Dec 30, 2025

Log-in here if you’re a member with access to the Closer.

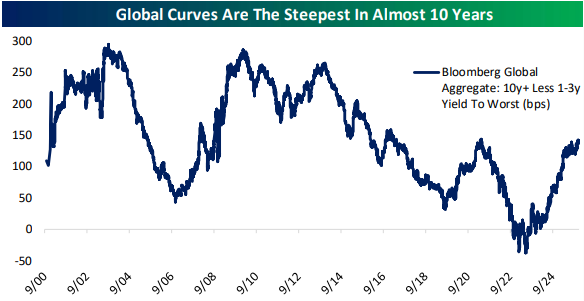

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a recap of fixed income markets in 2025 (pages 1 – 4). We then show the lack of volatility in today’s session (page 5) before closing out with an update on home prices and the Dallas Fed’s service activity data (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Dec 29, 2025

Log-in here if you’re a member with access to the Closer.

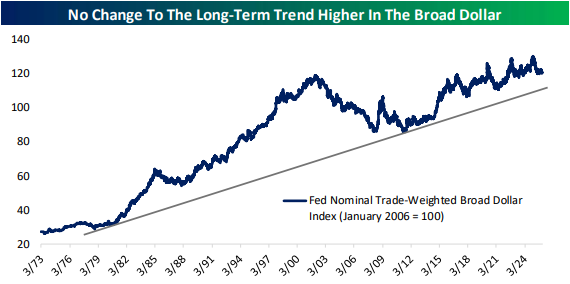

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after last week’s recap of commodities in 2025, we give a review of currency markets (pages 1 – 3). We also check up on our Five Fed Manufacturing Composite (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Dec 23, 2025

Log-in here if you’re a member with access to the Closer.

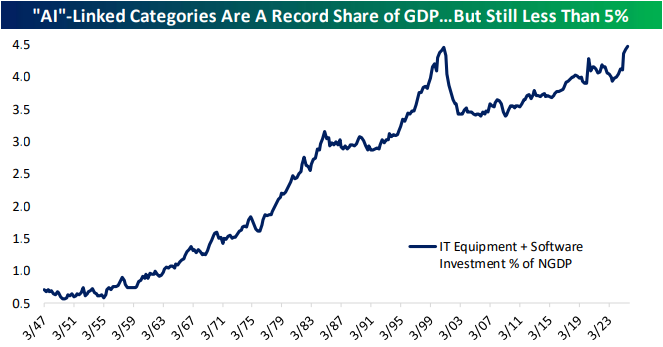

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with an in depth look at the latest GDP figures including a dive into AI impacts on the number (pages 1-2) in addition to an update on some of the latest employment metrics according to ADP (page 3). We then turn over to an update to our Five Fed Manufacturing Composite (page 4) before closing out with a rundown of the latest durable goods figures (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Dec 22, 2025

Log-in here if you’re a member with access to the Closer.

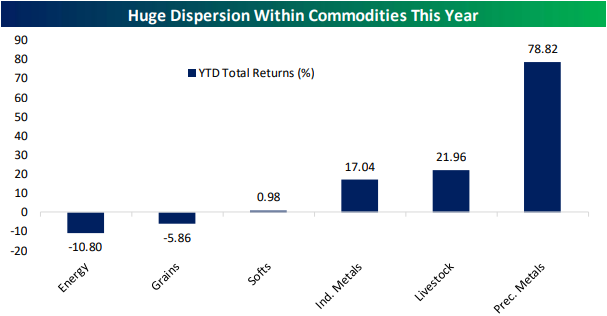

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, as the year winds down to a close, we provide a recap of commodity performance in 2025 including looks at broad commodity indices (page 1), the dispersion between various commodities (page 2), and finally, energy, precious metal, and cattle prices (page 3). We round out tonight’s note with an update on Treasury allotment data (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!