See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great things are not accomplished by those who yield to trends and fads and popular opinion.” – Jack Kerouac

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Money Movers yesterday to discuss the moves in the energy market and their impact on the equity market. To view the segment, click on the image below.

After a mixed session yesterday where the Nasdaq finished up 8 basis points (bps) while the S&P 500 fell 8 bps, US futures are firmly lower this morning, with the S&P 500 and Nasdaq both indicated to open down by about 35 bps. The primary culprit is crude oil, where prices are up over 5% and back above $90 as Iran stepped up attacks on tankers in the Persian Gulf. Energy Secretary Chris Wright was also just on CNBC and noted that the US is not yet ready to escort tankers through the Strait of Hormuz, but could be mobilized later this month. As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy.

With crude oil prices rising, treasury yields are higher again as investors focus on the potential inflationary impacts. Gold prices are essentially flat, silver is up 2%, and Bitcoin is down fractionally but still above $70K.

Stocks were down across the board in Asia overnight, as the Nikkei was down 1.0%, while China’s Shanghai Composite was only down 0.1%, and the Kospi fell 0.5%. Relative to the last two weeks, it was a muted session! Given the spike in crude oil prices and the region’s dependence on energy imports, you could make the argument that it could have been worse.

In Europe, equities are also taking the overnight spike in crude oil prices in stride. The STOXX 600 is down just 0.4%, while Germany is fractionally higher. We’re also starting to see impacts of the conflict showing up in corporate results as UK travel firm On the Beach lowered guidance, citing a sharp slowdown in travel bookings for locations in the Eastern Mediterranean.

On the economic calendar this morning, we just had jobless claims, Building Permits, and Housing Starts at 8:30. Initial claims came in 2K lower than expected, while continuing claims were 1K higher, so from this perspective at least, the labor market remains very well behaved. With respect to the housing numbers, permits were lower than expected (1376K vs 1410K) while starts were much higher than expected (1487K vs 1341K), although much of the strength was due to multi-family units.

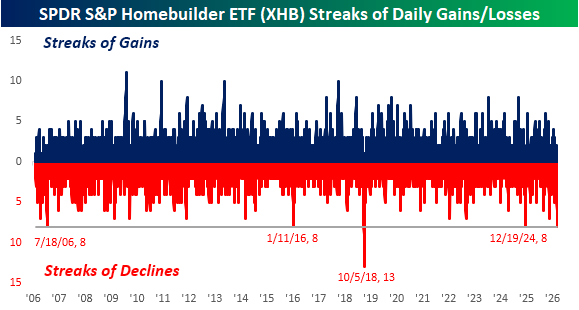

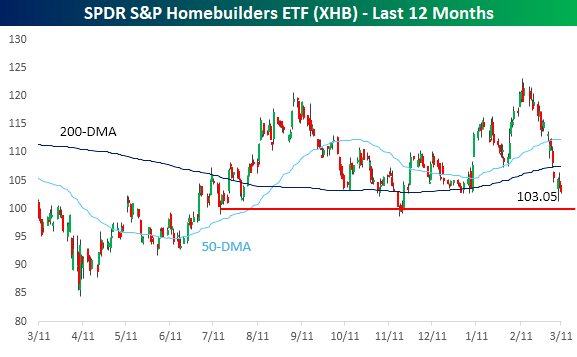

With treasury yields moving higher, it’s been a rough month for homebuilder stocks. The SPDR S&P Homebuilder ETF closed at $121.36 on 2/13, but has since declined more than 15% through yesterday’s close. Those highs in February were enough to push the group to 52-week highs, but the gains for 2026 quickly evaporated, and it’s now close to testing support at the $100 level.

Part of that 15% decline since the February highs includes what is now an eight-day losing streak, which is tied for the longest losing streak in the ETF’s entire history. The last time there was a streak this long was over a year ago in late 2024, and the only longer streak was 13 days ending in October 2018.