Bespoke’s Morning Lineup – 12/16/25 – Honey, I Shrunk the Range

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The more wonderful the means of communication, the more trivial, tawdry, or depressing its contents seemed to be.” – Arthur C. Clarke

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Ahead of a busy morning for economic data, US futures are lower but well off their lows of the overnight session. S&P 500 futures are down just 10 basis points, while the Nasdaq is down 16. Treasury yields are down nearly 2 bps to 4.165%, and crude oil is down over 1.6% and on pace for another closing low. Gold prices are fractionally lower but still trading over $4,300 per ounce. In the crypto space, Bitcoin is up 1.5% but still only trading at $87,100.

As mentioned above, it’s a busy morning for economic data with Non-Farm Payrolls and Retail Sales hitting the tape at 8:30. It’s good to get some economic data again, but be forewarned that these reports could be noisy.

Most Asian markets were down at least 1% overnight, with South Korea leading the losses and falling over 2% as memory stocks were weak. European stocks are also weak this morning, but the losses are much more contained than what Asia saw overnight.

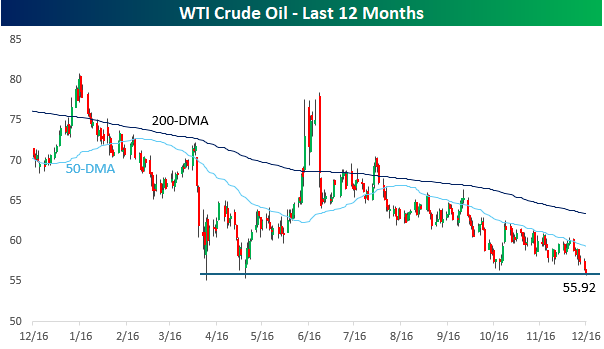

As mentioned above, crude oil prices are down over 1% this morning, and while not quite at 52-week lows on an intraday basis, if these losses hold, it will mark a new 52-week closing low. After briefly trading over $80 per barrel in January, prices have been in a steady decline almost all year. The only exception was back in June when prices briefly spiked after Israel launched airstrikes on Iranian nuclear facilities.

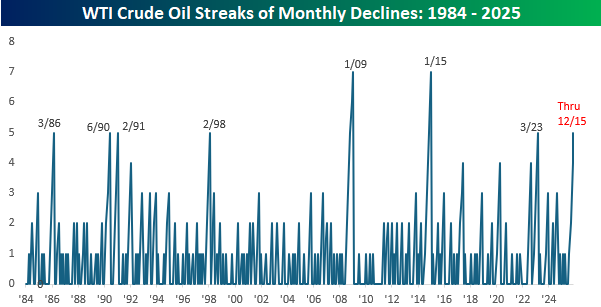

With this morning’s declines, crude oil prices are down close to 5% for the month, and if these losses hold throughout the next two weeks, it will be the fifth straight month of declines for crude oil. That would be tied for the longest streak since January 2015 (7 months). Since 1984, there have only been two longer streaks (7 months each) and five others that lasted five months. What would also make this current streak noteworthy if the losses hold is that it would also be the fifth month in a row that crude oil declines 2% or more. Since 1984, there have only been two streaks that lasted longer and one that lasted as long.

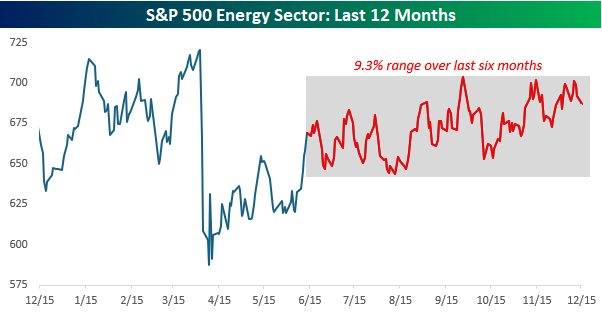

Even though crude oil is sinking towards new 52-week lows, the S&P 500 Energy sector has been holding up relatively well. While it’s underperforming the S&P 500 on a YTD basis, it’s still much closer to 52-week highs than 52-week lows. That may be partly due to the strength of natural gas, although even that commodity has weakened in the last few days, falling from $5.25 MMBtu on 12/5, down to $3.94 this morning.

Bespoke’s Morning Lineup – 12/15/25 – Midpoint

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life’s under no obligation to give us what we expect.”- Margaret Mitchell, Gone With the Wind

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a rough end to last week, bulls are shaking the dirt off their shoulders and looking to make a stand as we head into the final half of the month. Both the S&P 500 and Nasdaq are down fractionally so far this month, but with the seasonally strong second half of the month now here, will the bulls show up?

So far, they’re coming out on the offensive. Futures on all three of the major averages are higher by roughly 0.5%. The 10-year yield is moving lower and picking up in pace to the downside following a weaker-than-expected Empire Manufacturing report. Crude oil is fractionally higher, while gold and Bitcoin move higher.

Asian stocks started the week with broad-based losses. The South Korean Kospi led the losses with a decline of 1.8%, but both the Nikkei and Hang Seng finished down 1.3%. China also finished lower, but the losses were more contained at 0.6%. Besides follow-through from Friday’s losses in the US, the declines in the region also followed weak economic data out of China, where Industrial Production (4.8% y/y) and Retail Sales (1.3% y/y) both missed expectations.

Unlike Asia, European stocks are higher across the board with the STOXX 600 trading up 0.8%, with the UK, France, Italy, and Spain all up over 1% while Germany lags as peace talks in Ukraine continue to drag on.

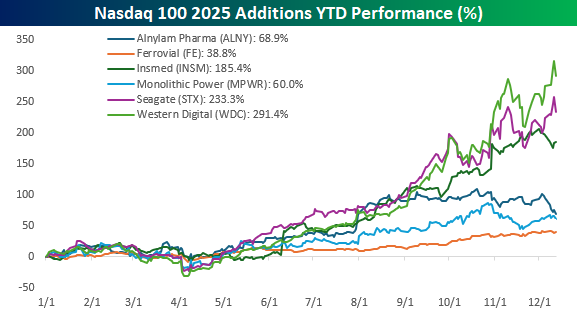

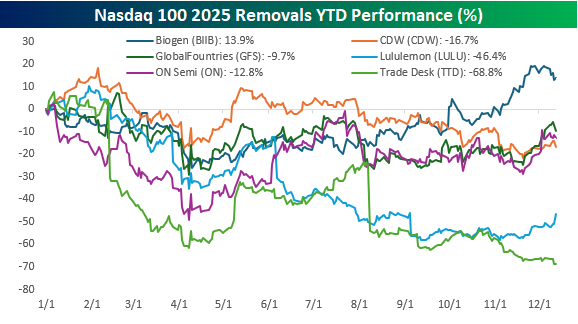

On Friday, Nasdaq announced the annual changes to the Nasdaq 100, and for this year’s shakeup, six stocks will be added and six removed. The new class of 2025 includes Alnylam Pharmaceuticals (ALNY), Ferrovial (FER), Insmed (INSM), Monolithic Power Systems (MPWR), Seagate Technology (STX), and Western Digital (WDC). The six stocks being removed to make room are Biogen (BIIB), CDW (CDW), GlobalFoundries (GFS), Lululemon Athletica (LULU), ON Semiconductor (ON), and The Trade Desk (TTD).

The two charts below show the performance of the six stocks being added and removed from the Nasdaq 100 on a YTD basis, and judging by their performance, one factor that appears to be part of the criteria is popularity. All six of the stocks being added this year have positive returns since the start of the year, and the median gain is 127.2%. Leading the way higher, Western Digital (WDC) and Seagate Technology (STX) have both rallied more than 200%. Even the worst performer of those stocks being added – Ferrovial (FE) – was 38.8%.

Turning to the six stocks being removed, they haven’t exactly shone this year. Five out of six of the stocks are down on the year, and the only winner – Biogen (BIIB) – is up only 13.9%. All totaled, the median performance of the six stocks is a decline of 14.8%.

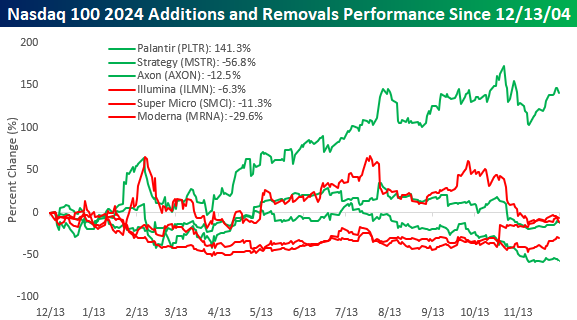

While six stocks are being added and removed this year, last year, there were only three. With one exception, the performance of both the stocks being added and removed from the Nasdaq 100 wasn’t particularly good. As shown in the chart below, shares of Palantir (PLTR) have rallied 141.3% since last year’s announcement that it was being added to the Nasdaq 100, but shares of Strategy (MSTR) and Axon (AXON) are both lower. Likewise, all three of the stocks removed last year are also lower, with declines in the range of 6.3% for Illumina (ILMN) to 29.6% for Moderna (MRNA).

Finally, since we’re talking about the Nasdaq 100, it’s worth pointing out that the index closed below its 50-day moving average again to close out last week as the latest rally off the November lows failed to make a higher high. With megacaps like Nvidia (NVDA), Microsoft (MSFT), and Oracle (ORCL) faltering recently, it’s showing up in the performance of indices they dominate, like the Nasdaq 100.

Broadcom (AVGO) Earnings Disappoint

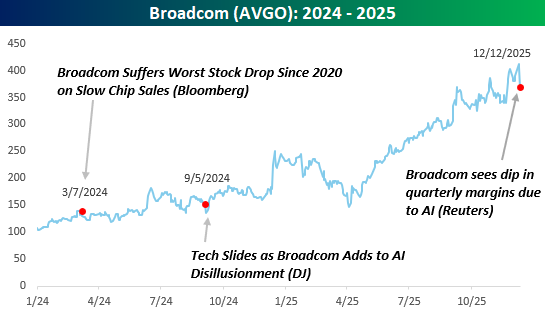

“Broadcom Suffers Worst Stock Drop Since 2020 on Slow Chip Sales” – Bloomberg

“Tech Slides as Broadcom Adds to AI Disillusionment” – DJ

“Broadcom sees dip in quarterly margins due to AI” – Reuters

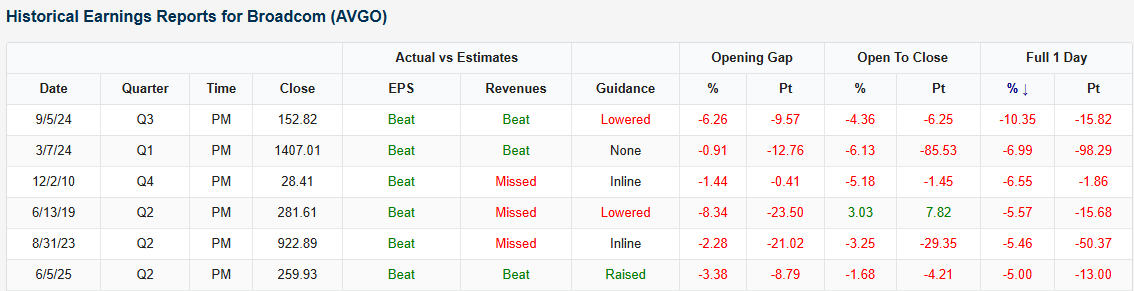

Shares of Broadcom (AVGO) are having a rough go this morning after the company reported earnings after the close yesterday. Despite reporting better-than-expected EPS and sales, as well as raising guidance, the stock is down around 9% this morning as management comments concerning margins and backlog spooked investors. Several analysts have said the comments were misinterpreted, but the stock’s reaction this morning tells another story.

Based on where the stock is trading this morning, today would be just the 7th time since at least 2009 that the stock declined more than 5% on an earnings reaction day, and if it stays at current levels through the close, it would go down as its second-worst earnings reaction day on record.

What’s interesting to note about the performance above, however, is that heading into today, the stock’s two worst earnings reaction days were in 2024. Despite those two clunker earnings reports, heading into today, AVGO has rallied over 275% since the start of 2024, making it the seventh-best-performing stock in the S&P 500!

Getting back to those headlines at the top, all three were written in reaction to AVGO earnings reports, but not yesterday’s. Only the Reuters headline was in reference to the most recent report, but the Dow Jones headline was written in response to its September 2024 report, while the Bloomberg headline pertained to its March 2004 report. In both cases, there was widespread concern over AVGO’s results, but the declines are barely visible on the chart.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

Bespoke’s Morning Lineup – 12/12/25 – Disco Fever

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Feel the city breakin’ and everybody shakin’, and we’re stayin’ alive, stayin’ alive” – Stayin’ Alive, Bee Gees

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to catch Bespoke co-founder Paul Hickey on Making Money with Charles Payne today at 2 PM Eastern on Fox Business.

Saturday Night Fever was released 48 years ago today, and when you think of that movie, “Stayin’ Alive” is the song that comes to everybody’s mind. With the S&P 500 closing at a new high yesterday, we can’t think of a song much better for the current market.

Ever since October 2022, the bull market has been ‘kicked around” by skeptics almost since the day it “was born.” The kicks came from all angles. Throughout the last three years, there have been repeated events that supposedly spelled the end of the AI rally. In the Summer of 2024, it was the unwind of the yen carry trade. Earlier this year, the haphazard rollout of US trade policy caused a tariff tantrum and raised concerns that Brand USA had lost its luster. Now, the fact that the Fed is cutting rates and rates at the long end of the curve aren’t falling has some arguing that the Fed has lost control.

With all these events and the scary headlines that accompany them, we can “understand the New York Times effect on man” and the potential to scare investors out of the market. Time after time (wait, that’s a Cyndi Lauper song), it felt like the market was “breaking and everybody shakin’”, but after the smoke cleared, that wasn’t Tony Manero on the dance floor striking the Disco Finger. No, that was the bull market hitting new highs and “ah, ah, ah, ah, stayin’ alive, stayin’ alive”.