The Closer – Another Dose of Fedspeak, Auto Assemblies Surge, Services Slump – 5/16/23

Log-in here if you’re a member with access to the Closer.

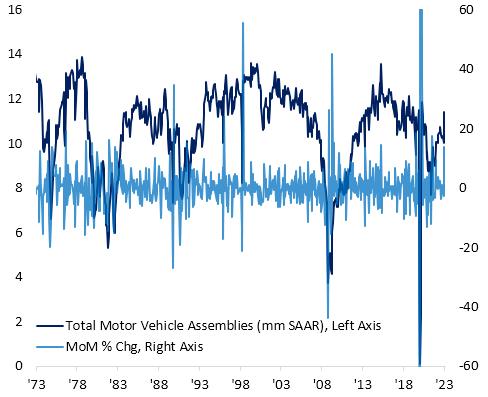

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at another busy day of Fedspeak (page 1) followed by a recap of industrial production numbers (page 2). We then dive into service sector (page 3) and credit availability data (page 4) from the New York Fed.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 5/16/23

This content is for members onlyBespoke Stock Scores — 5/16/23

This content is for members onlyHomebuilders Sentiment and Stocks Still On the Rise

As we noted last week on the release of the latest mortgage purchase data, housing activity appears to have finally stabilized after plummeting earlier in the tightening cycle. That improvement in housing markets is flowing through to builders as this morning’s release of homebuilder sentiment from the NAHB rose to 50 versus the expectation of it remaining unchanged at 45. While the index still has a long way to go to get back to pre-pandemic levels, let alone the record highs from the first two years of the pandemic, in May it hit the highest level since last July.

The higher reading in the headline index was a result of improvements across the board, including increases in present and future sales and traffic. As for regional sentiment, homebuilders have gotten more optimistic across most of the country. Everywhere save for the Northeast have seen steady improvements to homebuilder sentiment over the past several months. As for the Northeast, that is not to say sentiment has not improved. The reading has rebounded off of the worst levels but remains below the recent highs of 46 from February and March.

Homebuilder stocks continue to be even more impressive. Proxied by the iShares Home Construction ETF (ITB), homebuilders have been trading in a steady and uninterrupted uptrend. In fact, the ETF has been overbought every day for a month now.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.