See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I attack ideas. I don’t attack people. Some very good people have some very bad ideas.” – Antonin Scalia

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be on CNBC at 11 AM Eastern to discuss markets and today’s CPI.

Futures were in a holding pattern ahead of today’s CPI, with the S&P 500 and Nasdaq both indicated to open down about 0.1% despite Oracle (ORCL) trading up over 10% in reaction to earnings. Treasury yields moved higher ahead of the report, with the 10-year yielding 4.17%, and crude oil was up over 4% to $87 per barrel. Gold and Bitcoin prices are down about 1%.

For Asian equities, the last several days have been something of an all-or-nothing trade where the major averages in the region are either all sharply higher or lower. Last night, there was more dispersion. While Japan and South Korea were both up 1.4%, Hong Kong was fractionally lower, and India declined 1.7%. In South Korea, exports for the first 10 days of March were up 55.6% y/y, with chip exports surging more than 175%. In Japan, PPI fell 0.1% versus expectations for an increase of 0.1%.

In Europe, the move was more uniform, and unfortunately for bulls, it was mostly lower. The STOXX 600 is down nearly 0.5%, with Germany leading the losses with a decline of nearly 1% as German CPI for February rose 0.2%, which was right in line with forecasts.

In the US, the only economic report on the calendar today is February CPI, which given the events of the last two weeks, has become much less pertinent to the market. While it may not be a major focus of the market this morning, CPI was right in line with expectations as headline increased 0.3% m/m and core increased 0.2%

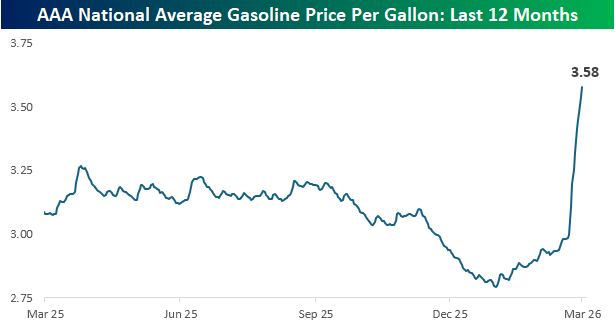

Through yesterday’s close, average prices at the pump have now surged to $3.58 per gallon, which represents a 20% increase this month alone. In the span of two months, prices have spiked from a 52-week and multi-year low to a 52-week high, easily surpassing the prior peak from last spring.

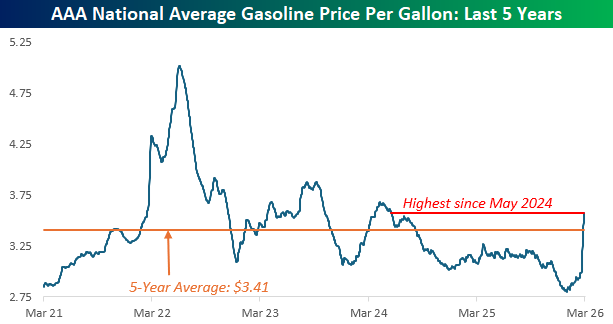

As shocking as the one-year chart looks, taking a longer-term look at crude oil prices shows a less dire picture. Current gasoline prices are now at the highest level since May 2024, but they’re still nearly 30% below the 5-year peak from June 2022, and less than 5% above the 5-year average. That doesn’t make it any easier to stomach, but at least it provides some decent perspective.

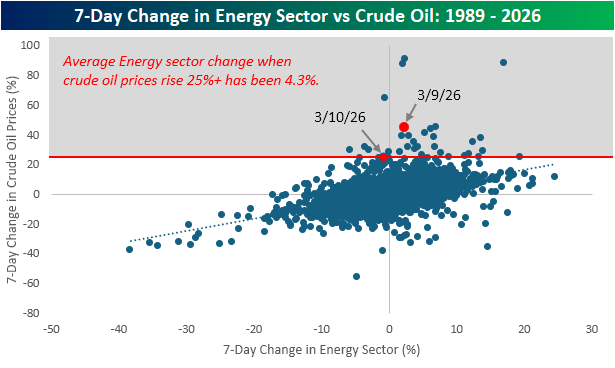

In the seven trading days since the war on Iran started, crude oil prices are up 25%, and as of yesterday, the seven -day change was over 45%. With such large increases, it seems like a disconnect that the S&P 500 Energy sector is up just 2%. The chart below compares the 7-day change in the S&P 500 Energy sector to the 7-day change in crude oil prices. While there has historically been a positive correlation between the two, in periods when crude oil prices have spiked 25% or more, the average change in the Energy sector has been a gain of 4.3%. The implication of those muted gains? The market views these price spikes as temporary.