See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Philosophy is common sense with big words.” – James Madison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been a tough few weeks for equities. After months of trading in a sideways range, the war in Iran has put an added weight on the bearish side of the scale, pushing stocks lower. All of the major US indices are below their 50-DMAs, and the 200-DMAs are now starting to come into play as well. The short-term key has been and will continue to be oil prices. With no spike this morning, equities are taking the opportunity to rally, and we’ve been picking up steam as the morning drags on. The S&P 500 is on pace to gap up 0.75% as the open, while the Nasdaq is up closer to 1%. Now, let’s see if the gains can hold!

Outside of equities, treasury yields are falling with the 10-year yield down 5 bps to 4.24%, and crude oil falls almost 2% to just under $97 per barrel. Gold prices are down just over 1% and barely hanging on to $5,000, while bitcoin is up nearly 3% and above $73K.

Asian stocks were flat to higher to start the week on the optimism that oil prices didn’t spike more after the weekend. Japanese stocks traded down 0.1% while China was down 0.8%. Hong Kong, India, and South Korea, however, all rallied more than 1%. The declines in China came despite better-than-expected February data for Industrial Production, Retail Sales, and Fixed Investment.

European stocks have taken a more muted start to the week. The STOXX 600 is down 0.1% while Germany is up 0.3% and Italy drops 0.3%. It will be a busy week for central banks on the continent as the ECB, BoE, and SNB all have meetings.

It’s a relatively busy day for economic data this morning, with the Empire Manufacturing report for March hitting the tape at 8:30, followed by Industrial Production and Capacity Utilization at 9:15. Homebuilder sentiment will come out at 10 AM. Another area of focus today will be on Nvidia (NVDA) as CEO Jensen Huang will give the keynote speech at his company’s GTC conference at 2 PM Eastern. Looking ahead, the Fed will announce its latest policy decision on Wednesday.

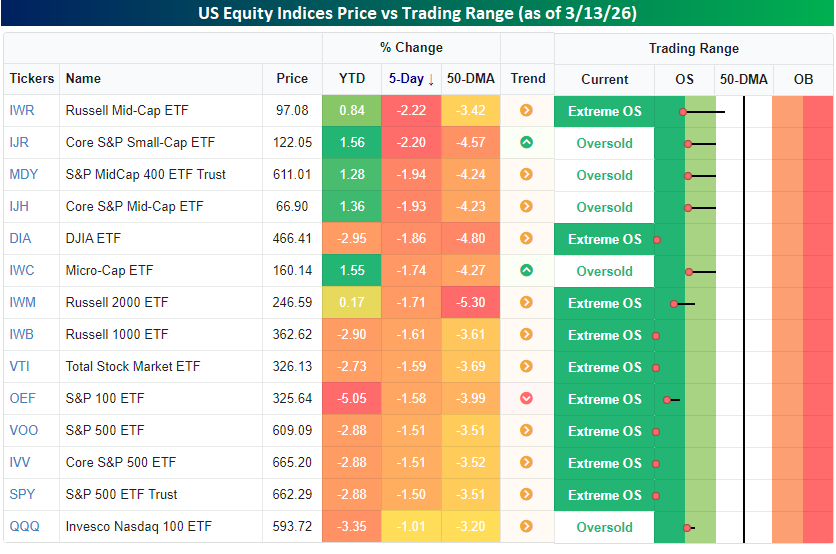

The S&P 500 has declined for four straight weeks now, but still hasn’t even declined 5% from its closing high in late January, so while it’s been a slump, it could be worse. Even with the relatively modest declines, as we discussed in Friday’s Bespoke Report, it still finds itself in what we consider ‘extreme’ oversold levels as it closed more than two standard deviations below its 50-DMA. Along with the S&P 500, the majority of other US index ETFs also finished off last week in extreme oversold territory, and the ones that aren’t are still in oversold territory.

Last week, there was a little bit of rotation in the market where the indices that had been performing the best YTD (small and mid-caps) experienced the largest declines, while large caps, which had been the weakest, were down less. It’s all relative, though, as even the best-performing US indices last week were still down over 1%.

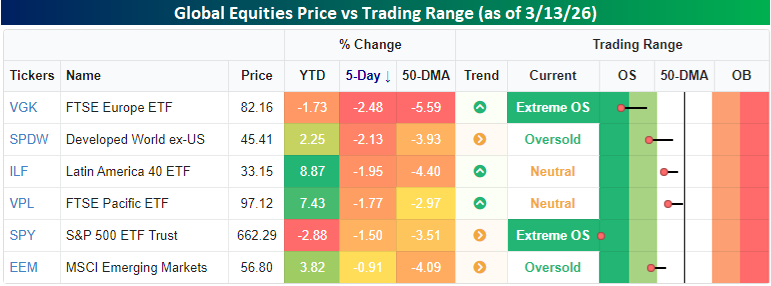

Similar to the relative outperformance of large caps versus small caps last week, US stocks outperformed their global peers once again last week, further digging out of their relative hole on a YTD basis. While the S&P 500 was down 1.5%, European stocks traded down by 2.5% last week, putting them into ‘extreme’ oversold territory with the US. The only areas of the world not oversold heading into the new week are Latin America (ILF) and Asia Pacific (VPL).

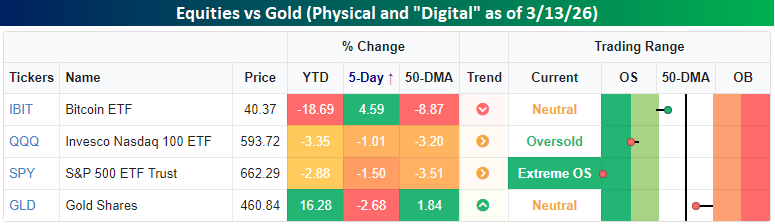

With equities under pressure, investors must be taking shelter in the safety of gold, right? Not really. Physical gold hit a speed bump last week, falling more than 2.5%. Despite the decline, though, it’s still up over 16% YTD and above its 50-DMA, so don’t shed too many tears for the gold bugs. One area of surprising strength last week was in Bitcoin (IBIT). While it’s still down close to 20% this year, it managed to rally more than 4.5% last week. As they say, even a broken clock is right twice a day.