Sep 10, 2025

As of mid-day, Oracle (ORCL) is trading up 38% in reaction to its quarterly earnings release after the close yesterday. Since the start of 2020, there have been more than 47,000 individual earnings reports across US stocks, and only 126 of those reports resulted in a one-day share price jump of 38% or more. Oracle is set to make it 127 today. While most stocks that jump 38% in a day have smaller market caps, Oracle is doing it with a market cap that’s now nearing $1 trillion.

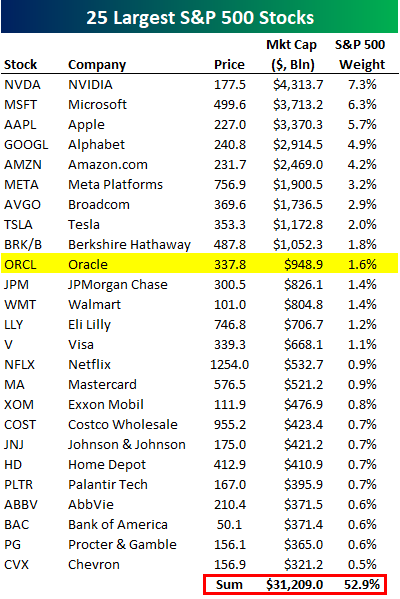

As shown below, Oracle’s gain today has propelled it up to the 10th largest stock in the S&P 500 with a market cap of $949 billion. It needs to gain another 5% or so to reach the $1+ trillion market cap club.

The 25 largest stocks in the S&P now comprise roughly 53% of the S&P 500 with a combined market cap of just over $31 trillion.

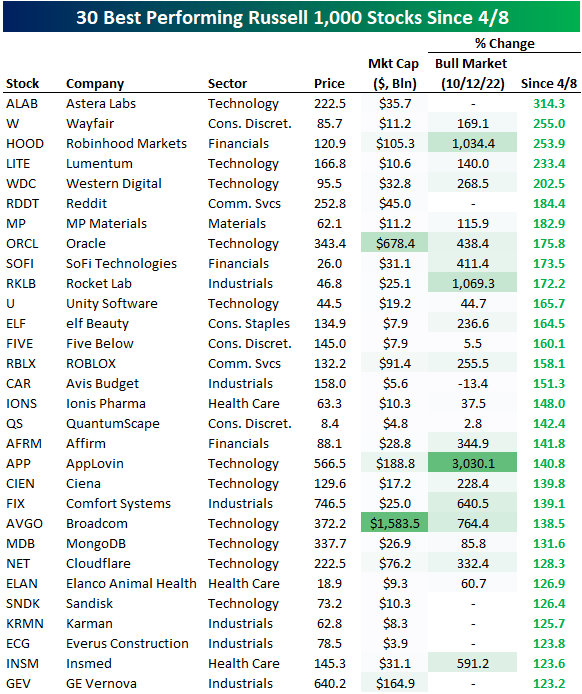

The average Russell 1,000 stock is now up 29% since the index’s low on April 8th following the Tariff-Crash of early April. There are 47 stocks in the index that have more than doubled since then, and below are the 30 that are up the most. Five stocks are up more than 200%: Astera Labs (ALAB), Wayfair (W), Robinhood (HOOD), Lumentum (LITE), and Western Digital (WDC). As shown below, Oracle (ORCL) is up the 8th most of any stock in the Russell 1,000 since 4/8 with a gain of 175.8%.

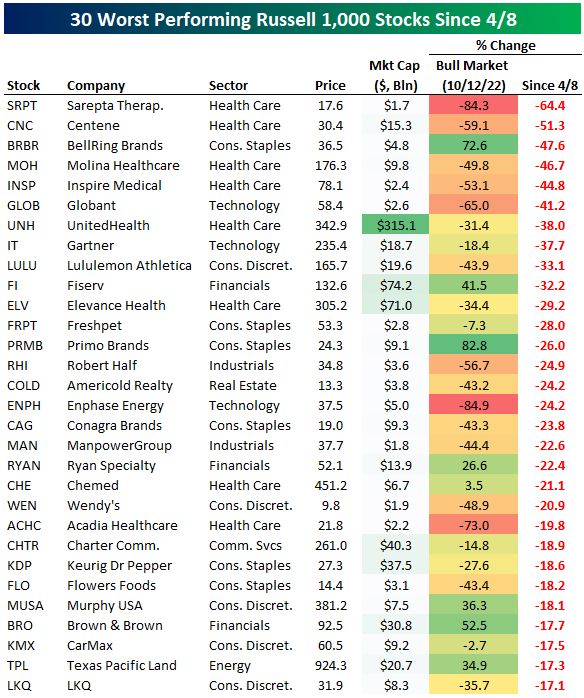

There are 155 stocks in the Russell 1,000 that are down since 4/8 (roughly 15% of the index). Below are the 30 worst performers over this time frame. The three worst performers have been Sarepta Therapeutics (SRPT), Centene (CNC), and BellRing Brands (BRBR).

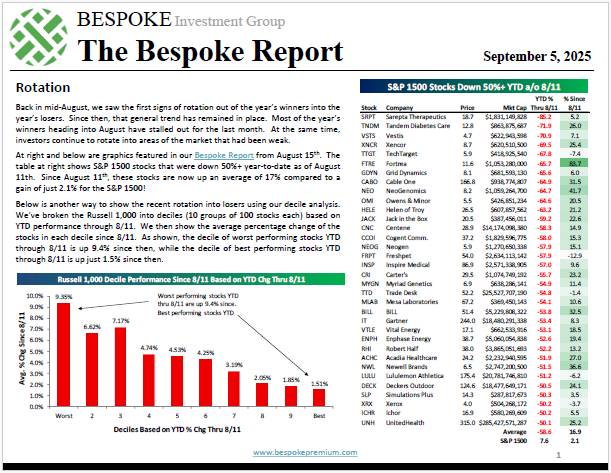

Sep 5, 2025

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium.

The tape has been heavy for growth stocks for a few weeks now, especially AI names, but that hasn’t stopped investors from rotating into other areas of the market that had been doing poorly up until mid-August. Read our thoughts on recent market action and where we might go from here in this week’s report.

Sep 2, 2025

If you missed Bespoke’s Paul Hickey on CNBC this morning, click here to watch the clip.

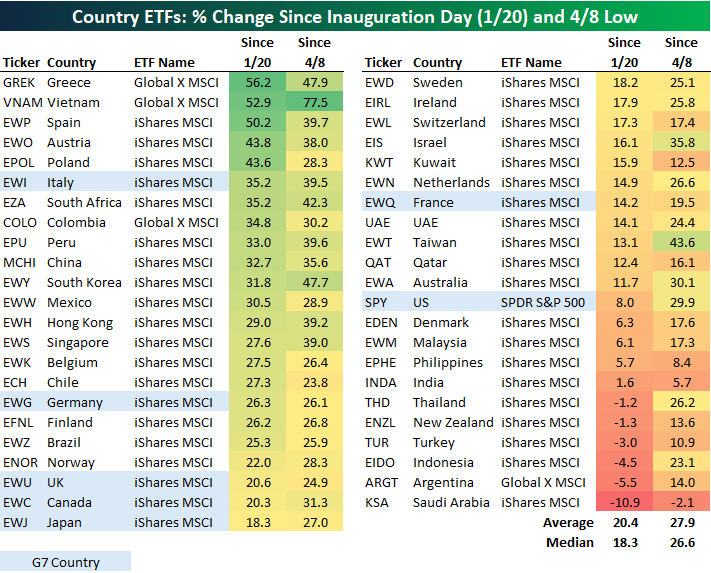

It has been 225 days since President Trump’s Inauguration on January 20th, and the S&P 500 (SPY) entered today up 8% since the last close before the Inauguration. That ranks 35th out of 45 country stock market ETFs we track closely. With a gain of 20.4%, the average country ETF shown in the table below is up much more than the US (SPY) since Trump 2.0 began. Greece (GREK), Vietnam (VNAM), and Spain (EWP) are up the most at 50%+, while Italy (EWI) has been the best performing G7 country at +35.2%. Speaking of the G7, the US has been the worst market among these seven developed nations since Inauguration Day in January.

In addition to post-Inauguration Day performance, we also show how each country ETF performed since global equity markets made their post-tariff crash lows on April 8th. The US (SPY) has posted much more respectable returns relative to the rest of the world; up 29.9% versus the average of 27.9%. Of the G7, only Italy (EWI) and Canada (EWC) are up more than the US (SPY) since April 8th, while France (EWQ) has lagged the most of this group with a gain of 19.5%.

Along with being the second-best-performing country ETF since Inauguration Day, Vietnam (VNAM) has easily been the best performer since April 8th with a gain of 77.5%. On the flip side, Saudi Arabia (KSA) is the only country ETF that is down over both periods (-10.9% since 1/20, -2.1% since 4/8). Argentina (ARGT) and Indonesia (EIDO) are two others that are now solidly red since 1/20, while India (INDA) is up just 1.6% since 1/20 and 5.7% since 4/8 (second worst).

Aug 29, 2025

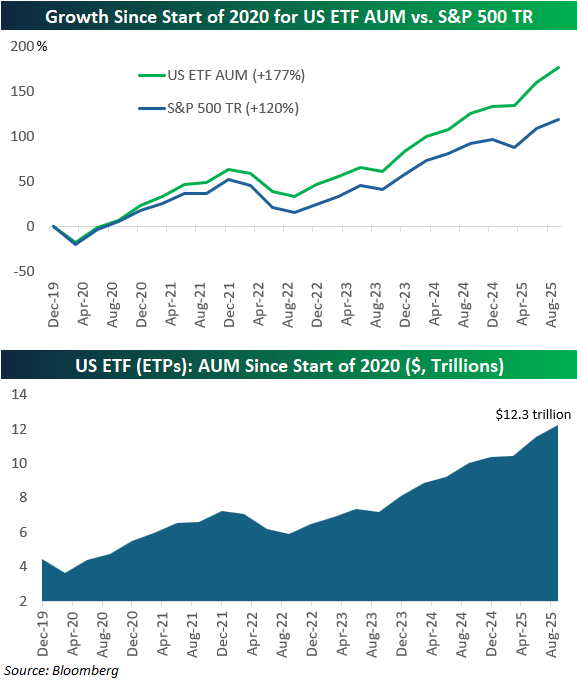

With the recent news that there are now more ETFs than stocks in the US, we wanted to provide an update on the dollar amounts that have flowed into ETFs so far this decade.

Since the end of 2019, exchange-traded products (ETPs) in the U.S. — primarily ETFs — have exploded in size, outpacing even the impressive rise of the S&P 500.

The first chart below highlights just how powerful the trend has been: while the S&P 500’s total return has surged about +120% since the start of 2020, US ETF assets under management (AUM) have climbed an even steeper +177%. That gap shows that ETFs have not just grown alongside the market; they’ve attracted a massive wave of fresh capital from investors seeking low-cost, diversified, and flexible investment vehicles.

The second chart below underscores this growth in dollar terms. According to Bloomberg, U.S. ETF assets have ballooned from around $4 trillion at the start of 2020 to a record $12.3 trillion today. While markets have had their ups and downs over the past five years, the long-term trajectory of ETF adoption has been relentlessly upward. This expansion is being fueled not only by equity gains but also by the sheer volume of new inflows, as investors of all sizes, retail to institutional, continue to shift from mutual funds and other structures into ETFs. Put simply, ETFs are no longer a niche product…they are the market. With their assets now equal to more than half of U.S. GDP, their influence on trading flows, liquidity, and even market structure will only grow. And with ETF growth running far ahead of the broader equity market, this wave of adoption shows no sign of slowing down.