Oct 30, 2025

Log-in here if you’re a member with access to the Closer.

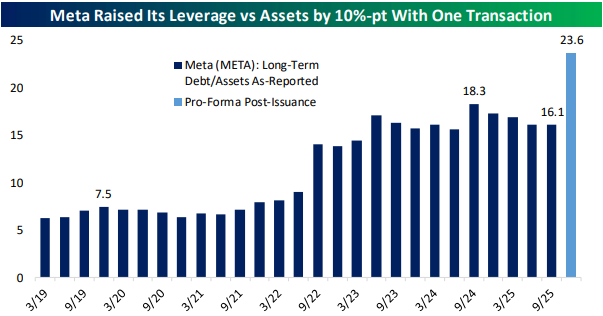

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a note of Meta (META) making a monster bond offering (page 1) in addition to other AI related credit market insights (page 2). We then review the triggering of the Hindenburg Indicator (page 3) followed by a recap of the latest earnings (pages 3 and 4). We cap off with a dive into the latest housing inventory data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Oct 29, 2025

Log-in here if you’re a member with access to the Closer.

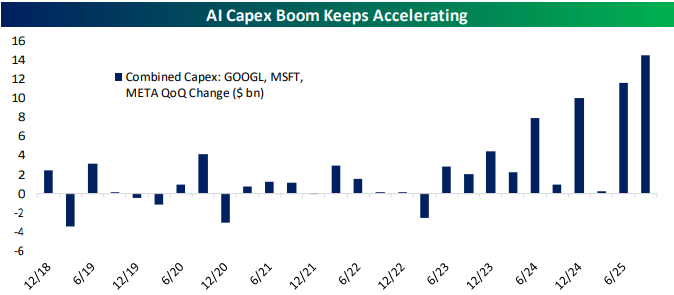

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of today’s FOMC meeting including an evaluation of Powell’s comments in addition to CBO forecasts of the effects of the government shutdown (page 1). We then switch over to a rundown of the latest earnings including results of the first mega-caps like Alphabet (GOOGL), Meta (META), Microsoft (MSFT), and more (pages 2 and 3). We then finish with an update on the changing trends for intraday trading on Fed days and the massive underperformance of equal weight equities over the past couple of sessions (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Oct 28, 2025

Log-in here if you’re a member with access to the Closer.

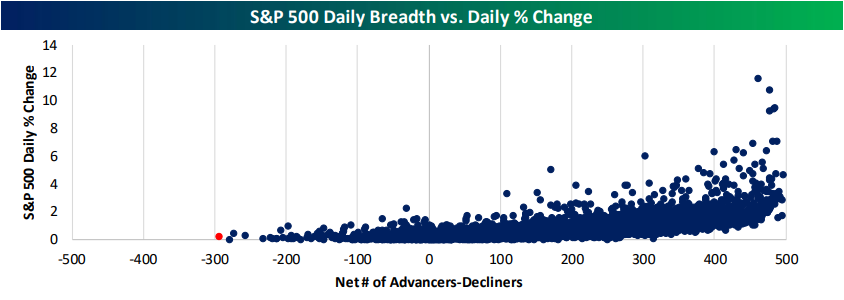

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we cover how since 1990, the S&P 500 has never had an up day with weaker breadth than today. We start out by covering this price and breadth divergence (page 1) followed by a look into volatility (page 2). After an earnings recap (pages 2 and 3), we dive into the latest consumer confidence figures (page 4) in addition to regional Fed manufacturing and service data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!