See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Philosophy is common sense with big words.” – James Madison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a shaky start to the third quarter yesterday, equity futures remained wary ahead of the June Non-Farm Payrolls report, with the S&P 500 basically unchanged while the Nasdaq was up less than 10 basis points. Treasury yields are slightly higher, but the 10-year yield is back above 4.5%. The real story, though, is in the energy market, where WTI prices are down over 2% and back to where they traded before the war with Iran started. Gold prices are down fractionally, and Bitcoin is higher, trading back above $61K.

In Asia, it was a shaky night led lower by tech stocks as South Korea plunged nearly 8%, the Nikkei fell 2.5%, and China dropped 2%. That’s not the start of a quarter bulls would have hoped for, but it’s also not unexpected given the moves higher we saw in Q2.

In Europe, stocks are broadly higher with the STOXX 600 trading up over 0.5%, as Italy and Spain lead the way, gaining over 1%.

It’s a busy day for economic data as we pack a lot of reports into the day due to Friday’s holiday. The main report, though, was the Non-Farm Payrolls report, which came in weaker than expected. The initial read was 57K, or about half expectations. Despite the weaker print, the Unemployment Rate dropped to 4.2% versus forecasts for 4.3%. Also, Initial and Continuing Claims were both slightly lower than expected. So, the headline number may have been weaker than expected; other releases weren’t nearly as bad. When it comes to the Non-Farm Payrolls, the most important thing to remember is that the initial release is what you tell your wife you’re going to spend at Costco, and the revision is your credit card statement. They’re rarely the same!

As we kick off the second half, investors face no shortage of questions. Will earnings season live up to expectations? Will inflation cool? Will the ceasefire in the Middle East continue? Will the AI trade continue to keep the market afloat, or will the underperformance of mega-caps sink the rally? We can all take our best guesses at these questions, but only time will tell, and as events unfold, the market will continue to react with gains and losses.

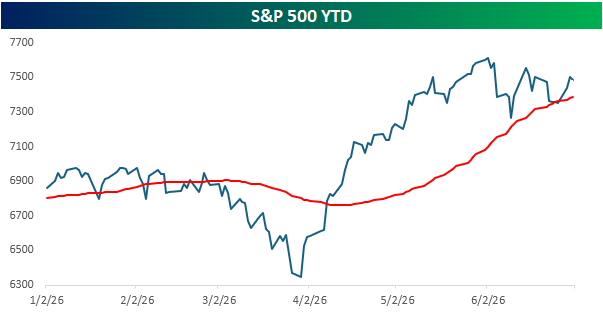

After a blistering rally off the March lows, investors are starting to question their recent optimism, which has caused the advance to stall. Heading into the last trading session before the July 4th holiday, the S&P 500 sits just above its 50-day moving average, so even on a short-term basis, the rally remains in place despite the sawtooth action of the last six weeks.

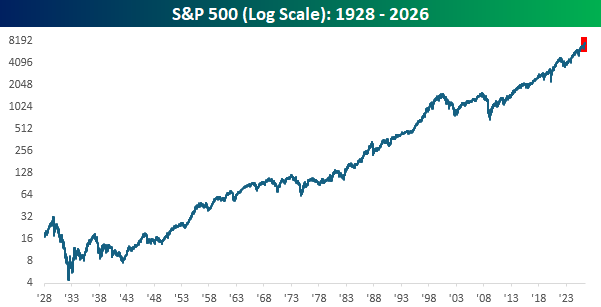

Regardless of how the market responds to these short-term questions, the most important thing to keep in mind is that over the last 250 years (to the day Saturday!), there has been no better investment than the US economy. The chart below goes back nearly a century, and the trend has been clear. It hasn’t been a straight line higher, but the last six months (red box) look inconsequential, and even the dark days of the Great Depression and the unwinding of the 1990s tech bubble don’t seem that bad. Most importantly, though, we got through them.

In real time, the road ahead won’t be smooth, but time has a way of smoothing out the rough edges, and $1 invested in the S&P 500 in 1928 would be worth more than $10,000 today. So, let’s all celebrate this weekend what makes this country the greatest place on earth and get back to work next week in the pursuit of making that $10,000 worth $100,000,000 by 2126! Happy 250th, everyone!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.