See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Better three hours too soon than a minute too late” – William Shakespeare, The Merry Wives of Windsor

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss energy, midterms, and the markets. To view the segment, click on the image below

Equity futures traded sharply lower overnight on concerns of renewed military action in the Middle East. Since then, the negative sentiment has receded on reports out of China that the US and Iran will return to the bargaining table, and futures are well off their lows. S&P 500 and Nasdaq futures are now flat, while the Dow, being dragged lower by a decline in IBM, is indicated to open down 0.35%.

Treasury yields are marginally higher this morning, with the 10-year yield ticking above 4.30%, while crude oil is now lower after trading much higher overnight. Gold prices are fractionally lower, and Bitcoin is still down 1.5% at just under $78K.

Asian stocks were mostly lower overnight, with South Korea the standout gainer among a sea of red. Higher oil prices were the primary driver of the weakness. In terms of economic data, though, flash PMI readings for April in Japan, India, and Australia came in higher than expected. European stocks are also trading tentatively this morning as the STOXX 600 trades down 0.3%, with France the only gainer. Like Asia, the flash PMI reading for the Eurozone Manufacturing also unexpectedly showed an acceleration.

Besides the pickup in earnings flow, the economic calendar is busy this morning with jobless claims at 8:30, flash PMI readings at 9:45, and then the KC Manufacturing report at 11 AM. On the sentiment front, if should come as no surprise that AAII’s weekly survey saw a big uptick in bullish sentiment, rising from 31.7% up to 46.0%, which isn’t far from the 52-week high of 49.5% in January.

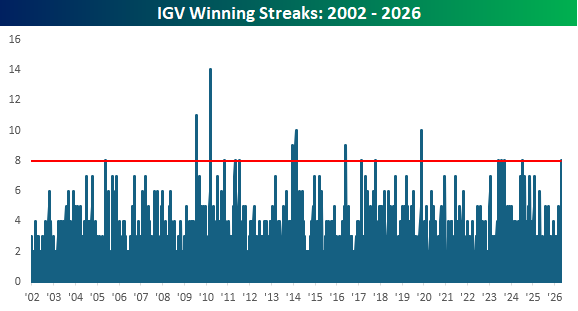

Semis and software have generally moved in opposite directions this year, but over the last several days, both have moved higher. Semis extended their streak of daily gains to a record 15 trading days yesterday, and the streak in software stocks has been half as long. As shown in the chart below, the iShares Expanded Tech Software Sector ETF (IGV) has traded higher for eight straight days, making it tied for the longest daily winning streak since late 2019. With the ETF trading down close to 3% this morning, though, we wouldn’t bet on the streak extending to a ninth day.

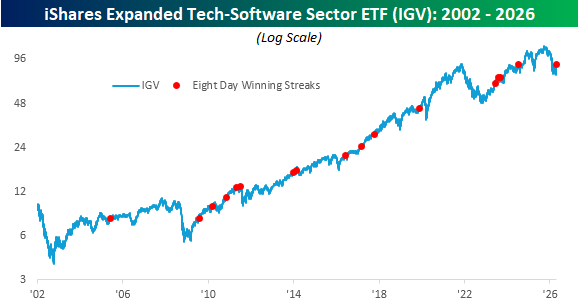

The chart below shows a long-term look at IGV’s performance, with red dots showing every prior eight-day streak. Only once, in the summer of 2011, did one of these streaks coincide with a notable peak in the sector, as the majority occurred within various stages of longer-term uptrends. This current streak has been somewhat unique in that IGV is trading so close to a low.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.