See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you don’t use your experience, your past is wasted” – Alan Shepard

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Yields are behaving themselves this morning as the 10-year US Treasury yield is unchanged at around 4.44%, and near the highest levels since last summer.

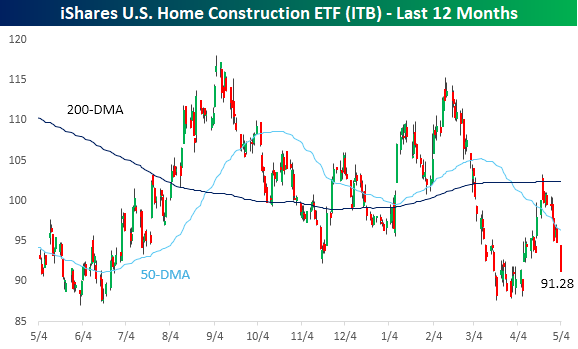

While rising yields haven’t had much of an impact on the overall equity market yet, the same can’t be said for homebuilders. In early February, the iShares US Home Construction ETF (ITB) was near 52-week highs and above $115. Yesterday, it closed at $91.28, or more than 20% below those levels from two months ago. While the S&P 500 is up over 13% from its March lows, ITB has only rallied 3%.

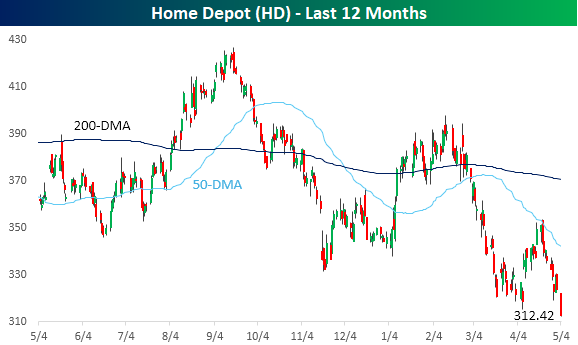

Rising yields have been more painful for housing-related stocks. Home Depot (HD) is a perfect example. Yesterday, the world’s largest home improvement retailer closed at a 52-week low of $312.42. The stock is down over 20% from its February high and over 26% from its 52-week high.

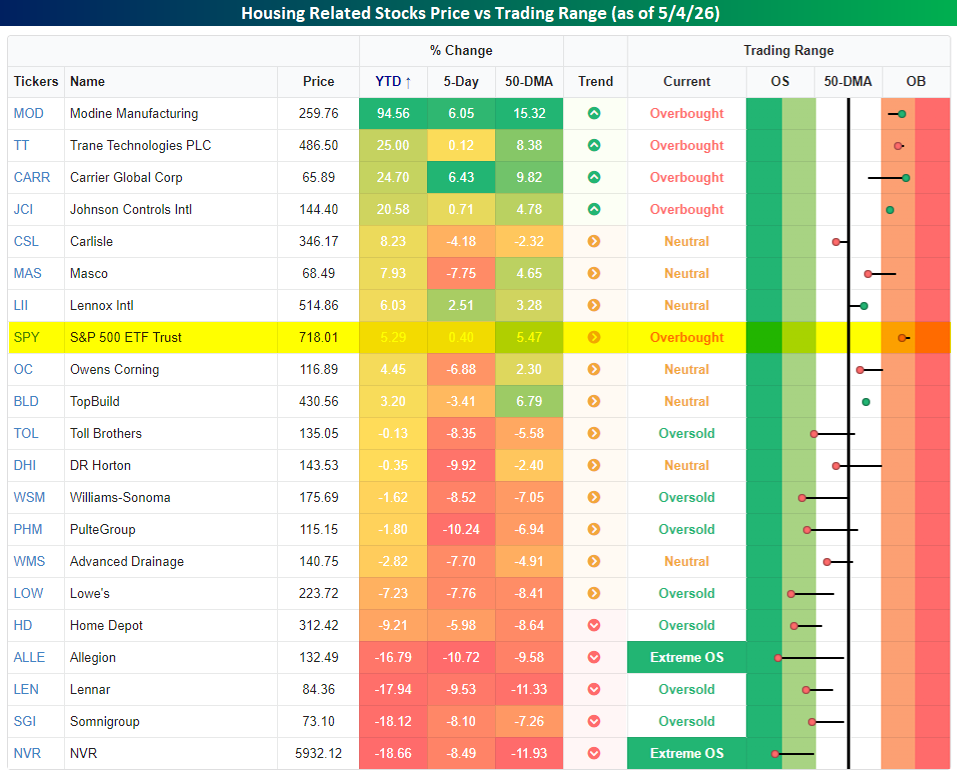

Looking more broadly at housing-related stocks. The snapshot below from our Trend Analyzer shows the 20 largest components in the SPDR S&P Homebuilders ETF (XHB), and the majority are not only underperforming the S&P 500 on a YTD basis, but they’re also down. The last week has been especially painful for the group, as all but six of them are down just as yields have started to spike.

There are some bright spots in terms of performance this year. Stocks like Modine Manufacturing (MOD), Trane Technologies (TT), Carrier Global (CARR), and Johnson Controls (JCI) are all up over 20% YTD, and they’re the only overbought stocks on the list. The rally in these four stocks really has nothing to do with housing, though. They’re all rallying due to the massive demand for cooling in AI data centers.

Turning to the markets this morning, futures are higher with the S&P 500 indicated to open up 0.4% and the Nasdaq rallies 0.6%. As mentioned above, yields have been behaved with the 10-year right around yesterday’s close of 4.44%. Oil prices are giving back some of yesterday’s gains, falling over 2% to just under $104 per barrel in WTI. Lastly, gold prices are up about 1%, while Bitcoin is up over 1% and back above $81K.

In Asia overnight, Japan, China, and South Korea were closed, while Hong Kong dropped 0.8%. In Europe, markets are all open and generally higher. The STOXX 600 is up 0.5%, led higher by Spain (1.35%) and Germany (1.0%). The UK is the main laggard, falling 1.3%.

In the US today, we’ll get service sector PMIs from S&P and ISM, along with New Home Sales and JOLTS.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.