See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures have been losing steam as we approach the opening bell, with the biggest recent winners leading the losses. S&P 500 futures are indicated to open nearly 0.5% lower, while the Nasdaq is poised to gap down 0.75%. Treasuries aren’t doing much this morning as the 10-year yield is modestly lower but still above 4.6%. Crude oil is little changed but elevated as the Middle East is on edge over whether the US will launch a new round of attacks on Iran. Gold and Bitcoin are both fractionally lower.

In Asia, it was a mixed session with the Nikkei down 0.5% following a modestly stronger than expected GDP report, while China was up nearly 1%. With AI-related stocks coming under pressure yesterday, South Korea fell 3.3%.

With tech and AI-related stocks leading the selling pressure, European stocks are much more immune, and the STOXX 600 is bucking the trend of weakness with a gain of 0.8%. Germany is leading the way higher with a gain of 1.4%, while Italy lags with just a marginal gain.

In the US today, it’s a quiet day for data with Pending Home Sales at 10 AM. On a housing-related note, though, shares of Home Depot (HD) are trading marginally lower after reporting earnings this morning. Management noted that while the consumer continues to “defer their spending on larger projects…consistent with what they’ve told us the last few years,” they remain engaged.

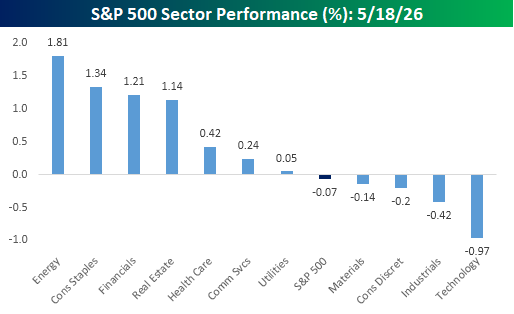

Divergent market breadth usually gets the most attention when the S&P 500 trades higher, but the net number of stocks trading higher on the day is negative. Yesterday was the opposite, where the S&P 500 traded lower, but most stocks in the index finished the day higher. At the sector level, yesterday was also net positive as seven sectors traded higher while just four traded lower. With Technology being one of those sectors that traded lower, though, it dragged the entire market into the red with it.

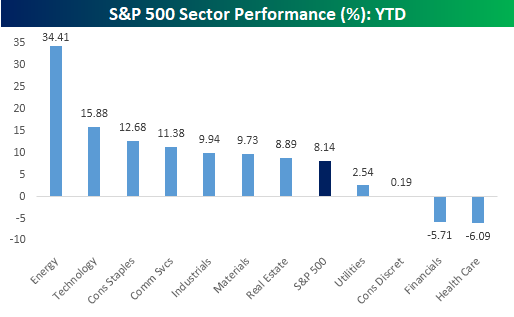

For all the talk recently about how narrow breadth has been, the YTD picture of sector performance is also surprisingly positive. While the S&P 500 is 8.1% higher YTD, seven sectors have outperformed the index on a YTD basis, while just four have declined.

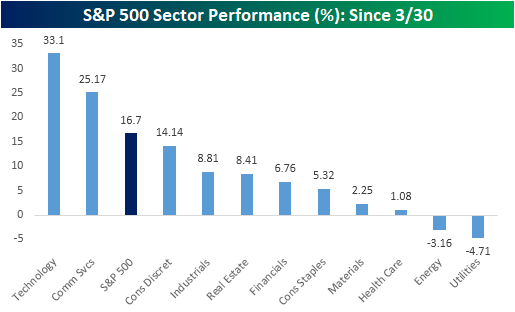

Where the big breadth divergence has occurred is since the low on 3/30. In the seven weeks since then, the S&P 500 is up 16.7%, but just two sectors – Technology and Communication Services – have outperformed. What really stands out is how many sectors have outperformed the S&P 500 by A LOT since 3/30. As shown in the chart, besides Technology and Communication Services, the only other sector that is even close to performing in line with the index is Consumer Discretionary.

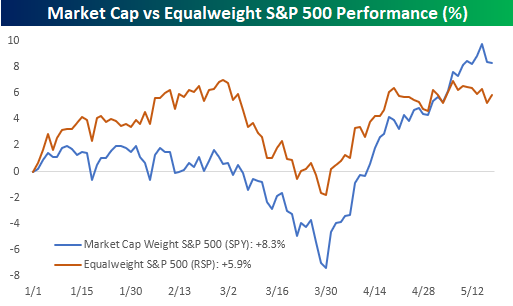

Comparing the performance of the market cap and equalweight S&P 500 so far this year, while the market cap-weighted S&P 500 has outperformed, it’s not as though the divergence has been all that wide. While there have been times throughout the year when one version has significantly outperformed the other, in the bigger picture, they have largely cancelled each other out.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.