See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no instance of a nation benefitting from prolonged warfare.” – Sun Tzu, The Art of War

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If there’s ever a day that feels like a Monday, today is it. As much as we may like daylight savings time for the later sunsets, we could do without the later sunrises after already missing an hour of sleep. Couple that with triple-digit oil prices and much lower equity prices, and we almost wish our alarms didn’t go off this morning.

Equity futures are down over 1% across the board this morning, treasury yields are higher with the 10-year yield now up to 4.17% (it was below 4% less than two weeks ago), and WTI crude oil is up over 10% to $102 per barrel. Incredibly, that’s down around 15% from just under $120 overnight. There’s been no flight to safety in gold either, as prices are down over 1% there too.

Equities in Asia plunged overnight, with the Nikkei down over 5%, while South Korea fell 6.0% after circuit breakers were triggered during the session. In China, CPI for February rose much more than expected, rising 1% after an increase of 0.2% in January. And that was before the spike in oil prices. European equities are also down more than the US. The STOXX 600 is down 1.6% with France down over 2% and Spain down just under 2%. We can try to read into different catalysts for the weakness, but it’s pretty much all oil. Until those prices stop rising, equity prices will continue falling.

The economic calendar is quiet today, and there will be no Fedspeak as the blackout period ahead of next week’s meeting started this weekend. The economic calendar will be very busy, though, with CPI on Wednesday, Jobless Claims, Housing Starts, and Building Permits on Thursday, and Personal Income and Spending, as well as GDP, among others, on Friday.

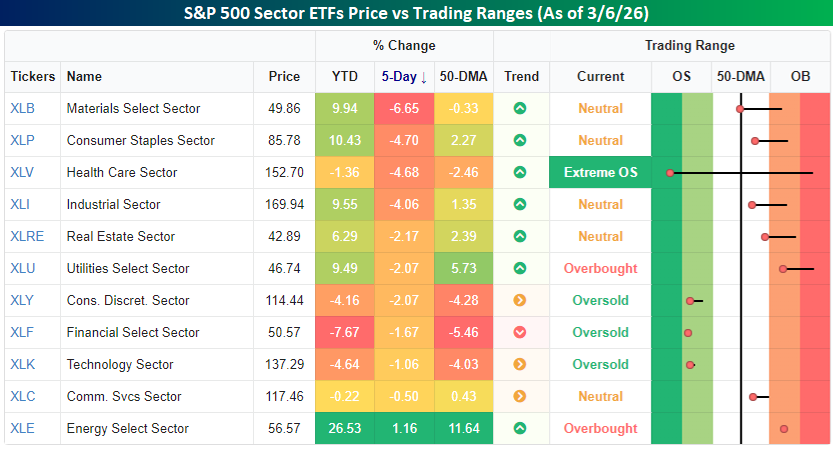

The war in Iran hasn’t had much of a benefit on any sector, except, of course, Energy. Since the fighting broke out just over a week ago, Energy has rallied over 1% while every other sector is in the red, with nine down more than 1%. Four sectors declined by over 4%, with Materials leading the losses at 6.65%, followed by Consumer Staples, Health Care, and Industrials. Health Care’s losses have taken that sector into ‘extreme’ oversold territory after trading in ‘extreme’ overbought territory just over a week ago. War has a way of changing market conditions very quickly!

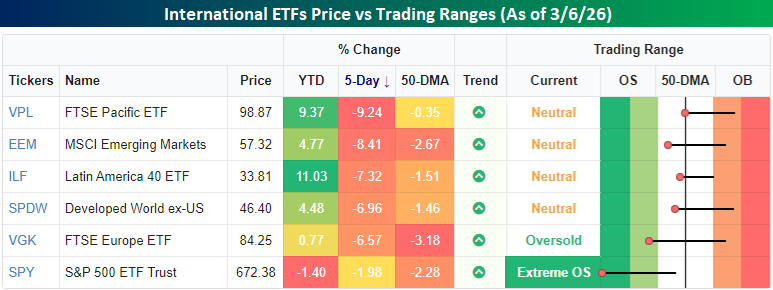

As bad as the US markets have been since the war broke out, it’s peanuts compared to the losses in the rest of the world. Below, we show the performance of various regional ETFs last week. While the S&P 500 was down nearly 2% last week, every other region of the world was down at least 6% and, in most cases, even more. Europe was down 6.6%, emerging markets were down over 8%, and stocks in the Asia Pacific region were down over 9%. As much as higher oil prices are a pain for US consumers and businesses outside of the Energy sector, other areas of the world are much more dependent on external sources for energy than the US.

In terms of the US vs. the rest of the world trade, the Developed World Ex US ETF was down nearly 7%, or five percentage points more than the S&P 500, in a week! As much as the US outperformed the rest of the world last week, it’s still significantly underperforming the rest of the world on a YTD basis (-1.4% vs +4.5%).

With the S&P 500 on pace to gap down 1% at the open for the fourth time in six days today, volatility has been on the rise, and the VIX is trading above 30 for the first time since last spring during the tariff-tantrum. Back then, though, the VIX briefly breached 60 before pulling back. So far during the current war, the highest the VIX has traded is 35.3. Last week may seem like a rough period for the markets, but relative to other points in just the last year, it could be a lot worse. The longer this conflict lasts and oil supplies remain disrupted, the more likely it is that conditions will worsen.