See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“All you have to do is say something nobody understands and they’ll do practically anything you want them to.” – J.D. Salinger

Bespoke’s Paul Hickey will be appearing on Making Money With Charles Payne today at 2 PM on Fox Business. Check it out!

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss markets and inflation. To view the segment, click on the image below.

Futures were modestly weaker early this morning, but things have taken a turn for the worse as the morning goes on. S&P 500 futures are currently down 0.3% while the Nasdaq is indicated to open nearly 1% lower as investors question the durability of the AI trade. Treasury yields are moving higher, with the 10-year yield up 4 basis points to 4.59%, and crude oil is fractionally higher, trading right around $80 per barrel as President Trump threatens to escalate attacks on Iran. Gold and Bitcoin are both lower by about 1%.

It was a tough night in Asia as the Nikkei plunged nearly 3% and South Korea tanked over 6%. The weakness in South Korea comes as regulators look to crack down on levered ETFs, which have been driving much of the volatility on both the way up and the way down.

European stocks are also lower again this morning, with the STOXX 600 down 0.5% while Germany trades down by nearly a full percent. UK GDP came in modestly better than expected, while Industrial Production and Construction Output both dropped more than expected.

It’s a busy day for data in the US this morning, and just about all of it was better than expected. Initial and continuing jobless claims both came in slightly lower than expected, while Retail Sales were mostly in line with expectations, although May’s numbers were revised slightly higher. The real showstopper of the morning, though, was the Philly Fed report, which came in much better than expected as the headline index surged to 41.4 (highest since November 2021) versus forecasts for a reading of 12.5,

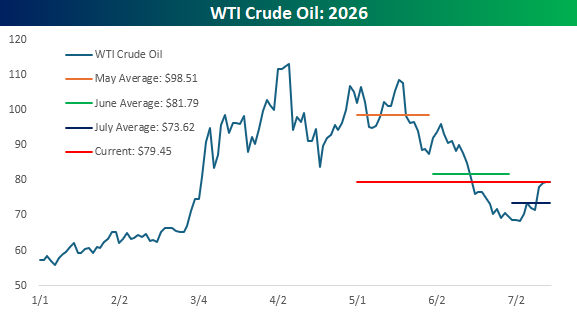

No matter how good the news gets, you can always count on skeptics to show up with a barrage of “buts”. This week’s inflation data from the June CPI and PPI reports both came in lower than expected, easing concerns over the troubling inflation levels from May’s numbers. Before investors could even digest the reports, though, you didn’t have to look far for the rebuttals. Yes, these numbers were good, they said, but with the war in Iran reigniting in the last couple of weeks, oil prices have rallied more than 15% from the early July low, so next month’s numbers will erase the improvement we saw in June.

Inflation is about more than just the price of oil, but since that was the focus of the loudest of the “buts,” let’s look at the trend in prices. During May, crude oil prices averaged $98.51 per barrel. In June, which is the month this week’s data was based on, prices averaged $81.79 per barrel. This morning, after oil prices have “surged” off the July lows, WTI is trading at $79.45 per barrel. That’s still nearly 3% lower than the average price from June, and the average price of $73.62 this month is 10% less than the average price in June. If oil were the only determinant of CPI, we’d be set up for another negative print!

The point here isn’t to diminish the fact that elevated inflation is a long-term issue. We’ll be the last ones to get complacent about the market and inflation, but at current levels, oil prices don’t appear to be a threat to unwind the improvement in CPI that we saw in this week’s data. If the oil price rises back up towards $90 per barrel? Yes, that would be a problem.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.