See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To devastate is easier and more spectacular than to create.” – Anthony Burgess

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets are looking to build on yesterday’s turnaround Tuesday gains and are on pace to erase much of Monday’s losses, but whether these gains stick through the end of the week could depend on Nvidia’s (NVDA) report after the close. It’s widely assumed that the results will be strong, but will they be strong enough? And ff they’re too strong, will that also be interpreted as further future disruption in the software space?

Crude oil is higher this morning, trading just above $66 per barrel, even as Reuters reports that OPEC+ is considering a 137K barrel increase to daily production. Gold is also fractionally higher, back above $5,200 per ounce as silver surges 4% and platinum spikes 8%. Even bitcoin, yes bitcoin, is higher by more than 2%.

Asian stocks finished the day higher across the board, with the Nikkei up over 2% and South Korea up just under 2%. Chinese stocks also traded higher even as the Ministry of Commerce threatened to impose countertrade measures in response to the new tariff policies of the Trump Administration.

In Europe, stocks are also broadly higher but at a more restrained pace. The STOXX 600 is up 0.5%, led higher by 1% gains in Italy and the UK. Eurozone GDP fell more than expected (-0.6% vs -0.5% forecast) and German GDP was in line with expectations, growing 0.3% q/q.

Besides some important earnings reports after the close from NVDA and Salesforce (CRM), it’s a quiet day for data, but we will hear from many Fed speakers, including Barkin, Schmid, and Musalem.

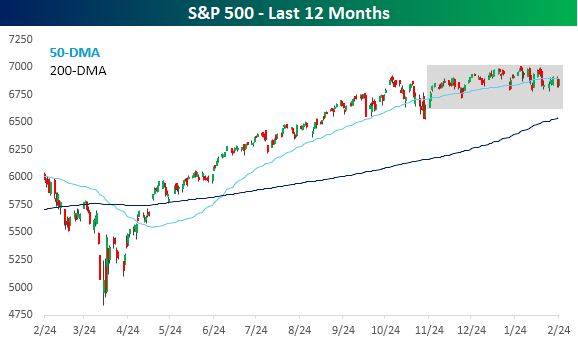

Given the ongoing weakness we have seen in certain areas of the market, which investors now think will be devastated by AI, it’s still hard to believe how range-bound the S&P 500 has been. Yesterday, the S&P 500 closed less than 0.1% below its 50-day moving average. You can’t get much closer than that! And it wasn’t just yesterday. The rangebound morass has been going on for months now, as there hasn’t been a day in the last three months where the S&P 500 closed more than 2.5% above or below its 50-day moving average.

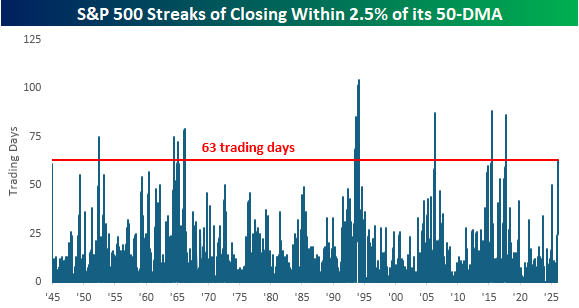

Periods where the S&P 500 has been so closely anchored to its 50-DMA haven’t been all that common throughout history. The chart below shows streaks when the S&P 500 closed within 2.5% of its 50-DMA (above or below), and the current streak, which reached three months (63 trading days) yesterday, is the longest since the first Trump administration in August 2017. Since WWII, there haven’t been many other extended periods where price was consistently so close to its 50-DMA.

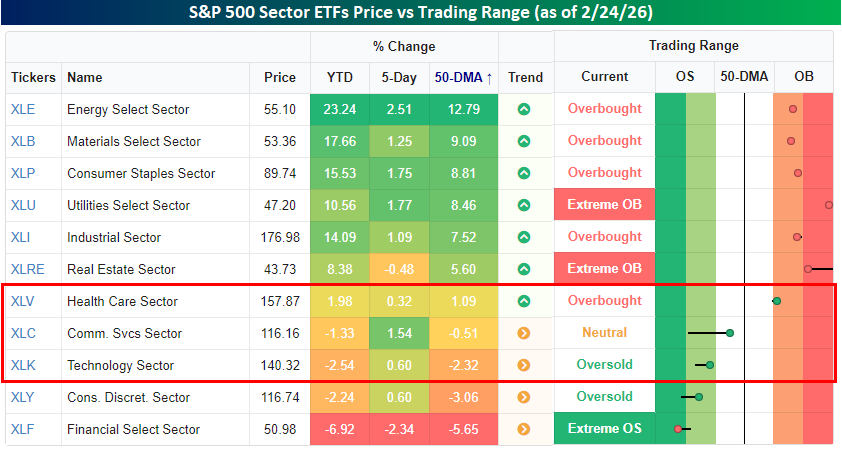

What makes the current streak even more incredible is that most sectors haven’t been showing the same pattern. As of yesterday’s close, just three of eleven S&P 500 sector ETFs – Health Care (XLV), Communication Services (XLC), and Technology (XLK) – closed within 2.5% of their 50-DMAs, and most sectors aren’t even close. Six are more than 5% above their 50-DMAs, and another is more than 5% below its 50-DMA. Like a sleeping volcano, the S&P 500 looks placid from above, but underground, the molten lava bubbles.