Mar 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great things are not accomplished by those who yield to trends and fads and popular opinion.” – Jack Kerouac

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Money Movers yesterday to discuss the moves in the energy market and their impact on the equity market. To view the segment, click on the image below.

After a mixed session yesterday where the Nasdaq finished up 8 basis points (bps) while the S&P 500 fell 8 bps, US futures are firmly lower this morning, with the S&P 500 and Nasdaq both indicated to open down by about 35 bps. The primary culprit is crude oil, where prices are up over 5% and back above $90 as Iran stepped up attacks on tankers in the Persian Gulf. Energy Secretary Chris Wright was also just on CNBC and noted that the US is not yet ready to escort tankers through the Strait of Hormuz, but could be mobilized later this month. As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy.

With crude oil prices rising, treasury yields are higher again as investors focus on the potential inflationary impacts. Gold prices are essentially flat, silver is up 2%, and Bitcoin is down fractionally but still above $70K.

Stocks were down across the board in Asia overnight, as the Nikkei was down 1.0%, while China’s Shanghai Composite was only down 0.1%, and the Kospi fell 0.5%. Relative to the last two weeks, it was a muted session! Given the spike in crude oil prices and the region’s dependence on energy imports, you could make the argument that it could have been worse.

In Europe, equities are also taking the overnight spike in crude oil prices in stride. The STOXX 600 is down just 0.4%, while Germany is fractionally higher. We’re also starting to see impacts of the conflict showing up in corporate results as UK travel firm On the Beach lowered guidance, citing a sharp slowdown in travel bookings for locations in the Eastern Mediterranean.

On the economic calendar this morning, we just had jobless claims, Building Permits, and Housing Starts at 8:30. Initial claims came in 2K lower than expected, while continuing claims were 1K higher, so from this perspective at least, the labor market remains very well behaved. With respect to the housing numbers, permits were lower than expected (1376K vs 1410K) while starts were much higher than expected (1487K vs 1341K), although much of the strength was due to multi-family units.

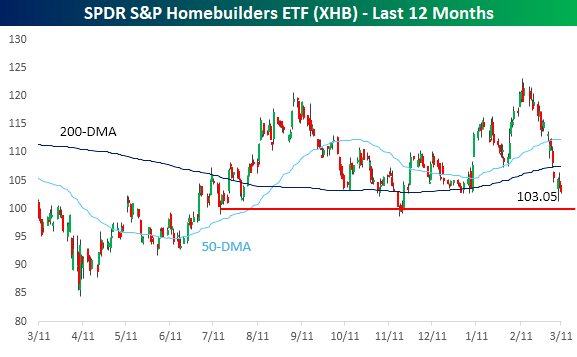

With treasury yields moving higher, it’s been a rough month for homebuilder stocks. The SPDR S&P Homebuilder ETF closed at $121.36 on 2/13, but has since declined more than 15% through yesterday’s close. Those highs in February were enough to push the group to 52-week highs, but the gains for 2026 quickly evaporated, and it’s now close to testing support at the $100 level.

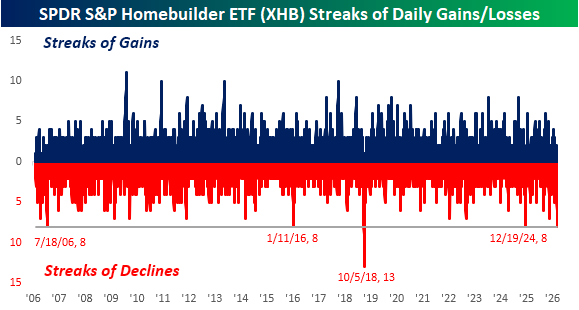

Part of that 15% decline since the February highs includes what is now an eight-day losing streak, which is tied for the longest losing streak in the ETF’s entire history. The last time there was a streak this long was over a year ago in late 2024, and the only longer streak was 13 days ending in October 2018.

Mar 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I attack ideas. I don’t attack people. Some very good people have some very bad ideas.” – Antonin Scalia

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be on CNBC at 11 AM Eastern to discuss markets and today’s CPI.

Futures were in a holding pattern ahead of today’s CPI, with the S&P 500 and Nasdaq both indicated to open down about 0.1% despite Oracle (ORCL) trading up over 10% in reaction to earnings. Treasury yields moved higher ahead of the report, with the 10-year yielding 4.17%, and crude oil was up over 4% to $87 per barrel. Gold and Bitcoin prices are down about 1%.

For Asian equities, the last several days have been something of an all-or-nothing trade where the major averages in the region are either all sharply higher or lower. Last night, there was more dispersion. While Japan and South Korea were both up 1.4%, Hong Kong was fractionally lower, and India declined 1.7%. In South Korea, exports for the first 10 days of March were up 55.6% y/y, with chip exports surging more than 175%. In Japan, PPI fell 0.1% versus expectations for an increase of 0.1%.

In Europe, the move was more uniform, and unfortunately for bulls, it was mostly lower. The STOXX 600 is down nearly 0.5%, with Germany leading the losses with a decline of nearly 1% as German CPI for February rose 0.2%, which was right in line with forecasts.

In the US, the only economic report on the calendar today is February CPI, which given the events of the last two weeks, has become much less pertinent to the market. While it may not be a major focus of the market this morning, CPI was right in line with expectations as headline increased 0.3% m/m and core increased 0.2%

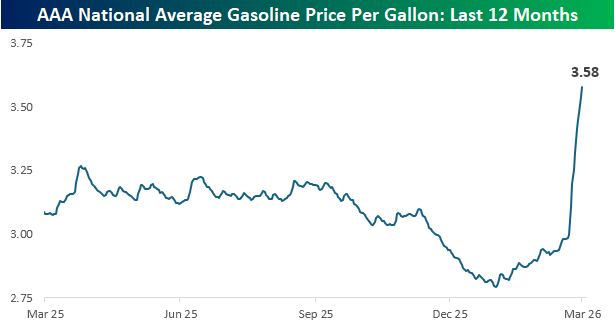

Through yesterday’s close, average prices at the pump have now surged to $3.58 per gallon, which represents a 20% increase this month alone. In the span of two months, prices have spiked from a 52-week and multi-year low to a 52-week high, easily surpassing the prior peak from last spring.

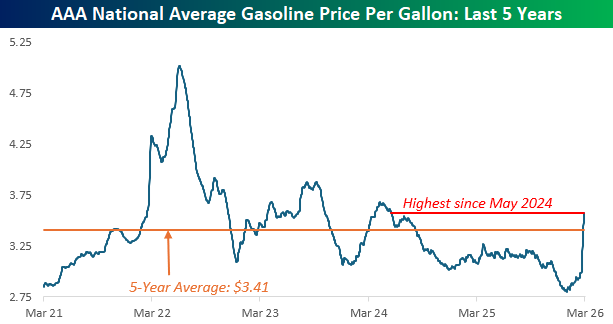

As shocking as the one-year chart looks, taking a longer-term look at crude oil prices shows a less dire picture. Current gasoline prices are now at the highest level since May 2024, but they’re still nearly 30% below the 5-year peak from June 2022, and less than 5% above the 5-year average. That doesn’t make it any easier to stomach, but at least it provides some decent perspective.

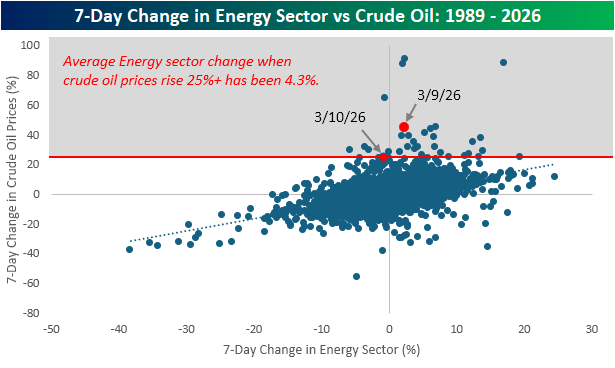

In the seven trading days since the war on Iran started, crude oil prices are up 25%, and as of yesterday, the seven -day change was over 45%. With such large increases, it seems like a disconnect that the S&P 500 Energy sector is up just 2%. The chart below compares the 7-day change in the S&P 500 Energy sector to the 7-day change in crude oil prices. While there has historically been a positive correlation between the two, in periods when crude oil prices have spiked 25% or more, the average change in the Energy sector has been a gain of 4.3%. The implication of those muted gains? The market views these price spikes as temporary.

Mar 10, 2026

This content is for members only

Mar 10, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we’re at a bottom. I really do.” – Mark Haines, CNBC, 3/10/09

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a dramatic reversal late in yesterday’s session on hopes that the war in Iran would be ‘complete’ soon, futures were higher for the overnight session and into this morning. As the opening bell approaches, though, futures have been drifting lower, and all of the major averages are on pace to open fractionally lower. Treasury yields are little changed, and crude oil has been volatile, sitting under $90 per barrel. While that seems low relative to Sunday night, it’s still much higher than anything seen in the months leading up to the war in Iran. Gold prices are up over 1.5%, and silver is surging 5% as it’s currently trading at the same price as WTI! Bitcoin has been quietly grinding higher over the last few days, and this morning, it’s above $70K.

Earnings season is largely in the rearview mirror, but after the close, we’ll hear from Oracle (ORCL), which could be a major catalyst tomorrow for different parts of the AI ecosystem. The only economic reports on the calendar today are small business optimism from the NFIB, which came in weaker than expected (98.8 vs 99.5), and then at 10 AM, we’ll get Existing Home Sales for February.

Asian markets followed the lead of the late-day reversal in US equities and traded sharply higher overnight. It wasn’t enough to entirely erase Monday’s losses, but the Nikkei rallied just under 3% while South Korea surged over 5%. Chinese stocks rallied a more modest 0.7%, and while February exports surged 39.6% y/y, exports to the US declined 17%. Those lost exports to the US were scattered across Europe and Southeast Asia, and many of those likely ended up finding their way into the US in a roundabout way. In Japan, GDP rose 0.3% q/q, which was higher than expected, and in South Korea, growth contracted less than expected.

European stocks are also sharply higher this morning as the US reversal occurred after those markets closed for trading yesterday. The STOXX 600 is up 2.3%, and Germany, Italy, and Spain are all up over 2% as well.

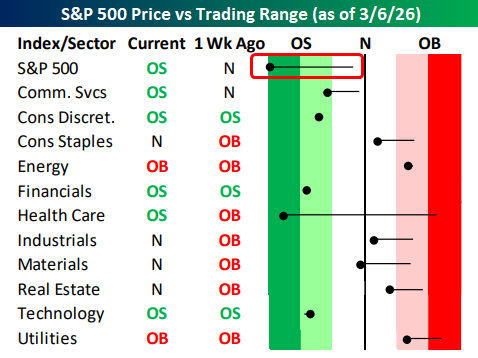

When you looked at page two of the Morning Lineup to see where sectors closed out last week relative to their trading ranges (image below), you may have done a double-take at seeing that the S&P 500 was in ‘extreme’ (2+ standard deviations) oversold territory and more oversold than any sector. In fact, the only other sector in extreme oversold territory was Health Care (after being in extreme overbought territory a week earlier), and just four other sectors were oversold while five were still above their 50-DMAs.

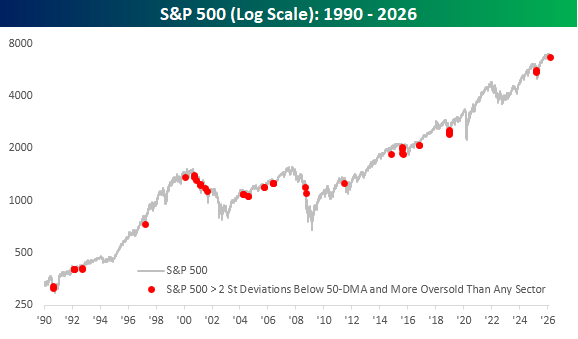

We were curious to see how often it is that the S&P 500 trades in ‘extreme’ oversold territory and is also more oversold than any other sector. Since sector data begins in 1990, there have only been 49 other days when this was the case, and a lot of them occurred during the dot-com bust from early 2000 to late 2001, but as the chart below illustrates, it’s hardly just a bear market phenomenon.

Mar 9, 2026

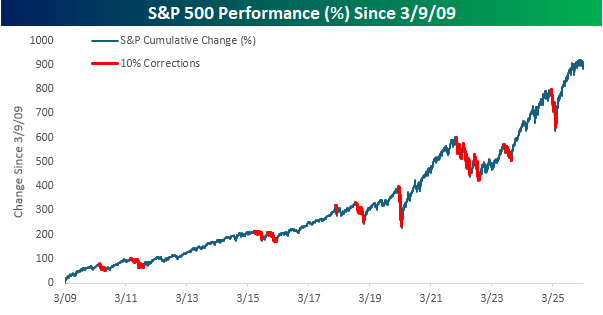

Just how low can stocks go? That was the question posed by the Wall Street Journal on Monday morning, March 9, 2009. Just like this year, March 9th fell on a Monday, following a Friday where the S&P 500 closed sharply lower on economic fears.

That’s where the similarities end. In 2009, the S&P 500 closed below 700 for the first time since 1996; this year, it’s trading not far below 7,000, or roughly ten times higher. Back then, strategists were debating if the index would crater another 27% to reach 500. Having already dropped 56% from its 2007 highs, another leg down felt entirely plausible, but in hindsight, it was the low. Compare that to today: when was the last time you saw mainstream analysts calling for a 27% drop, even with equities right near record highs?

The analysis from that article serves as a reminder of the investor tendency to extrapolate current trends into the future. If stocks are up, they’ll stay up; if they’re sliding, the bottom is always miles away. Analysts often add a ‘countertrend’ hedge in their forecasts just to cover their bases, but take today’s ‘temporary sell-off’ forecasts with a grain of salt. They’re only echoing what the market has been doing. The only way to know for sure is to watch, listen, and let the tape tell the story.

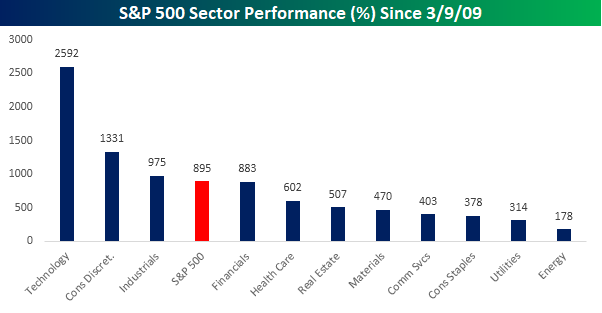

The ride since March 2009 has been incredibly rewarding for those who stayed the course. Since that Monday close, the S&P 500 has rallied 895% (excluding dividends), and more than half of all sectors have risen more than fivefold. Technology has been the top-performing sector with a gain of over 2,500%, followed by Consumer Discretionary, which is up by just over half of that amount. Rounding out the top three, Industrials is the only other sector that has outperformed the S&P 500 since the March 2009 low. While all eleven sectors are higher since March 2009, Energy (178%) and Utilities (314%) have been the worst performers, along with Consumer Staples (378%) and Communication Services (403%), which are the only other sectors that are up less than half as much as the S&P 500.

Have you ever heard anyone say that big gains are right around the corner? Of course not. Looking back at the last 17 years, it seems like the market has done nothing but go up. How many times have you heard someone say that the easy money has been made?

Investing always looks easy in retrospect, but in the moment, it never is. And the last 17 years? The S&P 500 has experienced two bear markets, three other near bear markets (-18%+ from a peak), and a total of 12 different declines of at least 10%. It’s nothing like the period from 2007 to 2009, but there were plenty of moments when putting new money into the market felt like anything but easy. That’s the trick. It’s only easy in retrospect.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up: