Bespoke’s Morning Lineup – 1/6/26 – Only the Year Has Changed

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The freshest moments in my films have always been with unknown actors.” – John Singleton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The rally in the US to kick off the week yesterday continued overnight in Asia as Japan, China, and South Korea all rallied between 1.0% and 1.5%. The strength came amid a weaker manufacturing PMI reading in Hong Kong and a weaker services PMI in India. In China, the PBoC said that monetary policy would be maintained at loose levels to further support growth.

European stocks are also positive, but with more modest gains. The STOXX 600 is up 0.2%, and France’s 0.1% decline is the only major country benchmark in the red as bank stocks lag. The December Services PMI for December came in slightly weaker than expected, decelerating to 52.4 from 53.6 in November.

In the US, futures are on either side of the flatline, with S&P 500 futures barely higher, while Dow futures are barely lower. Nasdaq futures are faring better, but with an implied gain of 0.22% aren’t shooting the lights out. Treasury yields, crude oil, and gold are all fractionally higher, while silver, platinum, and palladium are all up over 1%. After a solid rally yesterday, which took it to its best levels in six weeks, Bitcoin is down modestly at just under $94K.

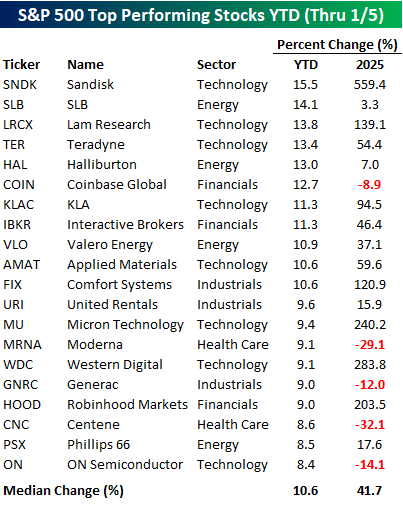

The market is always changing, but just because the year on the calendar changed last week, the performance of stocks leading the way higher hasn’t changed all that much- at least not yet. The table below lists the 20 best-performing S&P 500 stocks so far this year. For starters, Sandisk (SNDK) is the best-performing stock this year, and it was also the best in the S&P 500 last year, even though it didn’t have a full year of trading to gain more than 500%!

Besides SNDK, five of the other top performers were also stocks that more than doubled in 2025! Sure, there were some losers last year, like Centene (CNC) and Moderna (MRNA), that have gotten off to a strong start this year, but overall, last year’s median performance of the 20 best-performing S&P 500 stocks so far this year was a gain of 41.7%. The list is also dominated by tech, with eight of the 20 stocks coming from that sector.

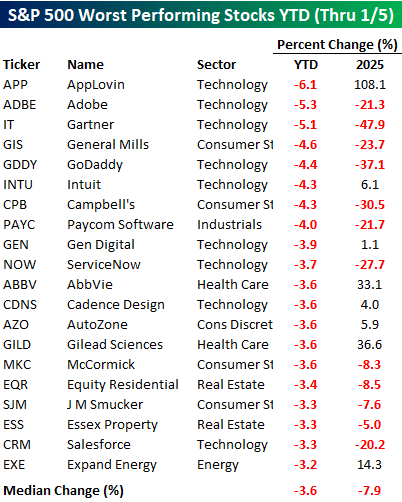

While eight of the 20 best-performing stocks in the S&P 500 so far this year are from the Technology sector, nine of the worst performers are also from the S&P 500’s largest sector. Besides AppLovin (APP), though, none of them were big winners in 2025. Of the 20 worst performers in the first two trading days of 2026, twelve were also down in 2025, and the median decline of all 20 was 7.9%. It’s also worth pointing out that the magnitude of the declines in the biggest losers so far this year is basically a third of the magnitude of the size of the gain in the biggest winners (-3.6% vs 10.6%).

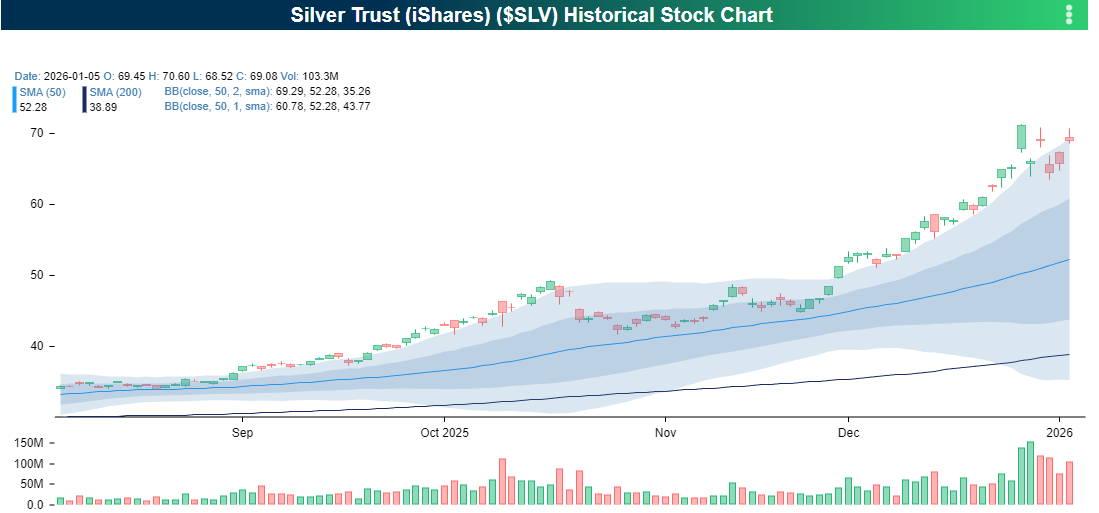

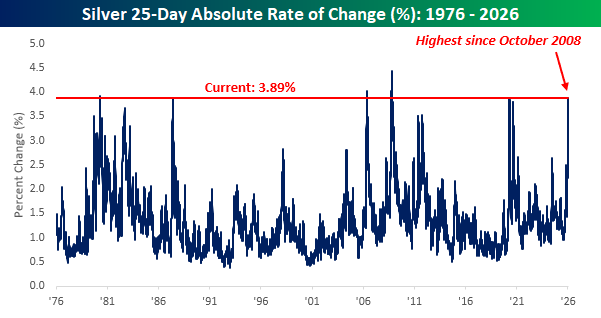

Another area where the change in the calendar didn’t impact that market was in the volatility of various metals. Silver is a perfect example, as volatility in gold’s bridesmaid hasn’t skipped a beat in the first two trading days of 2026. While silver only moved 0.58% last Friday, yesterday’s 7.1% rally was right in line with what has become the norm in recent weeks, and the chart is beginning to look increasingly funky with multiple detached candles with no overlap to the prior day’s range.

Over the last six trading days, silver’s daily move has been above 7% on five separate trading days, and the average daily move during the last 25 trading days has been 3.89%. That’s the highest average daily move over five weeks since October 2008, and there have only been a handful of periods in the last 50 years where the average daily move was higher. It doesn’t get more volatile than that. Somebody better put a ring on it.

Bespoke’s Morning Lineup – 1/5/26 – First Impressions Aren’t All They’re Cracked Up to Be

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What can a first impression tell us about anyone? Why, no more than a chord can tell us about Beethoven, or a brushstroke about Botticelli.” – Amor Towles

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Asian markets were the first to react to the Venezuela news from Saturday, and the response was positive. Japan’s Nikkei rallied 3% while China’s Shanghai Composite tacked on 1.4%, and South Korea surged 3.4%. India was a notable laggard in a sea of green as IT firms in the country declined after some cautious comments regarding the sector from Citi.

In Europe, the tone to start the week has been more subdued. The STOXX 600 is up 0.3% on modestly negative breadth. Germany is leading the way higher with a gain of 0.6% while Spain is fractionally lower.

In the US, S&P 500 futures are up nearly 0.30% while the Nasdaq is doing much better with a gai of over 0.6%. Treasury yields are little changed, and surprisingly, crude oil is only up fractionally. Gold is surging more than 2% while other metals prices are all up by at least twice that. Even crypto is catching a bid as Bitcoin is up over 1.5% and near $93K. If you’re a bull, it’s nice to see a positive reaction to the weekend news on the first real full trading day of the year, but we’ll be watching to see if the gains can be held through the trading session, which is a job the market has had a tougher time of doing in recent weeks.

With the start of every new year, investors tend to pay a lot of attention to first impressions. A strong start to the year raises hopes of a strong year, while weakness out of the gate causes investors to ask whether the market knows something for the year ahead. With the S&P 500 trading higher on Friday, the logic says that it should bode well for the rest of the year. Right?

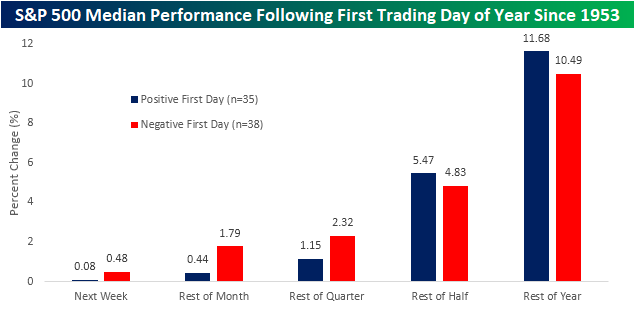

Whether stocks trade up or down to start the year is basically meaningless in the grand scheme of things. Going back to 1953, which was the first full year of the five-day trading week in its current form started, we looked to see how the S&P 500 performed on the first trading day of the year and then compared it to how it performed over the next week, the rest of January, the rest of the quarter, the rest of the half, and the rest of the year.

The chart below shows the S&P 500’s median performance following days when it was positive on the first trading day of the year (blue bars) and negative (red bars). Over the following week as well as the rest of the month and quarter, the S&P 500’s median performance was actually better following a down day to start the year than after a positive start. For the rest of the half and the rest of the year, though, performance was better following a positive start to the year. In both cases, though, the difference in returns was modest.

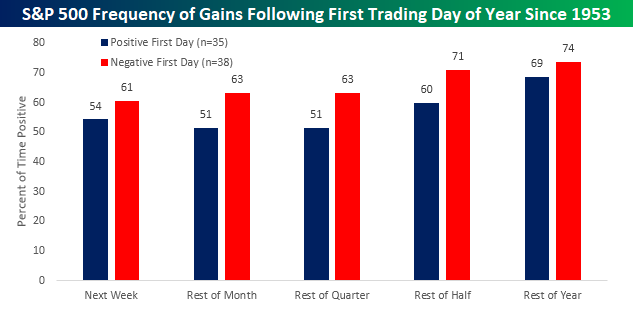

In terms of the consistency of gains based on first-day performance, the S&P 500 has been positive on a slightly more consistent basis following a negative start to the year, versus a positive start. Once again, though, the differences are modest at best.

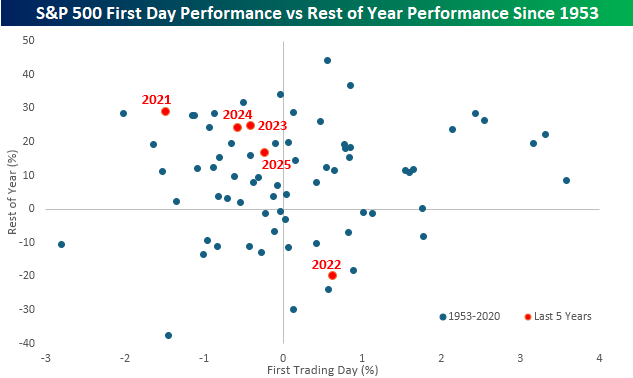

Not only have first impressions had little bearing on how the market performed going forward, but in recent years, it’s been the opposite. The scatter chart below compares the performance of the S&P 500 on the first trading day of the year (x-axis) to its performance for the rest of the year (y-axis). The random scattering of the dots provides another illustration of the lack of correlation.

One exception, however, has been the last five years (red dots). From 2021 through 2025, the S&P 500 traded down on the first trading day of the year four out of five times. 2022 was the only year that the first trading day was positive, when the S&P 500 traded up 0.64% to kick off the year. From the close on that first day through year-end, the S&P 500 dropped 19.95%. In the four other years when the S&P 500 traded down on the first trading day of the year, the S&P 500 rallied anywhere between 16.7% and 28.8% for the rest of the year. You would never base a prediction for the outcome of a baseball game on whether the first pitch was a ball or a strike, so don’t base your outlook for the year on which way the market trades on a day when most people were out of the office anyway. Even if it was higher.

Chart of the Day – Strategist Targets for 2026

This content is for members onlyBespoke’s Morning Lineup – 1/2/26 – New Year, Same Surprises

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The only true wisdom is in knowing you know nothing.” – Socrates

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As we approached the turn of the calendar, December was flooded with market outlooks for the year ahead, which always present the reader with highly confident expectations for the year ahead. Reading through most of them, the blueprint for the year ahead looks certain – solid earnings growth, two to three rate cuts, higher but stable inflation, and steady economic growth. It’s almost as though the outcome for 2026 has been pre-ordained. If only life were that simple.

All you had to do was watch last night’s Ole Miss/Georgia game to be reminded that even when everyone thinks they know what’s “going” to happen, it’s not uncommon for the opposite to play out. In the week leading up to last night’s game, prediction markets were giving Ole Miss less than a one in three chance of winning. After the game started, the odds for Ole Miss got worse, falling below 20% for much of the game. When the game finally ended just before midnight, though, it was Ole Miss on top by a score of 39-34. Whether it’s in sports, your personal life, or the markets, just because everyone seems to agree on what’s going to happen doesn’t mean that’s what will play out. Expect surprises.

After the weakness to close out 2025, investors are probably surprised to see futures looking so strong this morning. S&P 500 futures are pointing to a 0.57% gain to start the year, while the Nasdaq is on pace for a 1% gain. The 10-year yield is little changed at 4.15% while crude oil is down fractionally at just above $57 per barrel. After a volatile end to 2025, metals have picked up right where they left off last year, but this time on a positive note. Gold is up over 1%, while silver and platinum are up over 4% each.

In Asia, Japan and China were closed, but other major indices in the region traded on a positive note, with Hong Kong up 2.8% and South Korea jumping 2.3%. The only economic indicator of note in the region was South Korea’s manufacturing PMI, which moved slightly back into expansionary territory at a level of 50.1.

European stocks are also positive this morning, with the STOXX 600 up 0.5%, led higher by Italy and Spain with gains of 0.6% each. The gains come despite generally weaker than expected manufacturing PMI readings for the region, where the Eurozone slid further into contraction, and Germany’s reading fell from 48.2 to 47.0.

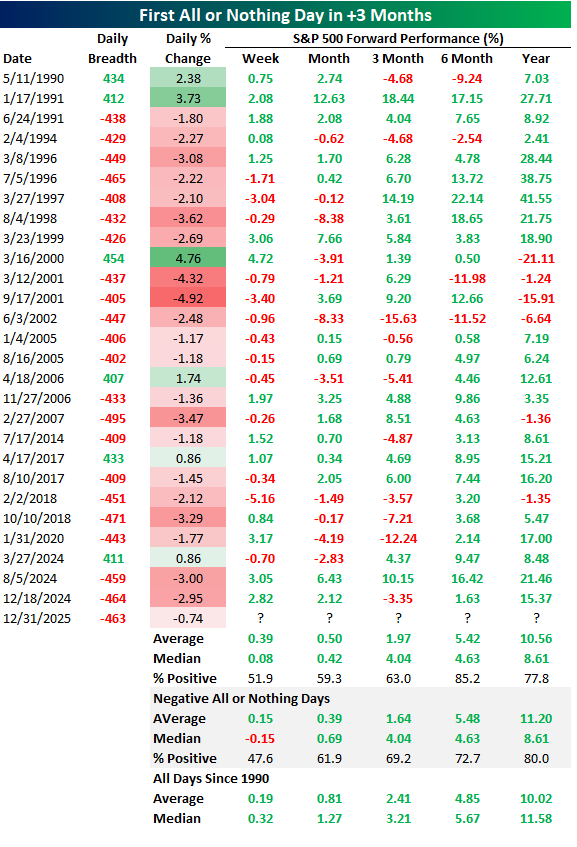

While futures are higher to kick off 2026, 2025 ended like a 500-pound bag of rocks, or more accurately, 482 rocks. The S&P 500 dropped 0.74%, which wasn’t the worst decline considering breadth was exceptionally bad with 482 index members declining versus only 19 rising. We consider an all-or-nothing day when breadth is +/-400, meaning at least 90% of the S&P 500’s constituents rose or fell. Wednesday was the first all-or-nothing day since July 15, when net breadth was -404. As shown in the table below, the first all-or-nothing day in at least three months has typically been followed by gains, but not particularly stronger or weaker than the long-term average. That’s also the case when the first day in at least three months is a ‘nothing’ day like Wednesday was. With that said, in the near term (one week and one month), median returns have been a little bit weaker than all periods after those instances.