See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you’re in a good situation, don’t worry it’ll change.” – John A. Simone Sr.

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a big rally on Friday on homes that the Iran war was ending, futures are lower to start the week as uncertainty over the progress of the war rekindles itself. The damage isn’t nearly as bad as it was earlier, though, as both S&P 500 and Nasdaq futures are down less than 0.5%. Treasury yields are only slightly higher, and while crude is trading up close to 6%, WTI is still below $89 per barrel. Gold prices are down 1%, and Bitcoin is surprisingly higher as it holds above $75K. In the short term at least, the market has taken a two steps forward, one step back mentality.

Despite the weakness in US futures, Asia had a positive session as it played catch-up to Friday’s rally. The Nikkei rallied 0.6% while South Korea added 0.4%. Europe, however, was still open on Friday when the positive news regarding the Strait came out, so this morning, the STOXX 600 is down over 1.1% with Italy and Germany leading the way lower (-1.4%).

The economic calendar is light in the US today, and there isn’t even a lot in the way of earnings reports for investors to digest, but that will change as the week goes on as we head into the peak of earnings season.

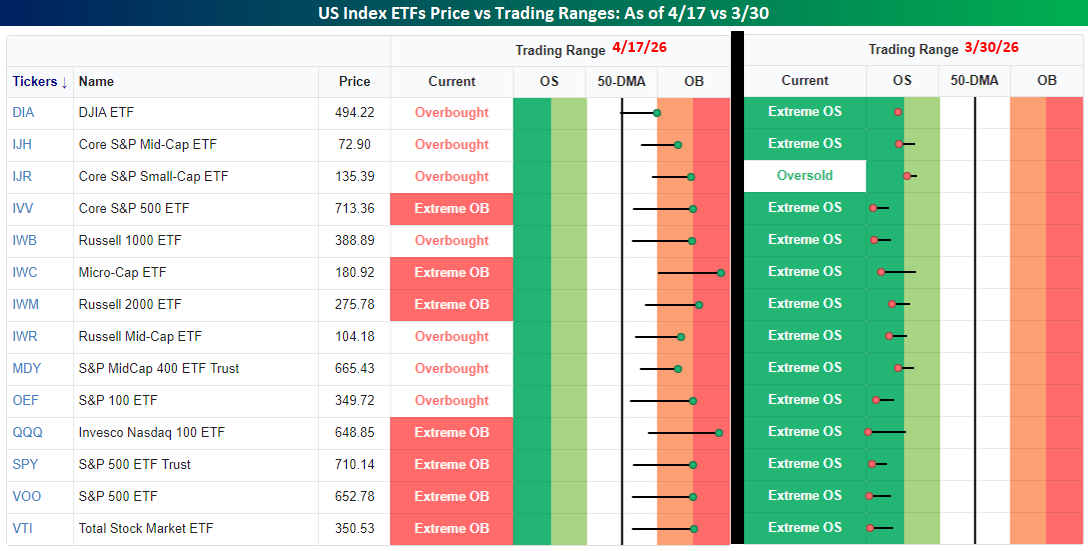

Equities are on pace to start the week lower, but keep in mind how fast it’s recovered. The snapshot below shows where US index ETFs closed out last week relative to their trading ranges compared to where they were as of the close three weeks ago today. As of Friday, every US index ETF in our screen finished off last week at either overbought (1+ standard deviations above the 50-DMA) or extreme overbought (2+ standard deviations above) levels. Three weeks ago, all but one of them were at extreme overbought levels. We’ve come a long way, so some short-term digestion of the moves is only natural.

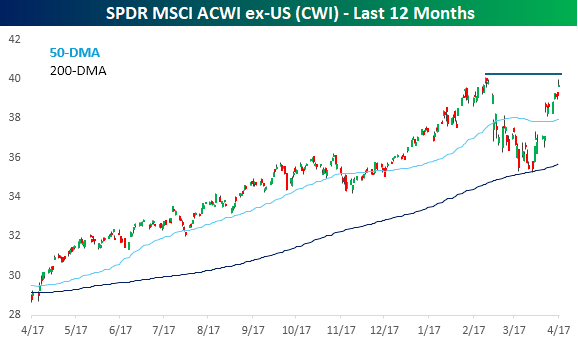

While major US indices closed out the week at record highs last Friday, the same can’t be said for stocks on an international basis. The chart below shows the performance of the SPDR MSCI ACWI Ex US ETF (CWI) over the last year. The sell-off because of the Iran war took the ETF right down to a successful retest of its 200-day moving average, and like the US, the rebound was faster than the decline. Unlike US equities, though, CWI’s rally on Friday stalled out just shy of the all-time highs from late February.

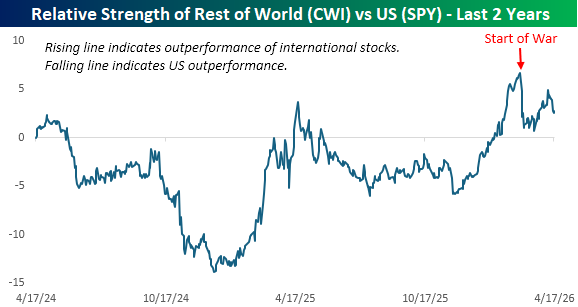

It’s well known by now that the US economy is much more insulated from the issues in the Middle East than the rest of the world, and the chart below illustrates that. On a relative strength basis, international equities bottomed shortly after the 2024 election and reached a short-term peak around Liberation Day last April. Towards the end of last year, as tariff concerns fell off the front page, international stocks started rallying again, hitting a multi-year high right at the end of February.

The start of the war abruptly derailed that outperformance, and while international stocks rebounded in late March into early April, they started to rollover again last week, and look poised ot continue that underperformance today. That weakness was somewhat surprising given it came as tensions in the Persian Gulf started to ease, but if there’s one thing we can all be certain of, the market is always full of surprises.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.