Sep 16, 2025

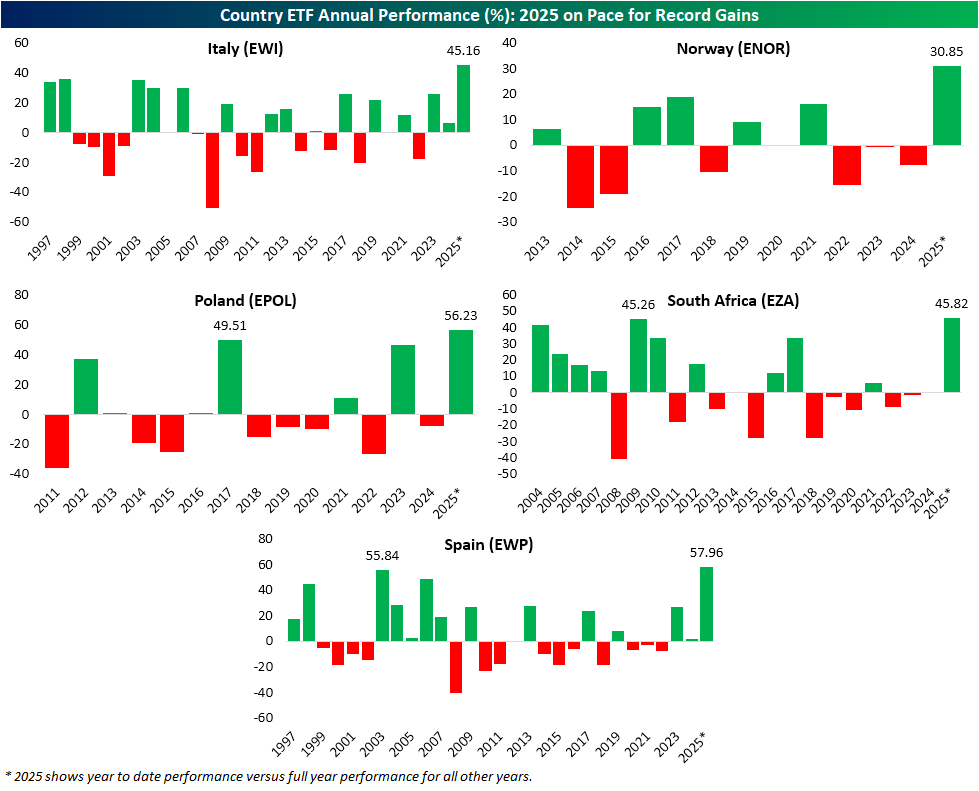

Now in the home stretch of Q3, international stocks have had a banner year in 2025. Whereas the United States’ S&P 500 (SPY) is currently up 12.7% year to date, the MSCI All World Ex. US ETFs (ACWX) have gained well over 24% in that same span. Looking at individual country ETFs in the iShares MSCI family, there have been some monumental winners. For example, Italy (EWI) is up over 45% on a year to date basis. That puts it on pace for the ETF’s largest annual gain on record (it began trading in March 1996) if it holds. The ETF tracking Spain (EWP) has similarly been around since the late 1990s, and its 58% gain this year narrowly beats the 55.8% gain observed in 2003 for its best year on record. Elsewhere in Europe, Norway (ENOR) and Poland (EPOL) are likewise sitting on what would be record gains, although those ETFs have much less extensive histories of a little more than a decade. Finally, we would note that outside of Europe, there is one other country whose tracking ETF is looking for a record. That is South Africa (EZA) which is currently up 45.8%. While that is in fact looking to be a record annual gain, it’s by a much more narrow margin than the others. In 2009, EZA rose 45.3% which is only 50 bps of underperformance relative to this year.

Sep 16, 2025

Log-in here if you’re a member with access to the Closer.

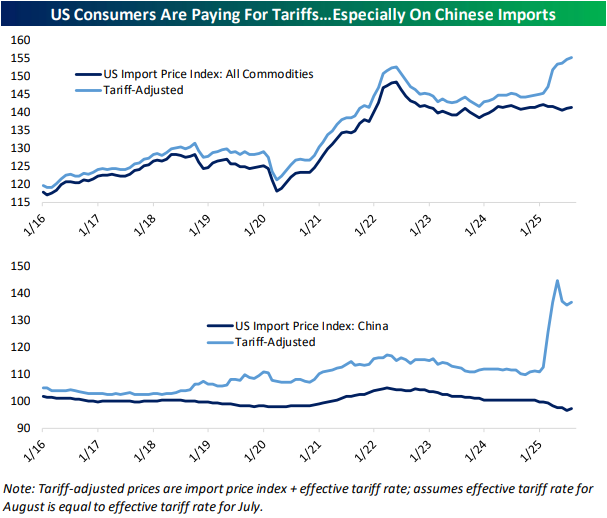

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at how retail sales have outpaced inflation (page 1) before checking in on various other releases of the day including GDP tracking, homebuilder sentiment, heavy truck sales (page 2), and NY Fed service data (pages 2 and 3). We then dive into tariff effects on trade prices and the dollar (page 4). We also include a look at the dollar versus a handful of currencies (page 5) before finishing with a check up on international market performance (pages 6 and 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Sep 15, 2025

Log-in here if you’re a member with access to the Closer.

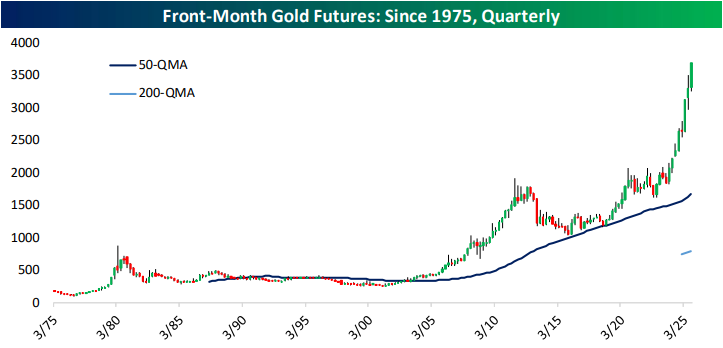

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look into the rare disconnect of extreme overbought stock prices on weak breadth (page 1). We follow up with a rundown on the rough go for farming (page 2) including farm employment and ag prices (page 3). We then provide a technical checkup on gold (pages 4 and 5) before pivoting over to the latest positioning data (pages 6 and 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Sep 11, 2025

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look into the diverging readings in sentiment gauges (page 1). We then look over some fundamentals of insurance stocks (page 2) before switching to a slew of corporate commentary we have gotten in recent days (pages 3-5). Turning over to macro data, we then review the latest CPI release (pages 6 and 7), the latest Z1 report out of the Fed (page 8), and wrap up with a glance at the strong demand for US Treasuries on the primary market (page 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!