See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If what you have done yesterday still looks big to you, you haven’t done much today.” – Mikhail Gorbachev

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Markets are poised to open the week sharply lower following the start of the war in the Middle East. Both the S&P 500 and Nasdaq are indicated to open down by over 1%, crude oil is sharply higher, gold is surging, and even Bitcoin is higher.

Overnight in Asia, major averages were all lower except for China, which rallied 0.5%. European markets are also joining in on the weakness, with the STOXX 600 down 1.5% and Spain and Germany both down over 2%.

It’s tempting to look at the initial moves in the opening hours of trading and extrapolate them to a specific endpoint, but we’d stress that we’re still very early in this process. While a short conflict would likely be received positively by the market, the longer it drags on, and the higher energy prices stay, the more of an economic/market impact this will have.

Markets are mostly reacting just as you’d expect given the news of the weekend. Crude oil is sharply higher, stocks are down, and the dollar is up. The only asset class not following the playbook is the 10-year yield. US Treasuries are actually selling off modestly this morning, with the yield on the 10-year up about 3 bps to 3.98%. Higher yields will inevitably raise questions over the sell America trade, but two points are worth highlighting. First, on Friday, yields closed right near 52-week lows even as PPI came in higher than expected, so there was certainly some front-running of the attack on Iran heading into the weekend. Secondly, it’s not just US yields that are higher. Sovereign yields are also higher by similar amounts in Europe as well, so the move is more a reflection of concerns over inflationary impacts of the war.

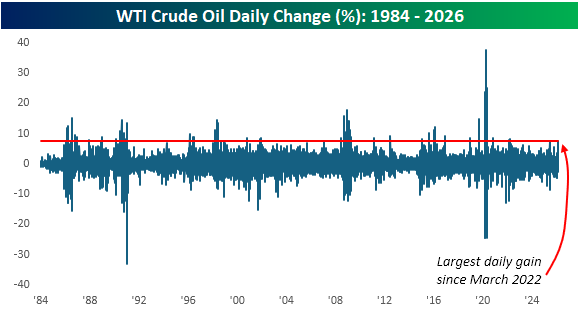

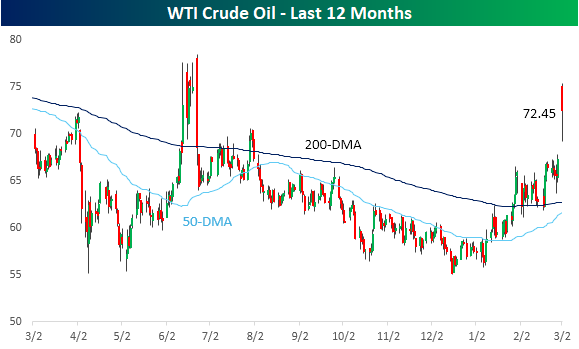

Crude oil has followed the playbook just as you would expect, though. If the pre-market gains hold through the end of the session, it will be the largest one-day rally in WTI crude oil since the early days of the Russia-Ukraine war in March 2022. While crude oil is off the highs from overnight, at over $72 per barrel, it’s right near its highest levels of the last year.

It’s been a large move, but today’s gain would only rank as the 80th largest one-day gain in crude oil since 1984. Given the enormity of the military action, an even larger move in crude oil wouldn’t have been a surprise.