See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we’re at a bottom. I really do.” – Mark Haines, CNBC, 3/10/09

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a dramatic reversal late in yesterday’s session on hopes that the war in Iran would be ‘complete’ soon, futures were higher for the overnight session and into this morning. As the opening bell approaches, though, futures have been drifting lower, and all of the major averages are on pace to open fractionally lower. Treasury yields are little changed, and crude oil has been volatile, sitting under $90 per barrel. While that seems low relative to Sunday night, it’s still much higher than anything seen in the months leading up to the war in Iran. Gold prices are up over 1.5%, and silver is surging 5% as it’s currently trading at the same price as WTI! Bitcoin has been quietly grinding higher over the last few days, and this morning, it’s above $70K.

Earnings season is largely in the rearview mirror, but after the close, we’ll hear from Oracle (ORCL), which could be a major catalyst tomorrow for different parts of the AI ecosystem. The only economic reports on the calendar today are small business optimism from the NFIB, which came in weaker than expected (98.8 vs 99.5), and then at 10 AM, we’ll get Existing Home Sales for February.

Asian markets followed the lead of the late-day reversal in US equities and traded sharply higher overnight. It wasn’t enough to entirely erase Monday’s losses, but the Nikkei rallied just under 3% while South Korea surged over 5%. Chinese stocks rallied a more modest 0.7%, and while February exports surged 39.6% y/y, exports to the US declined 17%. Those lost exports to the US were scattered across Europe and Southeast Asia, and many of those likely ended up finding their way into the US in a roundabout way. In Japan, GDP rose 0.3% q/q, which was higher than expected, and in South Korea, growth contracted less than expected.

European stocks are also sharply higher this morning as the US reversal occurred after those markets closed for trading yesterday. The STOXX 600 is up 2.3%, and Germany, Italy, and Spain are all up over 2% as well.

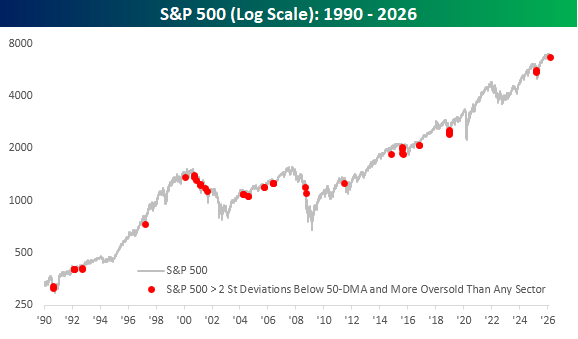

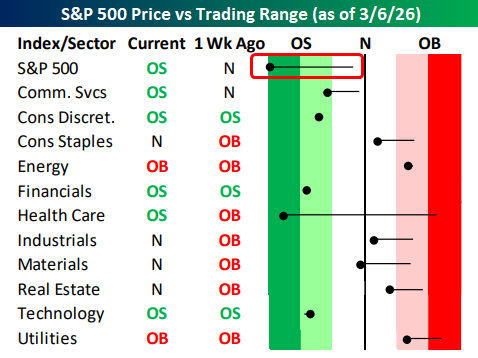

When you looked at page two of the Morning Lineup to see where sectors closed out last week relative to their trading ranges (image below), you may have done a double-take at seeing that the S&P 500 was in ‘extreme’ (2+ standard deviations) oversold territory and more oversold than any sector. In fact, the only other sector in extreme oversold territory was Health Care (after being in extreme overbought territory a week earlier), and just four other sectors were oversold while five were still above their 50-DMAs.

We were curious to see how often it is that the S&P 500 trades in ‘extreme’ oversold territory and is also more oversold than any other sector. Since sector data begins in 1990, there have only been 49 other days when this was the case, and a lot of them occurred during the dot-com bust from early 2000 to late 2001, but as the chart below illustrates, it’s hardly just a bear market phenomenon.