See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Don’t let what you cannot do interfere with what you can do.” – John R. Wooden

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The market has one more day to salvage what’s been a negative week for stocks, and so far, it’s making a valiant effort. Futures on the S&P 500, Nasdaq, and Dow are all up 0.39%. With today being both Friday the 13th and the last day of trading into a weekend, it’s surprising to see equities catching a bid. Treasury yields are modestly lower, with the 10-year yield at 4.25%, and oil prices are down 2% to $93.50 per barrel. Gold prices are also pulling back, but Bitcoin is trading up close to 3% and above $72K.

Asian stocks ended what was already a down week on a negative note. The Nikkei was down over 1%, which took its weekly decline to over 3%, while China finished the week with a 0.7% decline, and India was down over 5%. Higher oil prices are a major pain point for the Asian economy, so the longer the Strait of Hormuz remains cut off, the more pressure it will put on these economies.

Equity performance has been more muted in Europe. The STOXX 600 is little changed for both the day and week, and no major index in the region is up or down more than 0.5% on the day. Industrial Production for January fell 1.5% versus expectations for an increase of 0.6%. Weaker growth, coupled with increasing inflationary pressures from rising energy prices, is the type of cooking markets would prefer not to see on the menu.

The economic calendar is jam-packed this morning with most of the reports (Personal Income, Personal Spending, GDP, PCE, Durable Goods) hitting the tape as we send this out, but at 10 AM Eastern, we’ll also get Michigan Confidence and JOLTS.

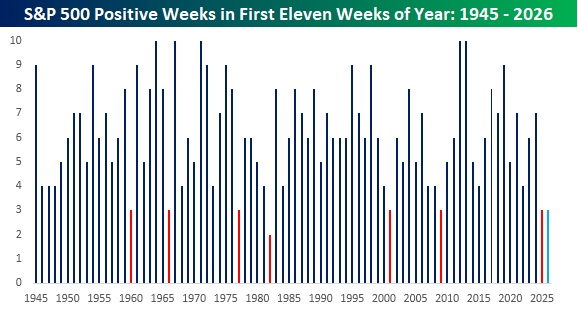

With the S&P 500 down 1% on the week heading into today, we’re on pace for the eighth negative week in the first eleven weeks of the year. With just three positive weeks, it’s been one of the weakest starts to a year for the S&P 500 in the post-WWII period. If the S&P 500 doesn’t rally more than 1% today, it will be the eighth year since 1945 that it has had three or less positive weeks to start a year. Ironically, last year also started weak, and while the market remained shaky through early April, it ended up being a good year. Before last year, the last time the year started out this inconsistently was in 2009, and the only year where there were fewer positive weeks to start a year was in 1982.

Two groups you would expect to benefit from the war in the Middle East are energy and defense stocks. Right out of the playbook, Energy stocks have rallied since the war broke out, but defense stocks have taken a sell-the-news response.

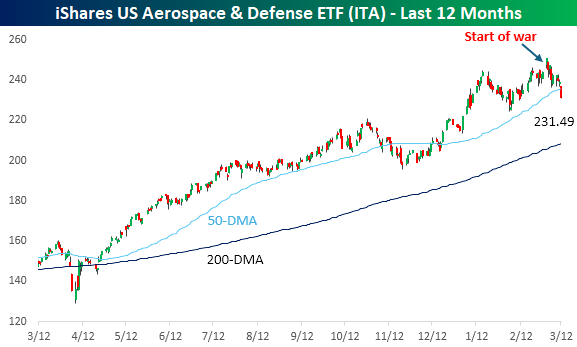

The chart below shows the performance of the iShares US Aerospace and Defense ETF (ITA) over the last year. While the ETF has surged over the last 12 months, it has struggled since the first missiles were fired. While ITA gapped up the Monday after markets reopened for trading after the war started, it’s been drifting lower ever since. Yesterday, it closed below its 50-DMA for the first time this year, and as Bloomberg noted in a news story overnight, the ETF had the largest outflow of assets in its history yesterday. Understandably, investors would take profits after the rally of the last year, but it’s interesting to see it follow the opposite path of Energy stocks.

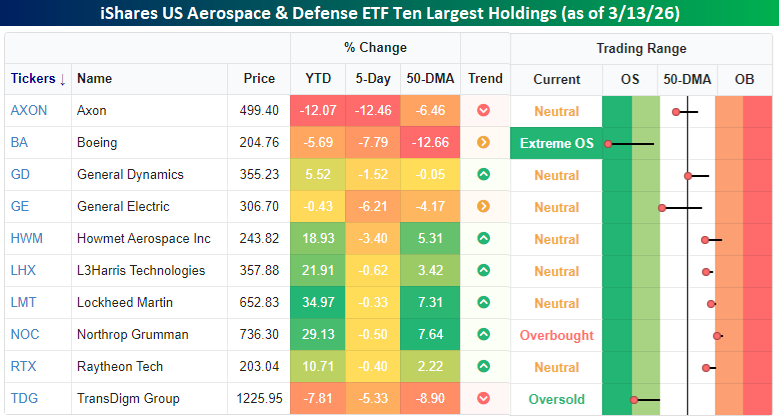

Below, we show the ten largest holdings in the ITA ETF and where each one closed relative to its trading range yesterday. Over the last week, all ten stocks are lower and some by a lot. General Electric (GE) and Boeing (BA) are the ETF’s two largest holdings, and both stocks are down more than 6% in the last week alone. For BA, that decline has taken it more than 12% below its 50-DMA and into ‘extreme’ oversold territory (2+ standard deviations below 50-DMA).