Jan 20, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember, your mind is like a parachute: If it isn’t open, it doesn’t work. So keep an open mind!” – Buzz Aldrin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If this is the price we pay for a three-day weekend, maybe we should have kept the market open. It’s looking like a terrible Tuesday for US equities as the S&P 500 is poised to open down 1.4% while the Nasdaq is indicated 1.7% lower. Over the weekend, President Trump escalated his rhetoric towards Greenland and threatened tariffs on European allies if a deal isn’t reached. Today also marks the first anniversary of Trump’s second inauguration, and it’s been eventful to say the least.

Equity indices in Asia were weak, given the declines in US equity futures and the global trade tensions. The Nikkei was down over 1%, but India was the only other country down more than 1%. South Korea’s KOSPI declined 0.4%. Yes, you read that correctly- South Korean stocks had a daily decline for the first time in 2026. The more concerning aspect of the weakness in Asia, though, is in the bond markets where JGB yields are surging to multi-decade highs in their biggest one-day moves since the Liberation Day turmoil last April.

European stocks are much weaker this morning, and in early trading, the STOXX 600 is down 1.3%. Spain is leading the declines with a drop of 1.7%, followed by Germany (-1.6%), and Italy (-1.5%). The weakness this morning stems from President Trump’s announcement over the weekend that he would put tariffs of 10% on the imports of eight European countries beginning on 2/1, which will increase to 25% on 6/1, if no deal is reached on Greenland. Making matters worse are reports that the President will put 200% tariffs on imports of French wine if French President Macron refuses to join the Gaza Board of Peace.

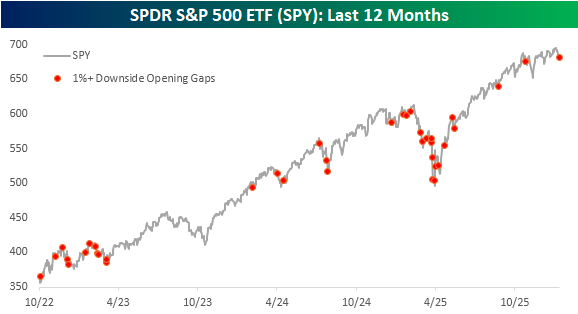

Whenever we see large declines like the market is poised for this morning, it always helps to put the move in perspective. The chart below shows SPY’s performance during the current bull market, and the red dots indicate every other time that SPY gapped down at least 1%. While today’s occurrence is only the third in the last eight months, since October 2022, there have been 37 other occurrences, which works out to an average of once per month.

Today’s gap down in SPY comes as the market has been stuck in a holding pattern for the last several weeks. Based on pre-market trading, SPY is trading right now at the same levels it traded in back in late October.

Jan 16, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“My advisers built a wall between myself and my people. I didn’t realize what was happening. When I woke up, I had lost my people.” – Mohammed Reza Pahlavi

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are bucking a general trend of weakness in international markets and are poised to open modestly higher. S&P 500 futures are indicated to open 0.15% higher, while the Nasdaq is looking at a gain of over 0.4%. Tech is leading the way higher as chip and memory stocks rally, while we’re seeing mixed reactions to earnings from regional banks. Treasuries are selling off as the 10-year yield pushes up near 4.2%, and crude oil is trading up over 1% to just under $60 per barrel. Metals are seeing weakness as gold is down nearly 1% while silver and platinum are down over 4%. Lastly, Bitcoin is up fractionally and above $95K, and Ether pushes up above $3,300.

Asian stocks ended the week on a mixed note but finished the week generally higher. The Nikkei fell 0.3% but finished the week up nearly 4%, while the Hang Seng was down by the same amount and finished the week 2.3% higher. China was the only outlier as the Shanghai Composite also traded down 0.3%, taking its YTD decline to 0.5%. South Korea traded 0.9% higher to close out the week (what else is new) and finished the week 5.6% higher.

Europe appears poised to close out the week on a sluggish note. The STOXX 600 is down 0.2% but still on pace for a weekly gain. France is the biggest laggard this morning as the CAC 40 drops nearly 1%, setting the stage for a weekly decline of 1.4%. The DAX is down close to 0.5% and teetering around the unchanged level for the week. December CPI in Germany was unchanged, which took the year/year rate down to 1.8%.

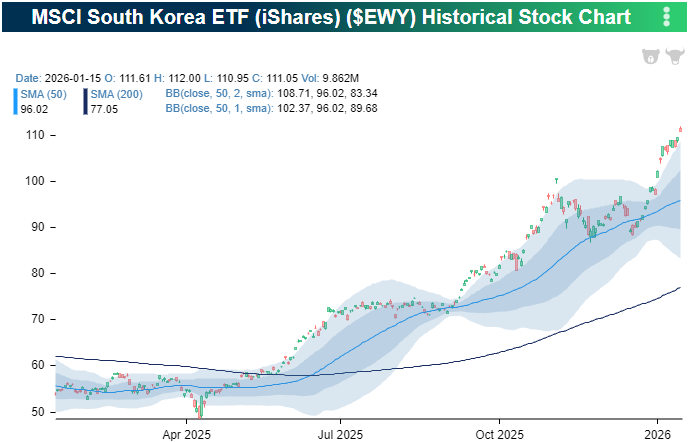

Getting back to the performance of South Korea, 2025 was already a strong year for the country, but it hasn’t skipped a beat so far in 2026. The chart below shows the performance of the MSCI South Korea ETF (EWY), and even after accounting for changes in the currency, it’s been a series of record highs all year.

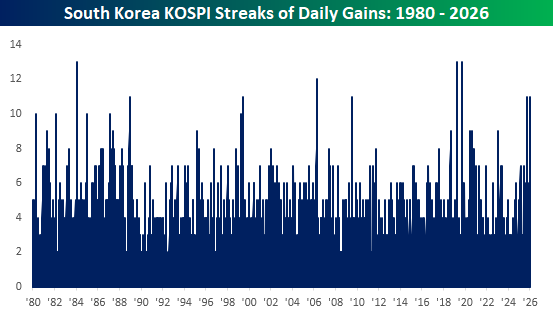

In local currency terms, the KOSPI traded higher on all eleven trading days this year. That’s an impressive streak, but it had another streak of the same length back in September. Before that, though, you have to go back to 2019 to find a streak lasting as long or longer. In fact, that 13-day streak in September 2019 was tied with a streak in April 2019 and February 1984 for the longest on record.

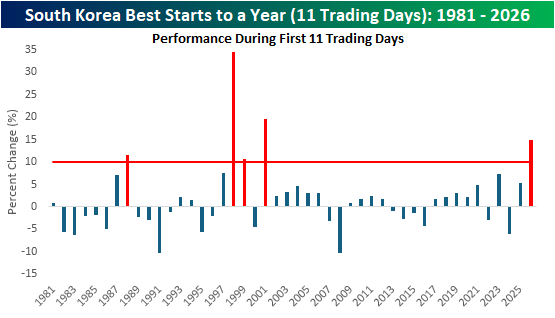

Over its current eleven-day winning streak, the KOSPI has rallied 14.9%, which ranks as the best start to a year for the index over 11 trading days since 2001 (19.6%). Since 1981, there have been four other years when the KOSPI rallied more than 10% in the first eleven trading days of the year. When you think about it, it’s interesting to see how a parallel to this period for the KOSPI traces back to the period starting in 1998, which is also just where we would be based on the comparison between the Nasdaq following the launch of Chat GPT versus its performance following the launch of Netscape in the early to mid-1990s.

Jan 15, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing makes a man so adventurous as an empty pocket.” – ― Victor Hugo, The Hunchback of Notre Dame

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are higher this morning, with the S&P 500 indicated to open 0.4% higher while the Nasdaq, driven by strong earnings from Taiwan Semiconductor (TSM), looks to open up nearly 1%. After weak reactions to earnings from the major banks over the last two days, Goldman Sachs (GS) and Morgan Stanley (MS) reported better-than-expected results but are experiencing muted to modestly negative reactions in their stocks.

Treasury yields are little changed, but at 4.14%, the 10-year yield is very well behaved. After surging above $62 per barrel yesterday as a strike on Iran seemed like a certainty, WTI is down over 4% and back below $60 this morning. Gold and other precious metals are also pulling back, but by much more modest amounts.

In Europe this morning, the STOXX 600 is up 0.5% as shares of ASML rallied more than 5% and saw their market cap exceed half a trillion dollars. Asian stocks were mixed overnight, with the Nikkei falling 0.4% (it can’t go up every day) while China was down a more modest 0.3%. South Korea, however, bucked the trend and rallied 1.6% (apparently, it can seemingly rally every day).

We just got a flurry of economic data, and the results were all stronger than expected. Both the Philly Fed and Empire Manufacturing reports topped expectations, and jobless claims were lower than expected on both an initial and continuing basis. Initial claims were even below 200K. The only fly in the ointment was Import Prices, which rose 0.1% m/m versus forecasts for a decline of 0.2%. In reaction the reports, yields ticked a little higher, and equity futures improved modestly.

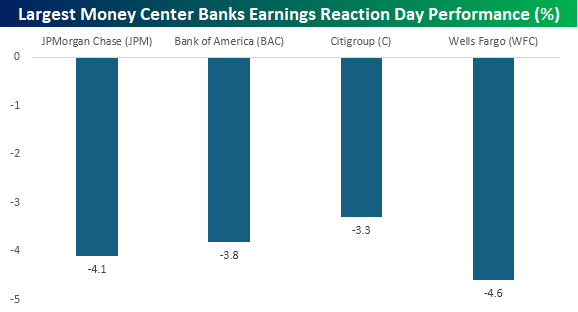

While large brokerage/investment banking-centric firms like Goldman Sachs (GS) and Morgan Stanley (MS) are seeing modest reactions to earnings, the same can’t be said for the largest money center banks, which reported this week. Bank of America (BAC), Citigroup (C), JPMorgan Chase (JPM), and Wells Fargo (WFC) all traded down at least 3% on their reaction days this week. For most, it was their worst earnings reaction day performance in over a year, and for BAC, it was the worst since October 2020!

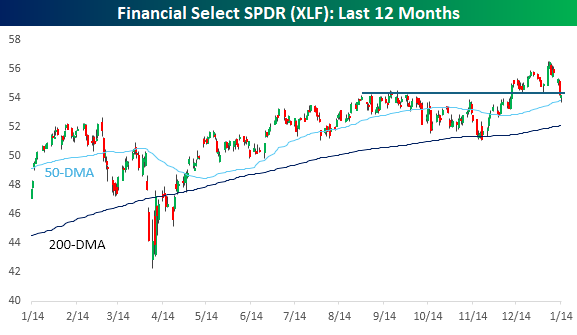

The weakness in the stocks has been a disappointment and a drag on the market this week, but keep in mind that these stocks were trading at record highs last week. They’ve also had to contend with the President’s call for a 10% cap on credit card interest rates. After the initial weakness yesterday, the Financial sector found some support at its 50-day moving average and ended up finishing the day right near the prior highs from last Fall. Provided the weakness eases from here, it’s nothing more than some consolidation.

The major banks are the first companies to report earnings every quarter, so their results and how their stocks react tend to get a lot of investor focus. Therefore, with all four reacting negatively to earnings, it raises the question of whether it’s a flock of canaries warning of bigger problems ahead.

The chart below shows the performance of the SPDR Financial Sector ETF (XLF) since 2000, and the blue dots indicate every time that all four money center banks declined on their earnings reaction days in the same earnings season, while the red dots indicate each time all four stocks declined at least 1%. There have been 14 other times that all four stocks declined on their earnings reaction day in the same earnings season, but there have only been three earnings seasons when all three declined 1%. Of those three, the only time all four stocks declined more than 3% was in April 2020 when the economy was shutdown from Covid! So, it’s uncommon to see all four stocks simultaneously react so poorly to earnings.

Jan 14, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“While any number of risks continue, we are bullish on the U.S. economy in 2026.” -Brian Moynihan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey appeared on Making Money with Charles Payne yesterday to discuss the markets in the post-Covid world and what to expect in 2026. To view the segment, click on the image below.

After a modestly negative Tuesday, futures are trading on the back foot once again this morning. S&P 500 futures are down 0.36% while the Nasdaq is even weaker, indicated to open down by 0.5%. Oil prices are higher as traders eye the simmering tensions in Iran and anticipate a possible disruption to supplies from the country. That’s also translated to a flight to safety trade in gold and other precious metals. Gold is up 1%, silver is up over 5%, while platinum is up 3%. A few weeks ago, a lot of traders thought these moves were getting long in the tooth, but those teeth now look like fangs. Even crypto assets have caught a bid in recent days as Bitcoin is back above $95K and Ether is up near 3,300.

After yesterday’s tame CPI, we just got PPI along with Retail Sales. PPI was a strange report as the m/m numbers were either inline with or weaker than expected, but the y/y readings came in much higher than expected at 3% compared to forecasts for 2.7%. These are hotter than expected inflation readings, but PPI is a volatile report. Retail Sales, also released at 8:30, were better than expected. The only other report on the calendar is Existing Home Sales at 10 AM, and given the lower mortgage rates recently, we could see some strength in that report.

The pace of earnings is also starting to pick up as Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC) all reported results this morning. All three companies exceeded bottom-line forecasts, while WFC was the only one to report weaker sales. As a result of its revenue miss, WFC is trading down about 2% while the other two stocks are hugging the flat line.

In Asia overnight, it was a mixed session. Japan extended its streak of 1%+ daily moves to seven with a gain of 1.5%. China was down modestly (-0.3%), while South Korea was up 0.7%. In Europe, there’s been little movement so far this morning. The STOXX 600 is basically unchanged as most major benchmarks in the region are marginally higher, but modest weakness in Germany weighs.

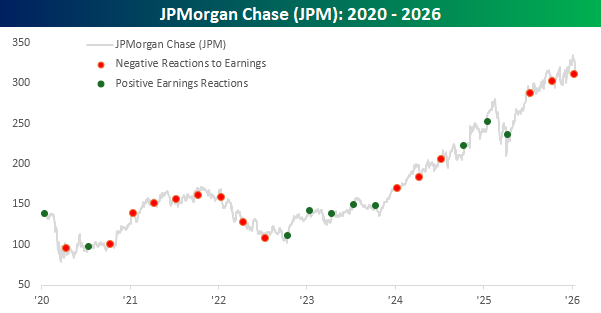

Yesterday’s 4%+ decline in shares of JPM ranked as the eighth most negative reaction to earnings for the stock since at least 2001 and the weakest since April 2024. The stock’s negative reaction to earnings raised some concerns surrounding the stock as well as the broader market, but as we noted in yesterday’s COTD, JPM’s reaction to earnings isn’t exactly a great bellwether for broad market. They’re not even a great bellwether for the stock’s future performance.

The chart below shows the stock’s performance since the start of 2020, and the red and green dots represent each of the company’s earnings reports since then. Red dots indicate days when the stock had a negative one-day reaction to earnings, while green dots indicate positive reactions. Yesterday was the third straight quarter that JPM had a negative reaction to earnings, but as the chart illustrates, the prior two weak reactions weren’t an especially ominous signal as the stock hit new all-time highs following each of them. JPM had a similar streak in 2024, and once again, between each of them, the stock hit all-time highs. From late 2020 through mid-2022, there was another extended streak of eight straight negative reactions, and while the stock held up well early on in that streak, towards the later stretch of that streak, the stock finally rolled over. All in all, though, a weak one-day reaction has tended to be a weak one-day reaction and nothing more.

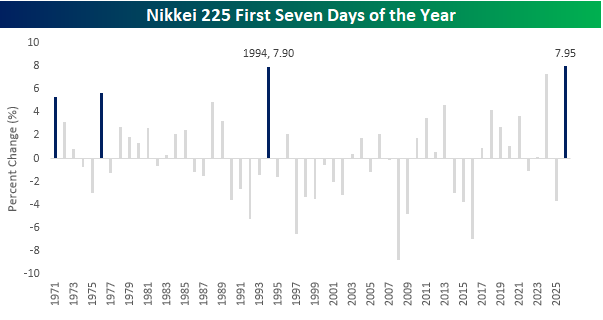

Moving on from JPM to Japan, last night’s rally in the Nikkei extended an impressive run to start the year. After just seven days of trading, the Nikkei is up 7.95%, which ranks as the best start to a year for that index since at least 1971. Before this year, the record was in 1994 when it rallied 7.9% in the first seven trading days. Besides 1994, the only other years that the Nikkei rallied more than 5% in the first seven trading days of the year were 1971, 1976, and, most recently, in 2024.

Jan 13, 2026

This content is for members only