See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I never worry about the problem. I worry about the solution.” – Shaquille O’Neal

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Did you know that there’s an employment report today? With geo-politics in the forefront, economic data has largely taken a back seat this week, but the data will keep coming (unless there’s a shutdown, of course!), and heading into this morning’s report, the S&P 500 and Nasdaq are indicated to open down by between 0.75% and 1.0%, continuing a week of lousy market action. Treasury yields are higher, crude oil is surging, and gold is fractionally higher.

In Asia, most major indices were flat to lower, but still finished the week sharply lower, with the Nikkei down 5.5%, China down 2.1%, and South Korea down more than 10%. In Europe, the losses are even larger, with the STOXX 600 down over 1%, taking its decline for the week to over 5%. Across the continent, every major benchmark is down over 5% this week.

Besides the Employment report, Retail Sales also hit the tape at 8:30. The employment report was a disappointment across the board as Non Farm Payrolls fell 92K versus forecasts for an increase of 55K, and the Unemployment Rate increased to 4.4% versus forecasts for 4.3%. Average hourly earnings were slightly higher than expected, rising 0.4% versus forecasts for an increase of 0.3%. As bad as that report was, it will be interesting to see if there were any weather-related impacts. While the jobs picture was weaker, Retail Sales came in better than expected.

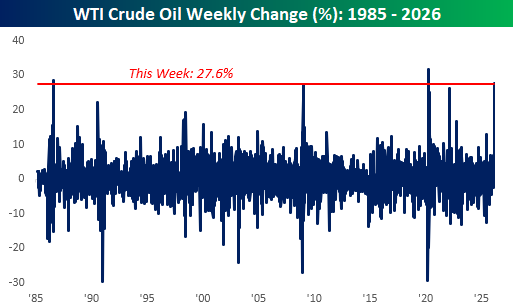

When markets opened for trading on Monday, and crude oil prices rallied a bit over 5%, it was viewed as a surprisingly muted reaction to a monumental event in the Middle East. It looked like we got off easy. As the days have gone on and the conflict has continued, crude oil prices rose every day this week with a 4.7% gain on Tuesday, a 0.1% gain on Wednesday, an 8.5% gain on Thursday, and what’s shaping up to be a 6.5% gain today. The frogs in the market pot had no idea what was coming.

Adding them all together, WTI is on pace for a 27.6% gain this week, which would rank as the third-largest weekly gain since at least 1985. The only two larger gains were 31% in early April 2020 during Covid and 28.4% in August 1986 when OPEC announced a surprise production cut. One-week rallies of this magnitude aren’t very common.

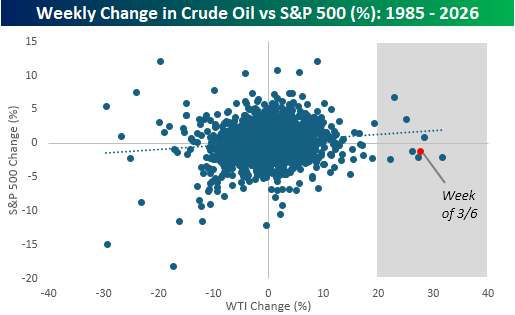

With oil prices up so sharply, it’s not surprising that equities have been under pressure, but looking at past moves shows that the inverse relationship isn’t as strong as you would think. The chart below compares the weekly change in crude oil to the S&P 500 going back to 1985, and there’s little correlation between the weekly direction of crude oil prices and the S&P 500. If anything, the correlation is slightly positive.

The shaded area includes each of the prior weeks when crude oil prices were up 20%, and of the seven occurrences, the S&P 500 was up three times and down four. For all seven weeks, the S&P 500’s median decline was 1.2%. Based on where futures are trading right now, guess how much the S&P 500 is down this week? 1.2%!