Oct 15, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stock prices have reached what looks like a permanently high plateau” – Irving Fisher, 10/15/29

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a sell-off into the close yesterday, equity futures are rallying this morning on the back of strong rallies in Asia and Europe. S&P 500 futures are up 75 bps while the Nasdaq is up 1%. In the commodities space, crude oil is little changed, while gold is up another 1% and now over $4,200 per ounce.

While there’s little economic data on the calendar again today, it’s been another strong showing for earnings this morning as eight of the ten companies reporting exceeded bottom-line results, while Progressive (PGR) was the only miss. Revenues have also been strong as the pace of beats has been nearly as strong.

We’ve all said things that we wish we could take back, and we can all come up with countless examples involving a boss, friend, family member, spouse, and/or our kids. You don’t need us to give you examples. In a less personal sense, it’s always funny to look back at past comments from public figures and, with the benefit of hindsight, see how foolish or wrong their comments turned out to be.

The stock market has seen a lot, but one of the most famously disastrous comments was made exactly 96 years ago today when an economist named Irving Fisher spoke at an industry trade dinner in New York. Fisher was one of the most well-known economists of his generation. Joseph Schumpeter called him the “greatest economist the United States has ever produced”. His theories on the velocity of money helped him forecast swings in inflation and the economy, and he wrote a weekly economic column that was read by millions of readers. He spoke to audiences all over the country, and they hung on every word.

The most famous or infamous of those speeches came on 10/15/29 when he made the quote above, and then followed it up later on in an informal Q&A session, saying he expected “to see the stock market a good deal higher than it is today, within a few months.”

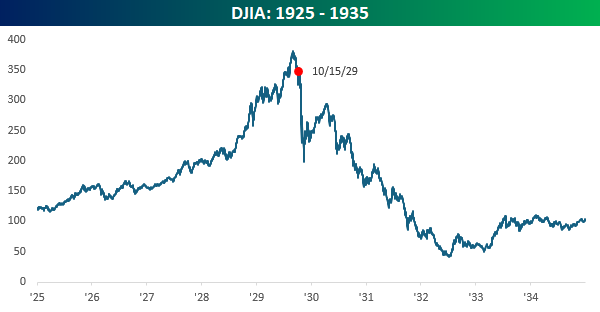

When Fisher made those comments, the equity market was coming off a solid year of gains. While the Dow was down about 8% from its September high, it was still up over 40% in the prior year. And that was coming off what had been one of the strongest four-year stretches in stock market history, where the index had tripled! Given the path equities had taken, Fisher’s comments were hardly out of consensus. At that point, gains were expected.

While investors were feeling entitled to gains, what the market giveth, it can quickly take away. The day after his comments, the Dow fell by over 3%. Then, after a one-day bounce of 1.7%, it had back-to-back declines of over 2.5%. Then, it kept falling from there. On 10/23, the DJIA fell 6.3%. On 10/24, it fell another 2%. Then, on 10/28, the crash came as the Dow fell 13% followed by another decline of 12% the day after that. Just after Labor Day of 1929, the Dow was at record highs, basking in the heat of the roaring 20s. Now, less than two months later, it was down 40%.

Looking at a ten-year window of the Dow from 1925 to 1935, from its peak in 1929 to the low three years later, it lost nearly 90% of its value. The economy sank into the Great Depression, erasing generations of wealth and causing permanent damage to the fabric of the US economy. Maybe not creative, but destruction nonetheless!

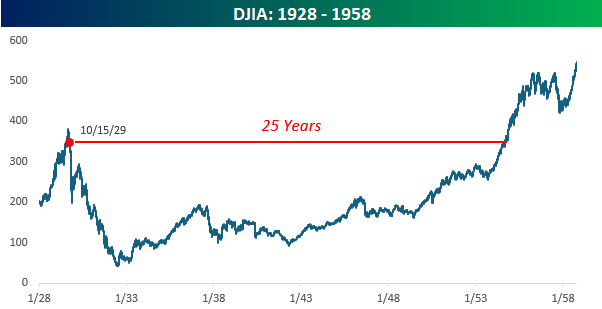

The S&P 500 closed at record highs just a week ago today, so no matter how steep the selloffs have been over time, the market has always come back. Sometimes, though, the comebacks take longer than others. After the peak this February, it only took a few months. After the 2022 peak, though, it took two years for the market to make new highs. Coming out of the Financial Crisis, it took close to five years. After the dotcom bust, it took seven years. The takeaway is that it’s all about time horizons. If you’re invested in the stock market, long periods of drawdowns shouldn’t necessarily be a baseline expectation, but they should be part of the plan. Coming out of the 1929 peak and Fisher’s comments from October 1929, those levels on the Dow wouldn’t be seen again for another 25 years! That type of drought should certainly not be a base case for investors, but it should provide some balance to a growing feeling of entitlement in some areas of the market where double-digit daily percentage gains are starting to feel like an Inalienable right.

Oct 14, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Pessimism never won any battle.” – Dwight Eisenhower

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If the market rallies on a bank holiday, does it count? Judging by the declines in US equity futures and cryptocurrency markets, it appears not. S&P 500 and Nasdaq futures point to a drop of about 1% at the open, which would erase about two-thirds of Monday’s gain. Declines in the crypto space look even scarier as Bitcoin drops 4% and Ethereum traded back down below $4,000 with a decline of nearly 7%.

The catalyst for this morning’s weakness stems from continued trade tensions with China as both countries start charging additional fees on each other’s cargo ships, and China imposed further sanctions on certain US shipping subsidiaries. The weakness also comes even after a strong batch of earnings reports on what is really the first busy day of earnings for the Q3 reporting period.

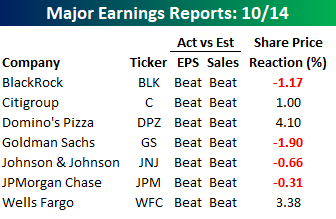

As shown in the table below, of the seven major reports this morning, all seven reported better-than-expected EPS and sales, but only three are trading higher in reaction to the reports. Domino’s (DPZ), Wells Fargo (WFC), and Citigroup (C) are all up 1% or more, while Goldman (GS) leads the declines with a drop of nearly 2%.

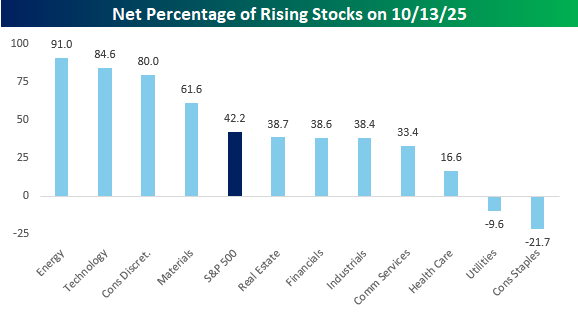

The S&P 500 had a good day to start the week yesterday, but breadth wasn’t exactly strong, especially for a day when the index rallied over 1.5%. As shown in the chart below, only four sectors saw a net of 50% or more of their components finish higher on the day. Energy and Technology led the charge with 90%+ of each sector’s components finishing higher on the day, while Consumer Discretionary (+80%) and Materials (+62%) were the only two other sectors where net breadth was stronger than the S&P 500. On the other end of the spectrum, Consumer Staples (-22%) and Utilities (-10%) both had negative net breadth, while Health Care also was relatively weak at just 17% net positive.

What was unique about yesterday’s trading, though, was that it was an extreme ‘inside’ day for the S&P 500 tracking ETF (SPY). An inside day in the market occurs when the intraday high for a day stalls out short of the prior session’s high, while the intraday low is higher. Not only did we have an inside day yesterday, but the intraday high was 1.3% below Friday’s high, while the intraday low was 1.1% above Friday’s low. We finished the day stuck right in the middle of the prior day’s range!

Inside days in SPY where both the intraday high and intraday low were more than 1% below or above the prior session’s extreme have been extremely rare. Since 1993, there have only been 11 other occurrences, with the most recent occurring back in April, right after the tariff-tantrum low. But before that, you have to go back to December 2020, and then before that, August 2015.

Oct 13, 2025

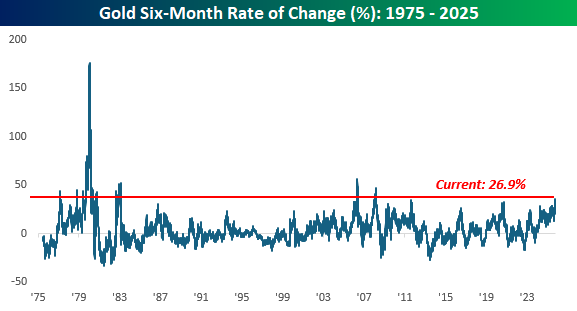

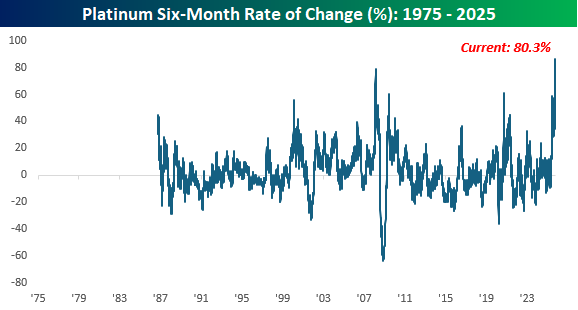

Precious metals prices have been going crazy lately. Gold’s move above $4,000/ounce last week garnered the most headlines, but its gains look pedestrian compared to other metals like silver and platinum. We’ll start with gold, though. Over the last six months, gold rallied 26.9%, and as of last week, it was up over 35% in six months. The last time it rallied that much in half a year was back in 2008.

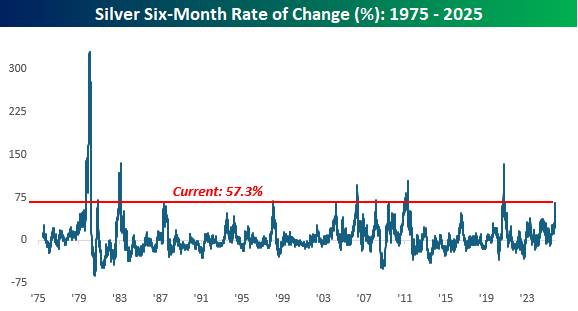

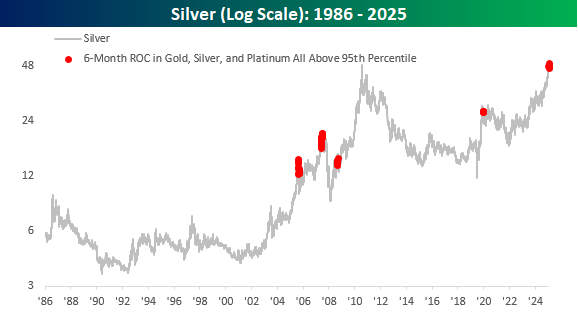

There’s nothing wrong with a gain of 26.9% in six months, but silver is still up by more than twice as much and was up over 65% in the trailing six months just last week. Historically, silver has been more volatile than gold, so its current run is ‘only’ the strongest since 2020.

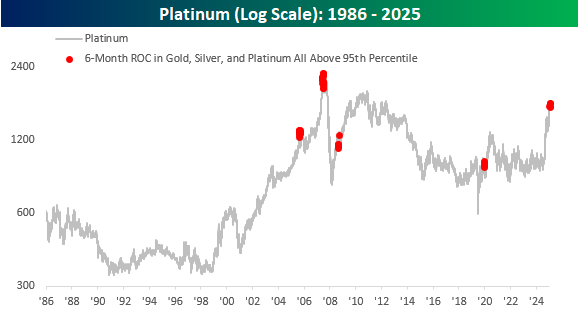

As if you think silver’s run has been impressive, platinum says “hold my beer.” Through today, platinum was up over 80% in the last six months, and as of last week, it was up over 86%. In futures pricing dating back to 1986, platinum has never had a larger six-month gain.

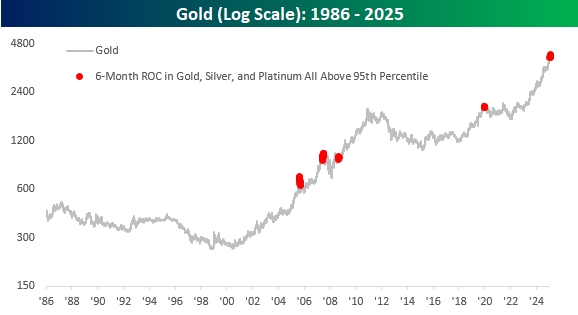

While all three metals have had widely varying rallies in the last six months, relative to their respective histories, their moves have ranked above the 95th percentile versus all other six-month periods. The charts below show the performance of gold, silver, and platinum since 1986, which is when we have pricing data for all three commodities. In each chart, we have also included red dots to show the times when all three metals simultaneously had six-month rallies that ranked in the 95th percentile or above of their respective histories.

The only other periods when all three metals simultaneously had six-month rallies that ranked in the 95th percentile or above were in May 2006, February to March of 2008, May to early June of 2009. and September 2020. Within the equity market, we often see overbought markets becoming more overbought, but in the case of these three metals, it wasn’t uncommon to see at least a short-term pullback following prior moves like the one we’ve seen recently.

Oct 13, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Riches don’t make a man rich, they only make him busier.” – Christopher Columbus

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a bout of ferocious selling on Friday for stocks and into the weekend for cryptocurrencies, investors took some time to think things through over the weekend, and they’re taking a more optimistic tone. Futures on the S&P 500 are 1% higher, while the Nasdaq trades up more than 1.5%. Bonds are closed for Columbus Day, but gold is sharply higher with a gain of over 2% and trading just under $4,100 per ounce. Crude oil is also bouncing back with a gain of 1.5% but is still trading below $60. It certainly could be worse, but even with this morning’s gains, the S&P 500 is still down well over 1% from Thursday’s close. The President may not like to see the stock market trade lower, but all the talk with China seems to have taken the shutdown off the front page of the business section.

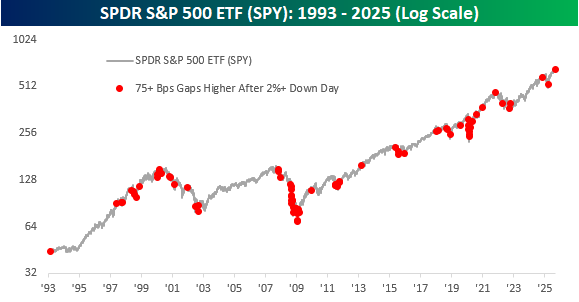

S&P 500 futures are still up over 1% but off their highs from earlier in the session. We looked at all prior periods when the S&P 500 SPDR ETF (SPY) fell 2% in a session and then gapped up at least 75 bps at the open the following day. We originally looked at 1% upside gaps, but with SPY now teetering on a 1% gain, we widened the band. The overall results of both analyses were very similar, though.

The long-term chart of SPY below shows every prior occurrence when SPY gapped up at least 75 bps after a 2%+ down day since its inception in 1993. While there were plenty of similar occurrences during the bear markets of 2000 to 2002 and 2008 into early 2009, there have also been plenty of other occurrences at various points in the market cycle.