See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I try not to worry about things I can’t do anything about.” – Christopher Walken

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Sometimes the headlines make you scratch your head. This morning, equity futures are sharply higher with the rally attributed to a Wall Street Journal report that “Trump Tells Aides He’s Willing to End War Without Reopening Hormuz”. As we highlight below, stocks have been following the lead of oil prices at an unprecedented rate over the last several weeks, and if the US just walked away from the Middle East with the Strait still blockaded, energy markets would likely remain incredibly supply-constrained, keeping prices high. The longer prices are high and supplies are limited, the worse it’s going to be for the global economy and ultimately stock prices.

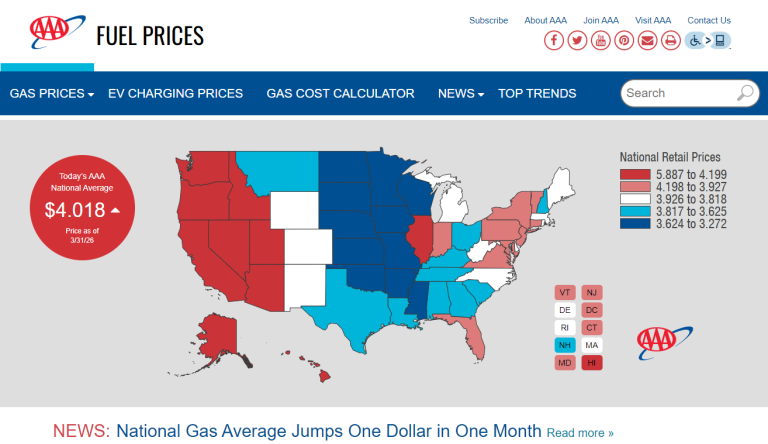

Just today, the national average price of a gallon of gas is above $4 for the first time since 2022, and as shown in the image below, it has increased by more than a dollar in just the last month.

Regardless of the reason, equity futures are up about 1% this morning, treasury yields are lower, and crude oil is slightly higher. Again, higher oil prices in this environment are negative for equity prices, and the gains we are seeing in futures may be nothing more than rebalancing ahead of quarter-end. Gold prices are up over 1%, and Bitcoin has seen a fractional gain.

We’re still in the ‘shoulder season’ for earnings, but it’s a busy day for economic data. At 9:45, we’ll get the Chicago PMI for March, followed by Consumer Confidence and JOLTS at 10 AM. The Chicago PMI and Consumer Confidence reports are both for March, so they will give some of the first reads on how the war has impacted economic and consumer sentiment.

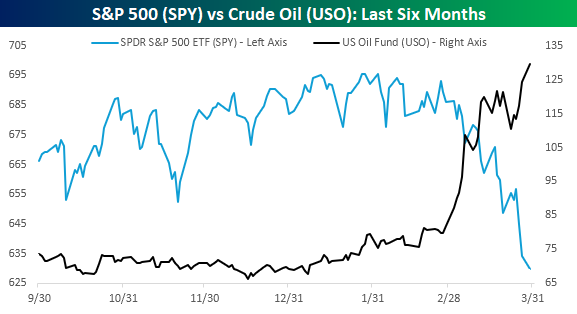

If you want to know the direction of the equity market these days, look at crude oil and go with the opposite. It’s become cliché, but it also hasn’t been truer at any point in at least the last 20 years. Just look at the performance of the SPDR S&P 500 ETF (SPY) compared to the US Oil Fund (USO) over the last six months. The two series have mirrored each other.

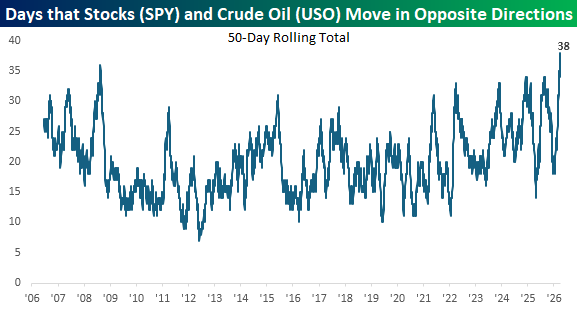

USO launched in 2006, and we compared the daily direction of the ETF and SPY for every trading day since its inception. The chart below shows the rolling 50-day total of the number of days that the two ETFs moved in opposite directions on the day. In the most recent 50-trading-day period, when USO zigged, SPY zagged 38 times, or 76% of all trading days. In the ETF’s history, its daily moves have never been more inversely correlated to the direction of SPY. The only other time the number of occurrences even approached current levels was back in August 2008. Ironically, that was also part of the price spike when crude oil first crossed $100, ultimately peaking above $147.

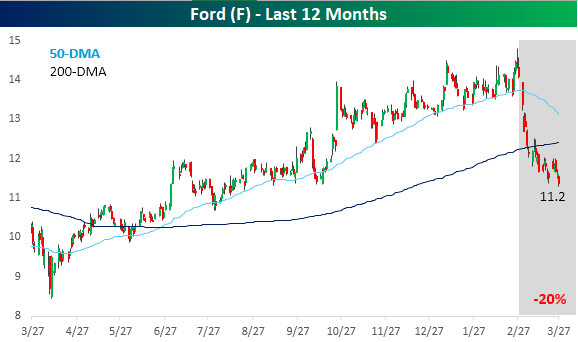

One sector that has felt the pain of higher oil prices is the traditional auto OEMS. Just moving alphabetically down the list, shares of Ford (F) had performed exceptionally well leading up to the war, with shares in a steady uptrend and trading at 52-week highs on the eve of the first missiles being fired. Since then, it’s down 20%.

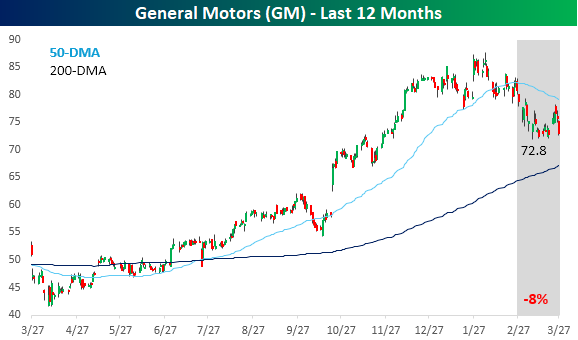

General Motors (GM) performance leading to the war was also very strong, and even though it wasn’t’ right at 52-week highs, shares were up more than 70% in the prior year. Shares have declined more than 17% from their peak and are down 8% since the war started.

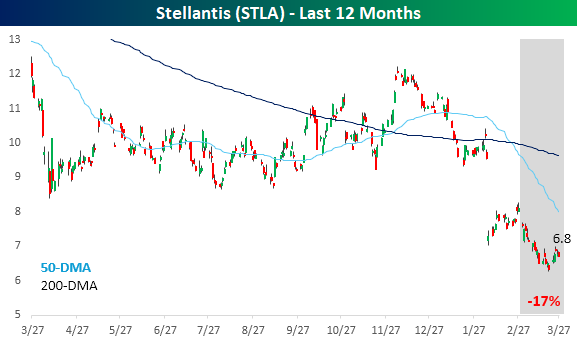

Unlike F and GM, Stellantis (STLA) was already weak leading up to the war and down sharply from its 52-week highs. Since then, it’s only got worse as shares are down 17% this month.

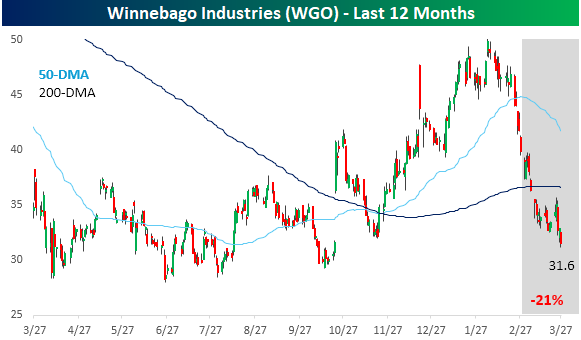

When you think of car stocks, Winnebago (WGO) may not be the first stock that comes to mind, but boy, is it ever exposed to higher gas prices. Right before the war, the stock was right at 52-week highs, perhaps on optimism that many Americans would take road trips to celebrate America turning 250. A month later, with gas prices at $4 per gallon nationwide, and suddenly that 10-mile-per-gallon gas guzzler doesn’t seem nearly as good an idea.

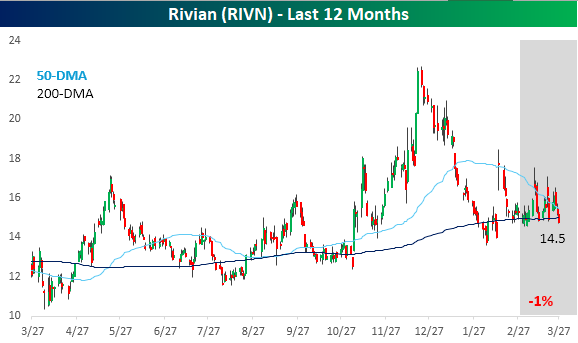

While traditional car companies with a focus on internal combustion engines have had a rough March, what about EV companies? Well, RIVN hasn’t rallied this month, but in this market, a decline of 1% is basically a win.

Until gas prices at the very least stop going up as quickly as they have, it’s going to be hard for these traditional auto stocks to get out of their own way.