Sep 13, 2022

Log-in here if you’re a member with access to the Closer.

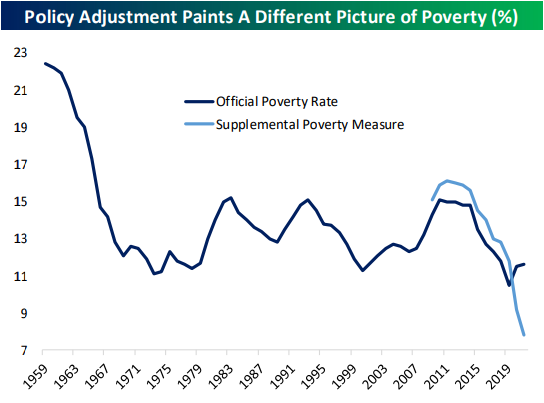

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight with a look at what current WTI pricing means for SPR as well as the dramatic Fed repricing after today’s CPI print (page 1). We then take a dive into said CPI report (page 2) followed by a rundown of the strong demand at this afternoon’s long bond reopening (page 3). Afterward, we look at the US Census’ Annual Social and Economic Supplement of the Current Population Survey (page 4 – 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Sep 13, 2022

COTD Bullet Points:

- The past week (before Tuesday) has seen outright impressive breadth from the S&P 500 as the 5-day advance/decline line has risen to one of the highest levels of the past decade.

Chart of the Day:

Although equities are pulling back sharply in the wake of the CPI release, leading into today the S&P 500 had taken a straight shot higher since coming back from the Labor Day holiday with the index moving higher each day save for last Tuesday. Even more impressively, it wasn’t just a handful of FANG-type mega caps driving the index higher. Breadth has been impressively strong. Typically, we track short-term breadth using the 10-day advance/decline (A/D) line which we update daily in our Sector Snapshot. While that line was basically neutral heading into today, the 5-day A/D line was at the extreme side of historically positive readings. Reaching a reading of 52.8% as of Monday’s close, the reading ranked in the 99.7th percentile of all days since 1990 when our data begins. As for some other most recent examples of breadth reaching such extended levels, there have been two occurrences in the past year: one near the end of 2021 and one this past May.

To read the rest of today’s Chart of the Day as well as gain access to our other reports and tools, start a two-week trial to Bespoke Premium.

Sep 12, 2022

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at how S&P EPS estimates have shifted (page 1). Ahead of tomorrow’s CPI release, we then provide a look at the volatility on CPI release days (page 2). Next, we dive into the latest inflation expectations data from the NY Fed (page 3) followed by a recap of today’s 10 year reopening and 3 year note auction (page 4). We finish with a rundown of the latest speculator positioning data (pages 5-7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!