Oct 27, 2025

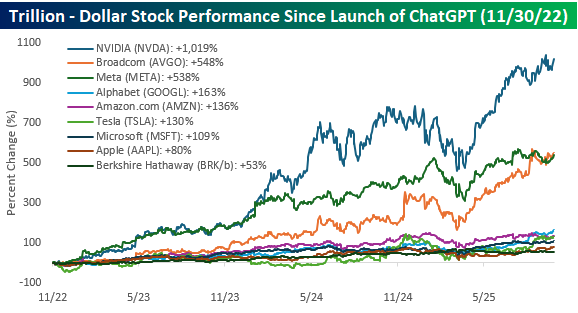

It’s been three days and a month short of three years since the launch of ChatGPT, and companies with any connection to AI have seen their stock prices do well. When ChatGPT first launched, there were four companies with market caps of a trillion or more (Microsoft, Apple, Alphabet, and Amazon.com), but now there are nine, and four of them are in the three-trillion-dollar club!

In the chart below, we show the performance of all nine current trillion-dollar stocks in the S&P 500 since the launch of ChatGPT on 11/30/22. Nvidia (NVDA) has been the obvious leader with a gain of more than 1,000%. When Chat first launched, NVDA’s market cap was less than $420 billion compared to $4.5 trillion now! The next closest stocks in terms of performance – Broadcom (AVGO) and Meta (META) – have barely half the gain of NVDA, but at over 500%, their respective gains have been pretty amazing as well. After these three stocks, though, the gains of the trillion-dollar club look a lot more modest.

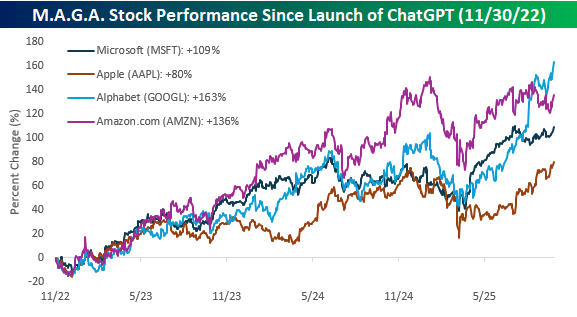

As mentioned above, there were just four trillion-dollar stocks when ChatGPT first launched on 11/30/22, and the performance of the four “M.A.G.A.” stocks, as they were referred to back then, is shown below. When ChatGPT first launched, MSFT was considered one of the biggest winners from AI given its stake in OpenAI, but as the chart above illustrates, its performance hasn’t held a candle to NVDA, AVGO, and even META. Even more surprising, though, has been MSFT’s performance versus the other M.A.G.A. stocks. With a gain of 109%, the only one it’s outperforming is AAPL, which has basically sat AI out.

Early in the AI rally, it was widely assumed that GOOGL had fumbled AI and would forever trail MSFT in the AI arms race. As the chart below illustrates, though, GOOGL’s recent run has put it far ahead of MSFT in terms of performance since the launch of ChatGPT. Whether that leadership continues is an entirely different question, but the fact that GOOGL has taken over in terms of leadership not long after the market crowned MSFT as the AI winner is a market storyline that has played out in different industries and sectors for as long as financial markets have been around. Henry VI said it in another context, but “uneasy lies the head that wears a crown”.

Oct 27, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you could kick the person in the pants responsible for most of your trouble, you wouldn’t sit for a month.” – Theodore Roosevelt

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A flurry of trade deals announced over the weekend and this morning has futures surging, with the S&P 500 indicated to open up about 0.8% and the Nasdaq indicated to rally more than 1%. It should be noted, however, that current levels are off the overnight highs. With most of the announced deals being connected to Asia, that is where the biggest gains were seen overnight as the Nikkei rallied 2.5% while China gained more than 1%. European stocks have been much more subdued this morning as the STOXX 600 is just marginally higher and major benchmarks on the continent trade on either side of the unchanged line.

With investors taking more of a risk on approach, treasury yields are higher, with the 10-year yield moving back above 4% to 4.03%. Crude oil is fractionally lower along with gold as it tries to recover after breaking a streak of nine weekly gains last week. Finally, after a rough go of it in recent weeks, Bitcoin is up again after a strong weekend, taking it back above $115K while Ethereum is up over $4,100.

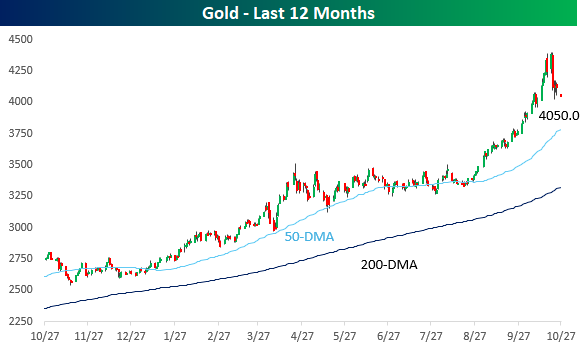

As mentioned above, gold ended a streak of nine straight weekly gains last week during which it rallied more than 25%. Since 1975, it was just the fifth time that gold traded higher for at least nine weeks and the first such streak since August 2020. Of the four prior streaks, only one in 2007 lasted longer (12). Of the four prior streaks, after the first down week that ended the streak, gold continued lower over the following three months three times for a median decline of 4.6%, and a year later it was lower three out of four times as well for a median decline of 7%.

As shown in the chart below, gold’s decline last week was a sharp reversal from record highs hit just last week and was one of the larger drawdowns we have seen in the commodity over the last year. Despite the decline, though, gold remains well above its 50 and 200-DMAs.

Oct 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If everything you try works, you aren’t trying hard enough.” – Gordon Moore

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US stocks are on pace to end the week on a positive note as S&P 500 futures indicate a 0.33% gap higher at the open, while the Nasdaq is up 0.50%. Treasury yields are higher as the 10-year yield is back above 4%, and crude oil remains above $60 with WTI trading up 1%. Gold, on the other hand, is down 1.7% and on pace to end its nine-week streak of gains. Finally, crypto is higher with Bitcoin up 0.6% and back above $111K, while Ethereum gets back up near $4K with a gain of 2.3%.

Overnight, Asia was mostly higher with Japan up 1.35% after declining 1.35% Thursday. For the week, most major indices were up multiple percentage points, although India and Australia only managed modest gains. The tone is less positive in Europe this morning as most major indices experience modest declines, but for the week, they’re all comfortably higher.

We finally got a government-run economic indicator as the BLS summoned workers back into the office to tabulate the September CPI, which came in weaker than expected across the board. While still well above the Fed’s 2% target, it’s moving in the right direction.

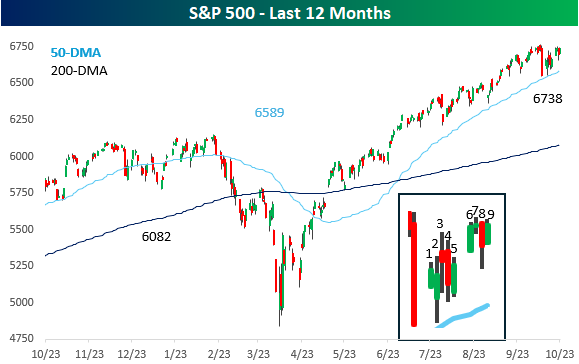

It’s been a while now, but after nine trading days bouncing around within the intraday range from 10/10, the S&P 500 is poised to test the upper end of that range at the open today. If the streak ends, it will be tied for the longest run of days trading within a prior day’s intraday range in at least 40 years. In our Chart of the Day from Tuesday, we covered these prior streaks and how the S&P 500 performed going forward, so make sure to check that out.

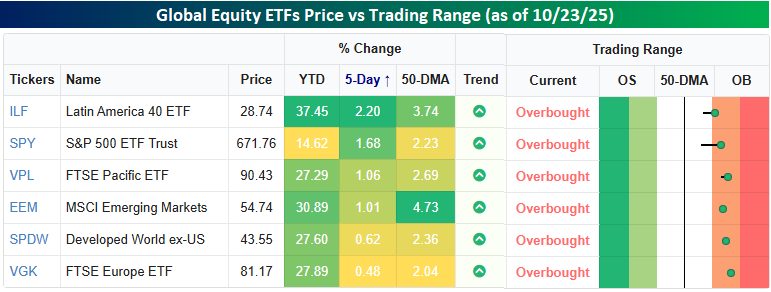

While the S&P 500 has been rangebound for two weeks now, like the rest of the world, it has been a positive week. The snapshot below from our Trend Analyzer shows the performance of various regional global ETFs. As shown, it’s been somewhat of a uniform move with every ETF trading higher to varying degrees over the last week, and all four moving into overbought territory. One of the biggest outliers, though, is in YTD performance. While every other regional equity ETF has rallied at least 27% YTD, the US is up barely more than half that, with a gain of ‘only’ 14.6%.

Oct 23, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want to increase your success rate, double your failure rate.” – Thomas J. Watson, Sr

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We may be starting to sound like a broken record, but once again this morning, futures are little changed with a downside bias, and the government is still closed. With the Fed in blackout ahead of next week’s rate decision, the only data the market has to focus on domestically is earnings. Overall, the pace of reports continues to come in positively with EPS and sales beat rates in excess of 70%. Also on the subject of broken records, it’s now been eight trading days where the S&P 500 has been stuck within the range it traded in on 10/10.

While the government may be closed, Washington is far from quiet, with the latest news being reports that the Trump Administration is in talks to acquire stakes of up to $10 million in various quantum computing stocks, including IonQ, Rigetti Computing, and D-Wave Quantum. Obviously, these stocks are surging in reaction to the news, and as a result have mostly erased yesterday’s declines. It’s worth pointing out, however, that after the gains these stocks have seen in the last couple of years, their market caps are all at or above $10 billion; a $10 million investment works out to less than 0.1%.

Outside of equities, crude oil is surging 5% and back above $60 per barrel after yesterday’s latest round of sanctions against Russian oil companies. Gold is also trying to regroup after the sell-off from the last couple of days, rallying 1.5% and back above $4,100 per ounce, while silver and platinum are both up at least 2.5%. Even Bitcoin and Ethereum have managed to rally more than 1%.

In international markets, Asian stocks were mixed overnight, with the Nikkei falling 1.4% and the Kospi dropping a percent. Hong Kong (0.7%), China (0.2%), India (0.2%), and Australia (0.1%) all managed to finish higher. The tone in Europe this morning is skewed more positive, with the STOXX 600 rallying 0.3% with little in the way of catalysts besides earnings driving the action.

The 10-year yield remains below 4% this morning after trading yesterday at its lowest level since the tariff-tantrum in April. While it wasn’t enough for a 52-week low on an intraday basis, on a closing basis, it was the lowest level since early October of last year. Since peaking at just under 4.6% in May, the 10-year yield has been stuck in a very consistent downtrend channel, and has been moving towards the lower end of that range all month.

Oct 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Women who seek to be equal with men lack ambition” – Timothy Leary

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The post 10/8 range-bound slog looks set to continue for the S&P 500 today as it enters its eighth day in a row of trading within its intraday range from 10/10. S&P 500 futures are essentially unchanged, while Nasdaq futures point to a modest decline. Yesterday’s weakness in gold and other precious metals has continued this morning, with gold down more than 1%, and while the crypto markets had a positive reversal yesterday, they’re giving it all back today as volatility in that space continues.

Overnight in Asia, most indices saw modest declines, although South Korea managed to buck the trend as it seems nothing can keep the Kospi down. European shares are mixed. The STOXX 600 is trading modestly higher on the session, led higher by the FTSE 100 and Spain’s Ibex 35, while Italy is down 0.5%. This morning’s strength in the UK was catalyzed by a much weaker than expected September CPI report, which showed no change in consumer prices relative to forecasts for an increase of 0.2%.

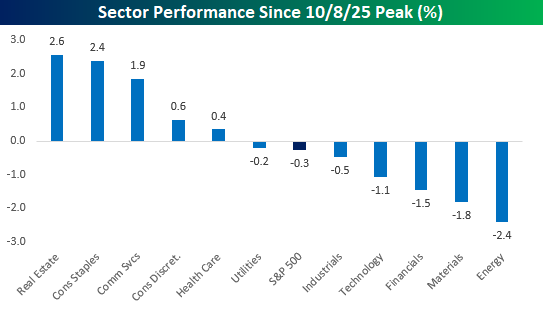

It’s now been two weeks since the S&P 500’s last record high, and while the S&P 500 has seen just marginal declines, some of the moves within sectors have been much larger. As shown in the chart below, Real Estate and Consumer Staples have both rallied over 2% and join Communication Services as the three sectors with gains of over 1%. To the downside, five sectors have declined since the 10/8 high, but four of them are down over 1%, including Energy (-2.4%) and Materials (-1.8%). Technology has also slumped 1.1%, which has acted as the main driver of the index’s decline.

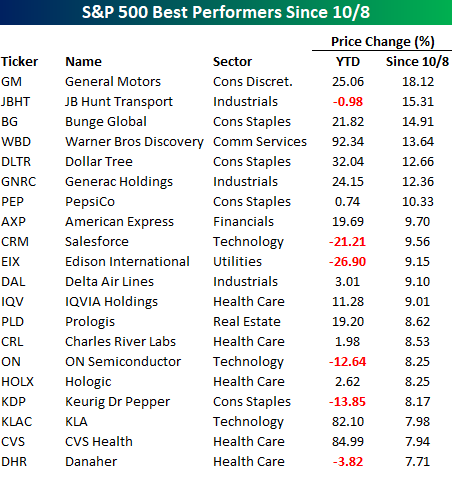

At the individual stock level, it’s been an eclectic mix of winners and losers. Starting with the winners, General Motors (GM) tops the list after yesterday’s post-earnings surge, and it’s one of seven stocks in the S&P 500 that have rallied over 10% since the 10/8 peak. While many of the 20 best-performing stocks in the S&P 500 are handily up YTD, they aren’t exactly the typical winners investors have been used to seeing throughout most of the year. The sector breakdown of these winners further illustrates that trend, as nearly half of the names listed are either from the Health Care (5) or Consumer Staples (4) sectors.

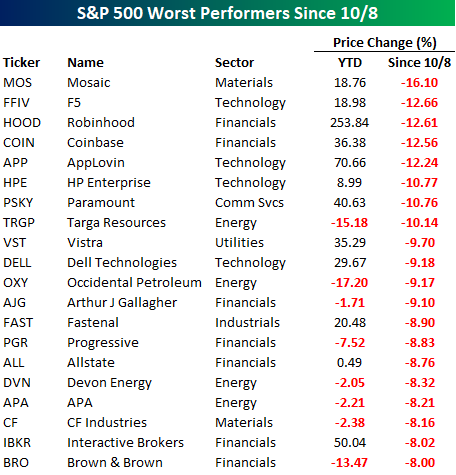

Shifting to the biggest losers, eight stocks in the S&P 500 have seen double-digit percentage declines since the 10/8 peak. Leading the way to the downside, Mosaic (MOS) has declined more than 16%. While many stocks listed have underperformed this year, for stocks like Robinhood (HOOD), Paramount (PSKY), Vistra (VST), Dell (DELL), and Interactive Brokers (IBKR), it has been a pause to potentially refresh.

At the sector level, Financials has been most heavily represented, with over a third of the names listed as concerns in the credit markets have hit some of the names in the sector hard. After Financials, the next most heavily represented sectors are Energy and Technology, with four each.