Aug 7, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, it’s a full report that starts off with a look into the intraday reversals experienced today (page 1). We then recap a busy day of macro happenings including productivity and jobless claims (page 2), Fed appointments (page 3), and the 30-year bond auction (page 4). We then pivot over to earnings (pages 4 and 5) before switching back to economic data with recaps of the NY Fed’s consumer survey (pages 6 and 7). We cap off with a look into Treasury allotment data (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Aug 7, 2025

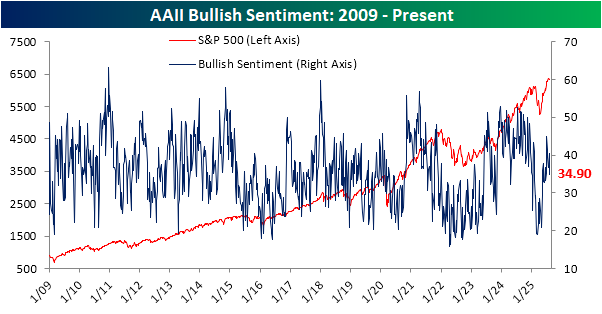

The equity market’s rally has hit a bit of a snag since late July, although the S&P 500 is far from having collapsed as it remains within a couple percentage points of record highs. Nonetheless, sentiment has taken a hit. Bullish sentiment according to the weekly AAII survey peaked in the first week of July at 45%. Since then, it has fallen in four of the five weeks with the latest print of 34.9% the lowest of that stretch. That is only the lowest reading since the week of June 18th when it fell to 33.2%.

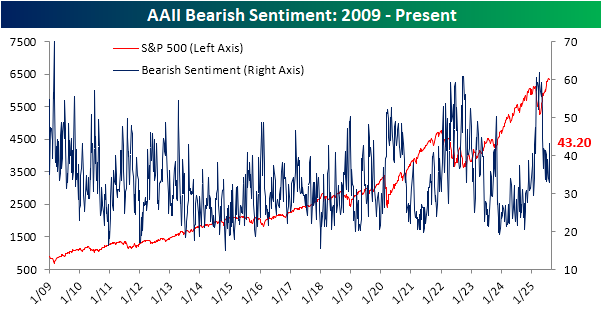

The drop in bulls corresponds with bearish sentiment picking up. Bearish sentiment has seen a more substantial increase, rising from 33% last week to 43.2% this week. That is now the highest reading for bears since the week of May 15, and the 10.2 percentage point leap week over week was the largest increase since the last week of February.

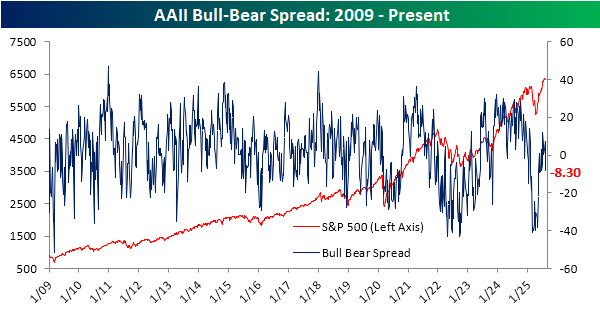

As shown below, the spread between bulls and bears has dipped back into negative territory and is at its lowest level since mid-May.

Aug 6, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of recent Fed speakers and whether each one have given hints of dovishness or hawkishness (page 1). We then cap off with a look at the latest earnings (pages 2 and 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!