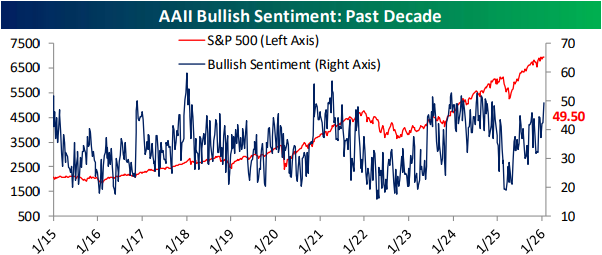

Jan 15, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with some commentary on the midterms (page 1) and the Health Care industry (page 2). Next up, we give an update of our Five Fed Manufacturing Composite (page 3) and check in on jobless claims (page 4). We then review the 52-week high in sentiment (page 5) before rounding out the report with a look at the resurgence of memory prices and related stocks (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

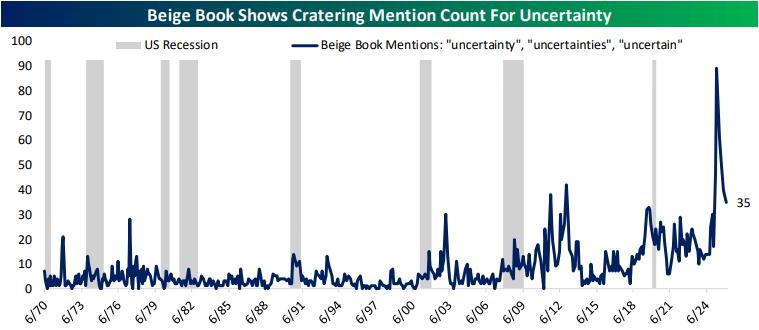

Jan 14, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a review of the rapid rise of tin prices (pages 1 and 2). We then give a quantitative look at the Beige Book (page 3), and follow up with recaps of all other data of the day including the current account and retail sales (page 4), existing home sales (page 5), and PPI (page 6). We finish out with Brookings Institute estimates for immigration (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

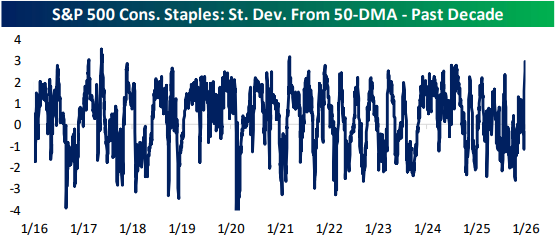

Jan 13, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a rundown of the latest CPI release (pages 1 and 2) followed by a checkup on new home sales (page 3). Next up, we take a peak at the performance of the US dollar and Oracle (ORCL) (page 4) before finishing with a look at the surge in Consumer Staples stocks (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!