The Bespoke Report – Equity Market Pros and Cons – Q4 2025

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q4 2025.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, sign up for Bespoke’s 50/20 special today. Our 50/20 special gets you a full year of Premium for half off, then 20% off per month after the first year. SIGN UP HERE.

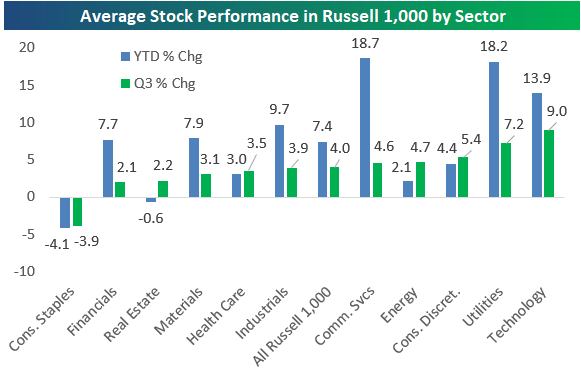

Key ETF Performance in September, Q3, and YTD

Below is a check-up on asset class performance using our key ETF matrix. For each ETF, we show its September, Q3, and YTD total return.

US index ETFs posted solid gains in both September and for all of Q3, with the Nasdaq 100 (QQQ) leading the way in September but the small-cap Russell 2,000 (IWM) leading for the full quarter. Small-cap value (IJS) did well in Q3 in particular.

Notably, the S&P 500 Equalweight (RSP) was up much less than the cap-weighted S&P (SPY) in September, as the mega-caps once again drove upside performance.

Looking outside the US, Argentina (ARGT) was the only real area of pain in September, although Germany (EWG) and Australia (EWA) were both down slightly as well. China (MCHI) and Mexico (EWW) were the two best country ETFs in September with gains of 7%+, while China (MCHI) led the way for all of Q3 with a gain of 19.5%. On the year, Spain (EWP) is still up the most at 61.2%.

Gold (GLD) and silver (SLV) were on fire in September with gains of 11.8% and 17.1%, respectively. Treasury ETFs were up slightly across the board during the month as rates fell, with longer duration up the most.

Biggest Winners to Close Out Q3

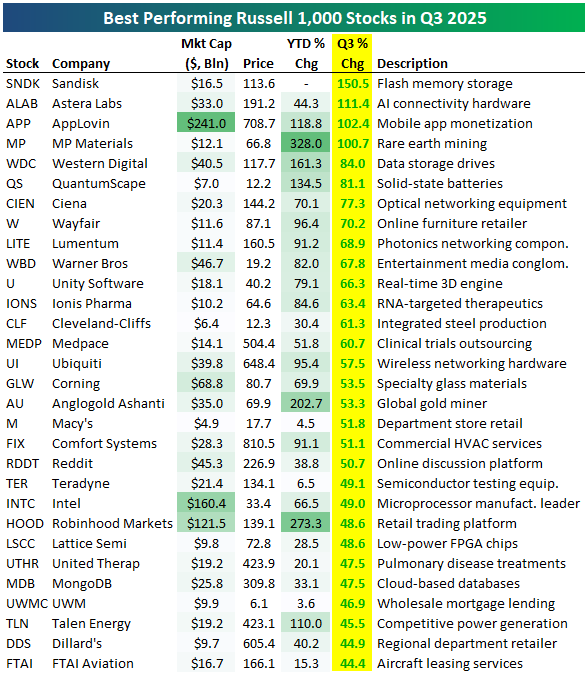

The large-cap Russell 1,000 is set to close out Q3 with a gain of roughly 7%, but the average stock in the index is up much less than that at 4%. The performance divergence is due to outperformance from mega-caps that push the cap-weighted index ever higher.

The five sectors whose stocks averaged bigger Q3 gains than the broad index (4%) are Technology (9%), Utilities (7.2%), Consumer Discretionary (5.4%), Energy (4.7%), and Communication Services (4.6%). Just one sector saw its stocks average declines in Q3: Consumer Staples (-3.9%).

Year-to-date, two sectors stand out: Communication Services and Utilities. Stocks in each of these sectors are up an average of 18%+ year-to-date through three quarters. Tech ranks 3rd at 13.9%, followed by Industrials at 9.7%.

Two sectors have seen their stocks fall year-to-date on average: Consumer Staples (-4.1%) and Real Estate (-0.6%).

Below are the 30 best performing stocks in the Russell 1,000 in Q3. There are four companies that gained more than 100% during the quarter: Sandisk (SNDK), Astera Labs (ALAB), AppLovin (APP), and MP Materials (MP). Another four gained more than 70%: Western Digital (WDC), QuantumScape (QS), Ciena (CIEN), and Wayfair (W). While there are a few names on the list of Q3’s big winners that aren’t related to AI, the AI Boom certainly made its presence felt.

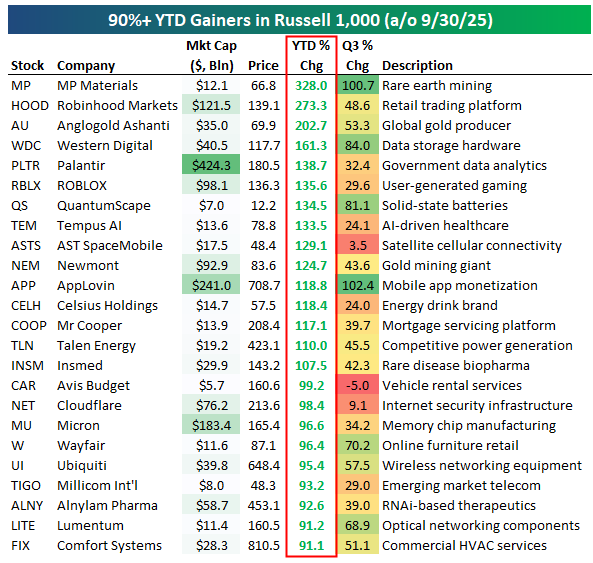

There are 24 stocks in the Russell 1,000 up 90%+ year-to-date as we close out Q3, including 15 that are up 100%+. MP Materials (MP), which gained 100% in Q3, is at the top of the leaderboard with a YTD gain of 328%. Two more stocks are up 200%+ on the year: Robinhood (HOOD) and Anglogold (AU). Western Digital (WDC) and Palantir (PLTR) round out the top five with YTD gains of 161% and 139%, respectively.

Other 100%+ winners through three quarters include social-gaming app ROBLOX (RBLX), AI healthcare platform Tempus AI (TEM), satellite cell-service provider AST SpaceMobile (ASTS), and energy-drink maker Celsius (CELH).

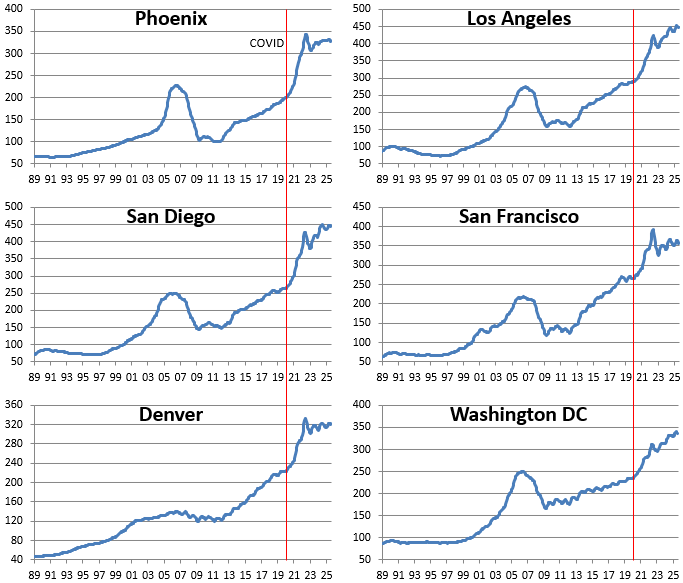

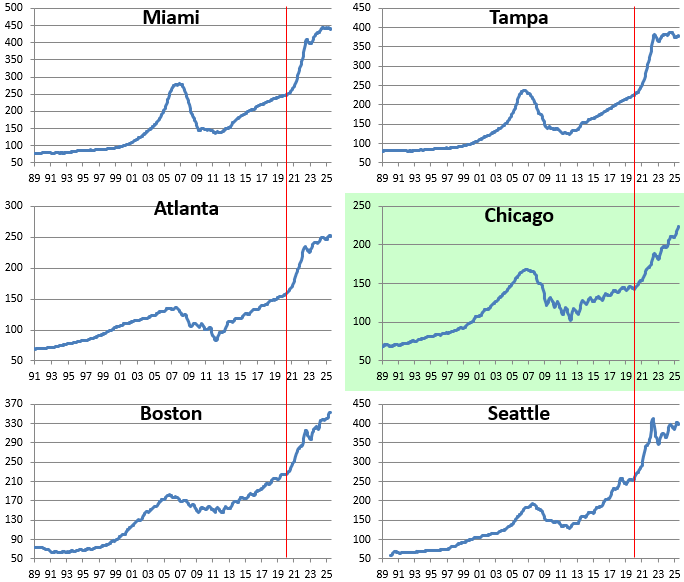

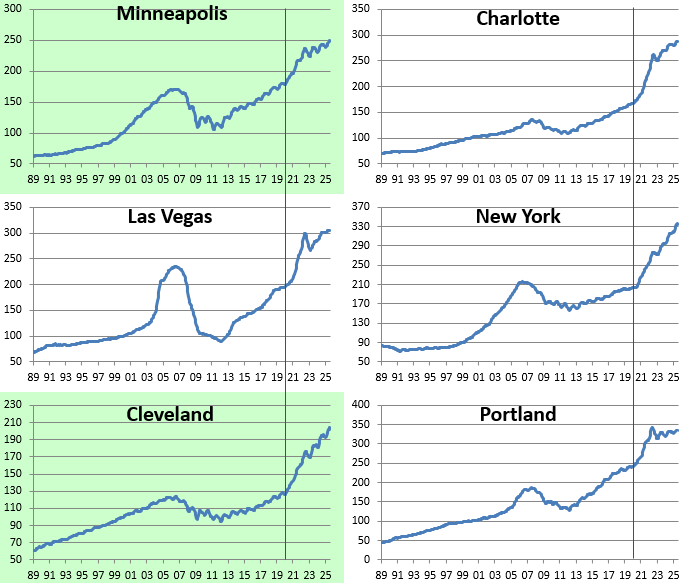

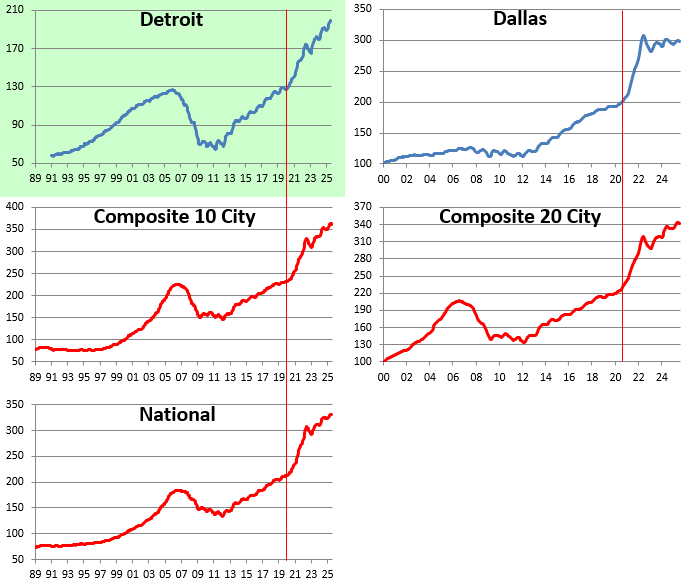

Midwest Resilience vs. Coastal Fatigue

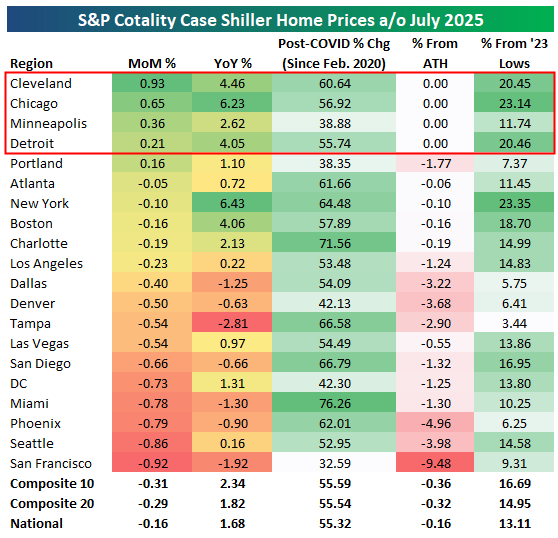

The latest S&P Case-Shiller home price data paints a clear regional divide in the U.S. housing market. Midwest cities were up on the month and remain at all-time highs (Cleveland, Chicago, Minneapolis, Detroit), while cities in the South and West continue to struggle.

Strength in the Midwest appears to be driven by relatively lower absolute price levels, tight supply, and steady migration in from more expensive regions.

In the South and West, many metros that were pandemic-era darlings are now rolling over. Places like San Francisco, Phoenix, Seattle, Las Vegas, Tampa, and Miami all saw monthly declines and remain below all-time highs. San Francisco was down the most of any metro on the month with a drop of 0.92%, while Tampa is down the most year-over-year at -2.8%.

Along with the Midwest, major metros in the Northeast like Boston and New York that are also supply constrained remain up solidly year-over-year and were only down slightly on the month.

Based on the latest Case Shiller data, the dynamic has flipped: instead of “Sun Belt boom, Rust Belt lag,” the post-COVID housing cycle now features a Midwest resilience vs. coastal fatigue narrative.

Below are price charts for each of the metros tracked. The four Midwest cities that hit all-time highs in the latest month are highlighted in green.