, while stocks sold off sharply after the index bumped up against this rising ceiling early in the year, most times it has encountered this trendline, the pullbacks were modest.

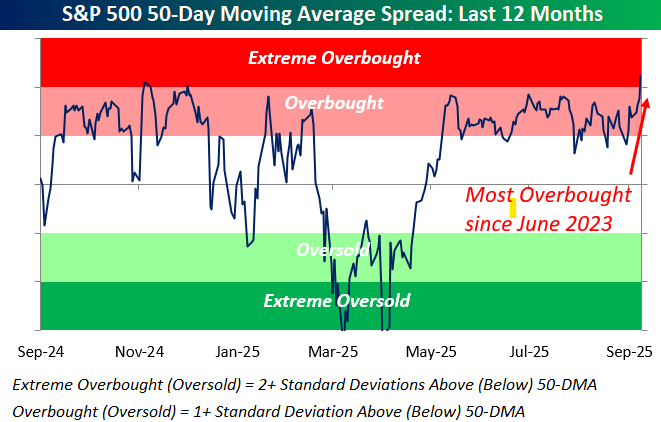

Following yesterday’s rally, the S&P 500 has now moved into ‘extreme’ overbought territory on a short-term basis, which we define as more than two standard deviations above its 50-day moving average (DMA). The last time it traded at more overbought levels was back in June 2023. We’ll have more on these ‘extreme’ overbought readings in tonight’s Bespoke Report.

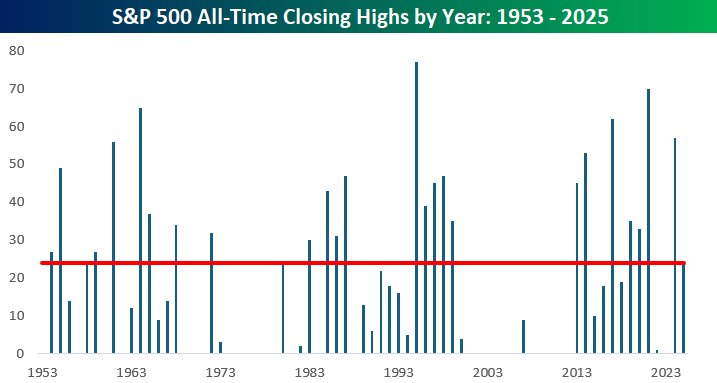

With yesterday’s new high, the S&P 500 has now had 24 record closing highs this year. While it’s above the historical average of 18 per year, 24 is hardly extreme by any stretch of the imagination, and it’s less than half of last year’s total of 57. On the other hand, back in early April, was anyone thinking we’d be anywhere close to new highs later this year, let alone hitting them multiple times? Be honest!

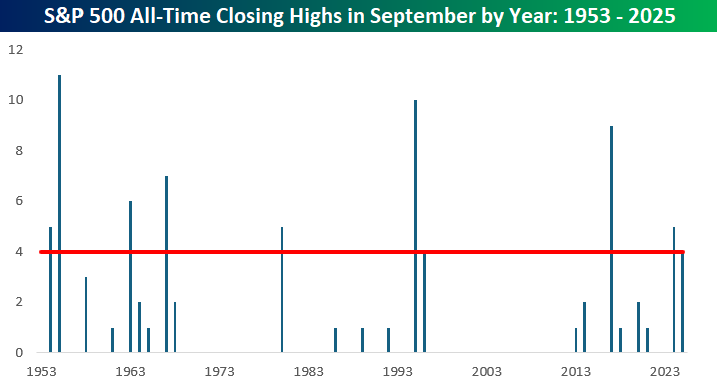

While September is historically known for its weakness, the S&P 500 has already had four record closing highs in eight trading days this month. That may be short of last year’s total of five, but there’s still another 13 trading days left in the month! The record for closing highs in September was 11 in 1955, followed by 10 in 1995, and 9 in 2017. If your memory is good (and long), you’ll remember that those were all good years, and some people reading this may have even been around for all of them!