Dec 22, 2025

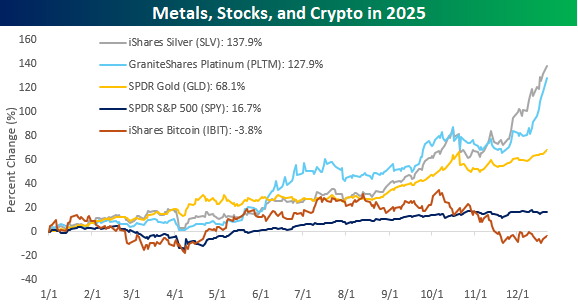

Silver is usually thought of as the award for second place, but during the fourth quarter of 2025, it moved firmly into first place in the precious metals race. Based on prices this morning, the iShares Silver ETF (SLV) has now rallied nearly 138% YTD. For much of the first five months of the year, silver trailed gold and/or platinum. In early June, platinum surged past gold and silver for the lead, but in the last few weeks, silver has taken the lead again with a rally that platinum and gold haven’t been able to match.

In the chart below, we have also included the performance of the S&P 500 (SPY) and Bitcoin (IBIT). The S&P 500’s 16.7% YTD gain looks pedestrian relative to the metals, and Bitcoin’s performance has been an embarrassment. Earlier this year, there was so much hope for Bitcoin on the assumption that President Trump would be the most crypto-friendly President that the country has ever seen. It’s been less than a year so far, so there’s still plenty of time, but at this point, Bitcoin hasn’t lived up to the hype.

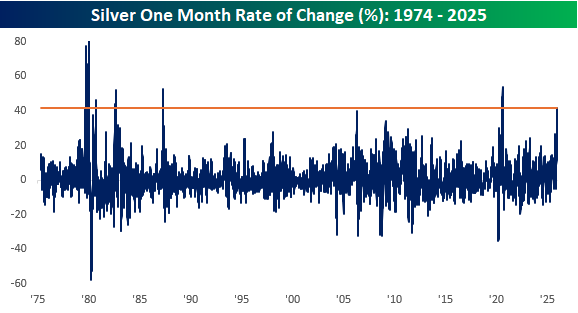

Looking at the chart above, silver prices have really surged over the last month, rallying more than 40%. That’s the largest one-month gain since August 2020. Before that, the only other times, outside of late 1979/early 1980 when the Hunt Brothers attempted to corner the market, that silver experienced similar or larger one-month rallies were in late 2025, early 1987, and September 1982.

Dec 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think the one lesson I have learned is that there is no substitute for paying attention.” – Diane Sawyer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The year is finally starting to wind down as the pace of economic data, earnings results, and analyst actions slows down to a trickle, if at all. This morning, traders are in a buying mood as S&P 500 futures trade 0.4% higher while the Nasdaq is up 0.65%. Bond yields are modestly higher as crude oil jumps 2% following reports that the US has seized another Venezuelan oil tanker. Even with that move, though, WTI still trades below $58 per barrel, so those sub=$3 gas prices should be safe for now.

The real action this morning, though, is coming from the metals markets. Gold and silver are trading to new highs with gains of 1.5% and 2.5%, respectively. Platinum prices are blowing those rallies out of the water, though, surging more than 5% to its highest level since 2008 and within 8% of its record high. Even crypto prices are joining in on the rally to kick off the week as Bitcoin is back above $90K.

Asian stocks had a rough go of it last week, but they’re in the holiday mood to start this week. South Korea led the way higher with a gain of 2.1%, followed by the Nikkei, which rallied 1.8%. Other major benchmarks in the region were also higher, but by less than 1%. Yields in Japan continue moving higher, but the Yen managed to rally.

In terms of holiday cheer, there isn’t much in Europe to start the week. The STOXX 600 is down fractionally, with the UK and France leading the way with losses of about 0.5%.

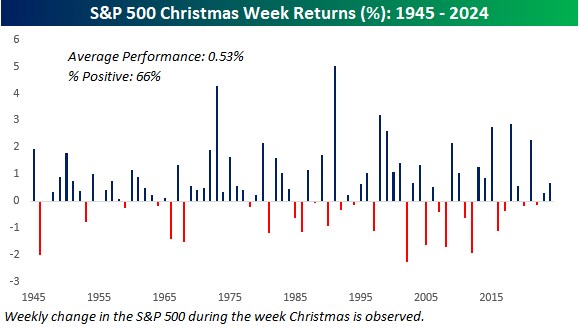

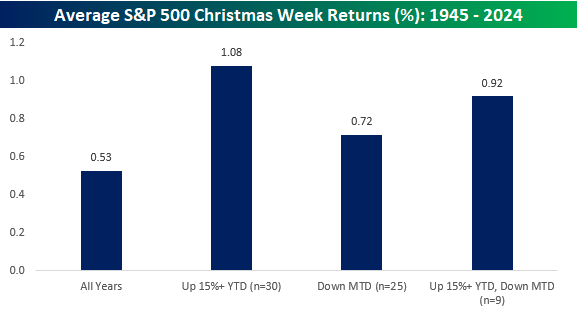

It’s called the most wonderful time of the year, but is it for the stock market? The chart below shows the S&P 500’s historical returns during Christmas week since 1945. For each year, we measure the S&P 500’s performance during the week when the Christmas holiday was observed. For all years since 1945, the S&P 500’s average gain was 0.53% with positive returns 66% of the time. For all one-week periods since 1945, the S&P 500’s average gain was 0.30% with gains 57% of the time, so Christmas week may not be the “most wonderful”, but it’s much better than average. The best Christmas week for the S&P 500 was in 1991, when it rallied just over 5%, while the worst Christmas week was in 2002 (-2.3%).

Looking at different scenarios applicable to this year, in the 30 years when the S&P 500 was up 15%+ YTD heading into Christmas week, the S&P 500’s average Christmas week rally was 1.08%, with gains 83% of the time. There have also been 25 years when the S&P 500 was down MTD heading into Christmas week, and in those years, the S&P 500’s performance was more muted at a gain of 72%, with gains just over two-thirds of the time. Together, there have been nine years when the S&P 500 was up 15%+ YTD and down MTD heading into Christmas week, and in those years, the average gain during the week was 0.92% with gains 78% of the time.

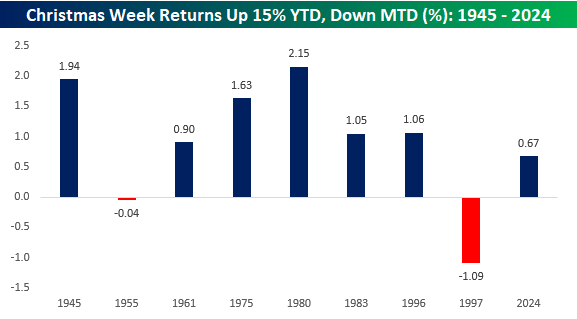

The chart below shows each of the nine other years that the S&P 500 was up 15%+ YTD and down MTD heading into Christmas week. The most recent occurrence was last year when the S&P 500 rallied 0.67% during Christmas week. Before that, the next most recent occurrence was way back in 1997.

Dec 19, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we obtain too cheap, we esteem too lightly: it is dearness only that gives every thing its value.” – Thomas Paine

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are limping into the last trading session of the week with the S&P 500 indicated up by a few basis points while the Nasdaq is indicated 0.15% higher. The 10-year yield is up 3 basis points, but still below 4.15%, and crude oil is up 1%, but still below $57 per barrel. Gold is essentially flat, putting it on pace for a gain of nearly 1% on the week, while Bitcoin is up over 3% as it attempts to erase some of the week’s sharp losses.

The only economic reports on the calendar this week are Existing Home Sales and UMich sentiment at 10 AM. While options expiration and a rebalancing in the S&P 500 could create some volatility, trading is likely to really slow down next week and into year-end

While it was a down week for stocks in Asia, they closed out the week on a positive note. The Nikkei rallied 1% but still finished down 2.6% for the week. China was up 0.4% and was unchanged on the week, while South Korea rallied 0.7% to soften its decline for the week to 3.5%. As expected, the BoJ raised rates 25 bps to 0.75%, which was the highest level in 30 years. While monetary policy in Japan is tightening, investors in China are speculating that the PBoC will loosen policy by lowering the reserve requirement early in the new year.

In Europe, the tone is less positive this morning as equity markets on the other side of the Atlantic snooze into the weekend. The STOXX 600 is down 0.1%, but still up over 1% for the week. Germany is poised to finish the week basically unchanged, while most other country benchmark indices are up over 1%. Inflation data in the region was mixed as German PPI for November was unchanged versus expectations for an increase of 0.1%, while French PPI increased 1.1%.

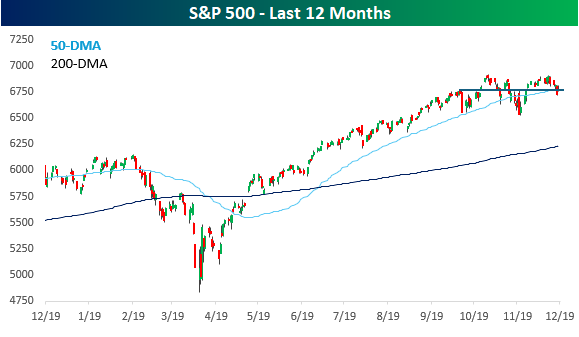

It’s hard to believe that the S&P 500 hit an all-time high a week ago yesterday, and yet as of yesterday’s close, it was barely above its 50-day moving average and essentially at the same levels it was at in early October. As Yogi Berra might say, the stock market is doing great. It’s just not going anywhere.

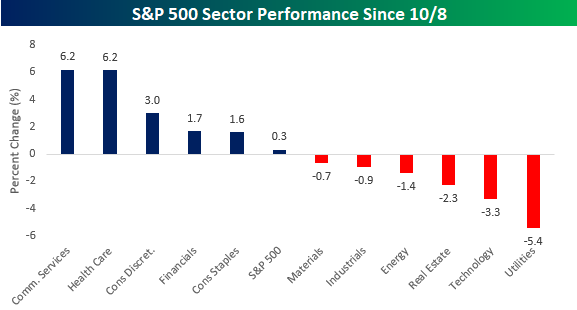

While the S&P 500 hasn’t really gone anywhere, sector performance has been disparate. Communication Services and Health Care are both up over 6%, and another three sectors have outperformed the S&P 500 gain of 0.3%. At the other end of the spectrum, Utilities is down over 5%, but right behind it, Technology has declined 3%. The fact that Technology, which makes up over a third of the S&P 500, has declined over 3%, and the market has treaded water, indicates a broadening of performance. It also illustrates how hard it is for the market to make headway without Technology participating.

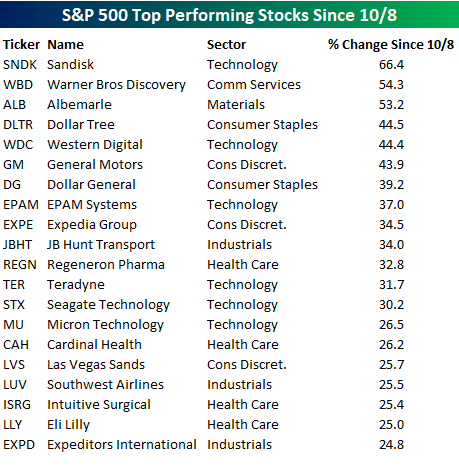

In terms of individual stock performance, of the twenty top-performing stocks in the S&P 500, 19 are up over 25%. Technology is the most heavily represented sector on the list with six, but the strength has been largely isolated to memory stocks, led by Sandisk (SNDK), which has rallied over 60% in just over two months! Besides Technology, six other sectors are represented, including Health Care with four, and Consumer Discretionary and Industrials with three each.

Dec 18, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Our coding teams are realizing productivity gains of 30% or more using agentic AI.” Mark Murphy, CFO Micron

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures got off to a positive start this morning ahead of a busy morning for economic data. Initial and continuing jobless claims came in better than expected, while the Philly Fed report for December came in weaker than forecasts. The number of the morning was CPI, and while there were no m/m readings since October data was not compiled, the y/y reading came in much weaker than expected at 2.7% versus forecasts for 3.1%. Core CPI was weaker at 2.6% versus forecasts for an increase of 3.0%.

In response to the report, futures have added on to their gains with the S&P 500 now indicated to open 0.5% higher while the Nasdaq is up 0.8%. Treasury yields are down about 3 bps across the curve, and crude oil is marginally higher. Gold is down about half of one percent, while Bitcoin is up 2.5%.

Asian stocks were biased to the downside with the Nikkei falling over 1% for the third time this week. South Korea fell 1.5%, but Hong Kong and China were both up marginally. In Europe, investors are more optimistic as the STOXX 600 trades up 0.3%. It’s been a busy morning for central bank announcements as the ECB left rates unchanged, and the BoE cut rates by 25 bps in a 5-4 decision.

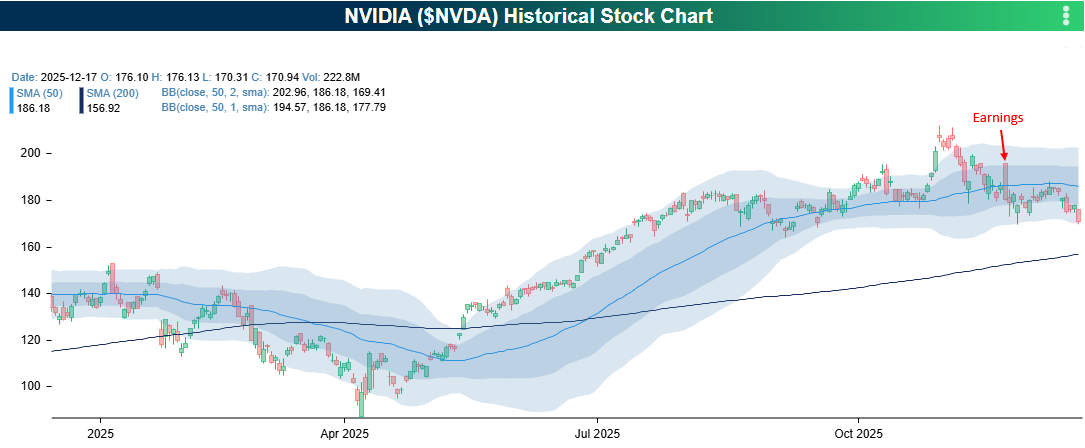

There’s obviously been tons of hype related to AI, and the increases in productivity that it promises. That’s why stocks like Nvidia (NVDA) and many of the hyperscalers have done so well. Moving forward, investors will increasingly demand to see concrete examples across the economy of productivity boosts from companies using AI. Last night’s earnings call from Micron (MU) provided one of those examples when the company’s CFO noted that its programming teams have seen a 30% boost to productivity from using AI.

That’s good to see, but it’s not why MU’s stock is trading up nearly 14% in the pre-market. Last night, the company reported one of the more impressive triple plays we’ve ever seen. While EPS beat expectations by over 20% and revenues were 5% ahead of forecasts, the jaw-dropping aspect of the report was the guidance, as the company sees next quarter’s revenues exceeding consensus forecasts by at least 25%, and they raised EPS guidance by at least 75%. MU’s stock was up 40% in the three months leading up to the report, so investors were expecting a strong report, but the results were still impressive.

MU’s double-digit percentage pre-market gain has investors breathing a sigh of relief, but you can’t fault anyone for being a little cynical after seeing how some other AI-related stocks recently performed in reaction to what, at face value, looked like impressive reports.

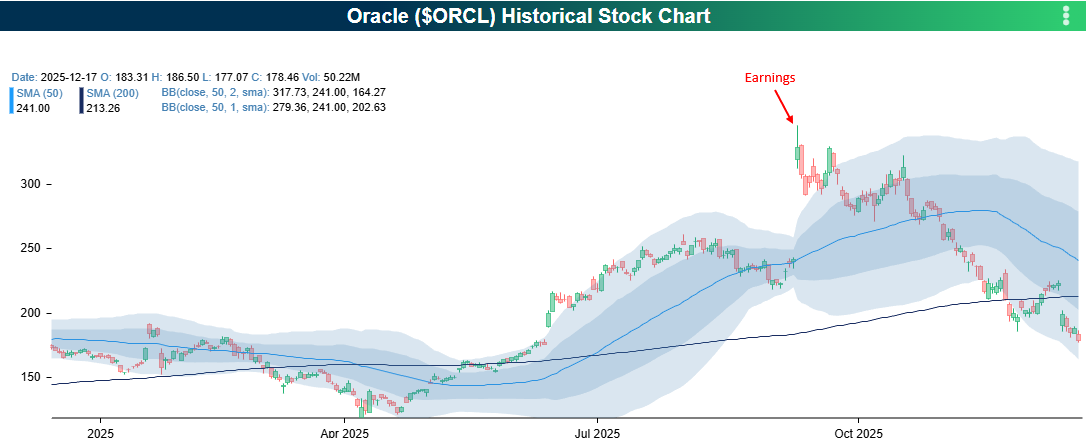

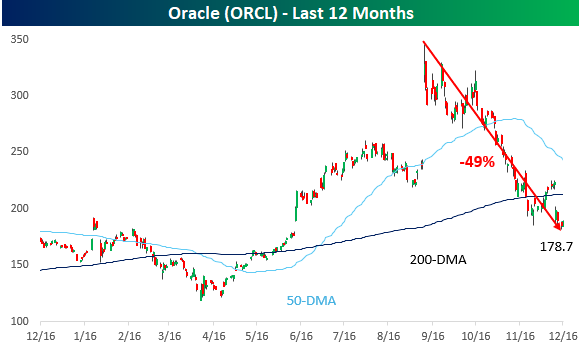

It started with Oracle (ORCL) in September. After reporting earnings after the close on 9/9, the stock traded up an astonishing 36%. Since then, all those gains and more have evaporated as the stock has been essentially cut in half.

On 11/19, Nvidia (NVDA) reported an earnings triple play, and the following morning, the stock gapped up over 5% and took the rest of the market along for the ride with it. Quickly after the market opened, though, shares nosedived nearly 8% intraday to finish the session down over 3%. Since then, the stock is down another 5%.

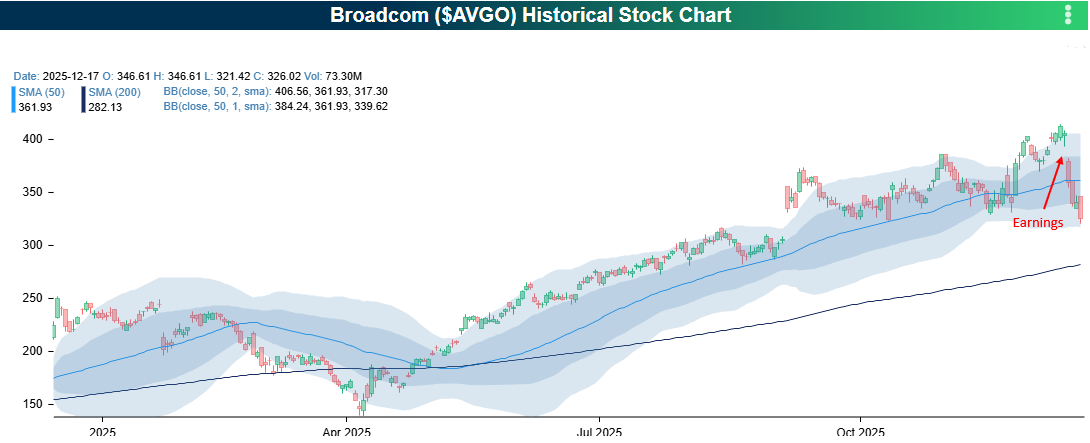

Then, last week, Broadcom (AVGO) reported another triple play, but that wasn’t enough to provide any positive traction in the stock. On 12/12, AVGO gapped down over 5% and is down close to another 15% since that opening trade.

All this is a long way of saying, yeah, it’s great to see MU rallying in reaction to earnings, but unless the stock can hold onto those gains through at least one full session of trading, you can understand if an investor wants to be at least a little skeptical. Fool me once, shame on you. Fool me twice, shame on me. Fool me three times, I’m the fool. Fool me four times, it’s a trend!

Dec 17, 2025

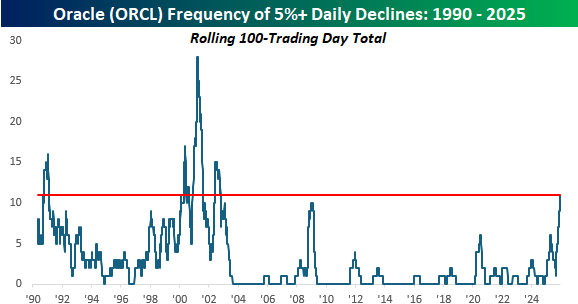

Investor sentiment towards Oracle (ORCL) is taking another hit today on reports from the FT and Reuters that Blue Owl Capital, which typically funds and leases data centers back to Oracle, pulled out of a project in Michigan designed to serve OpenAI. With over $100 billion in outstanding debt, investors continue to grow more concerned about the company’s borrowing to fund its AI ambitions.

Those concerns have obviously manifested themselves in ORCL’s stock price. With this morning’s 5%+ decline, the stock has basically been cut in half from its intraday high in September. Shockingly, even with that decline, the stock is still hanging on to a single-digit percentage gain YTD. It’s not often that stocks fall 50% and remain up on the year.

If today’s declines hold, it will also mark the 11th time in the last 100 trading days that ORCL declined at least 5% in a single session. Even during the Financial Crisis, when it seemed as though stocks were crashing every day, the highest this reading ever got for ORCL was ten. That said, it’s nowhere near the levels (at least not yet) that it got during the bursting of the dot-com bubble in early 2000 through 2002. Hopefully for bulls, Oracle’s recent weakness isn’t living up to its namesake and offering a warning for the rest of the market.