See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’ve missed more than 9000 shots in my career. I’ve lost almost 300 games. 26 times, I’ve been trusted to take the game-winning shot and missed. I’ve failed over and over and over again in my life. And that is why I succeed.” – Michael Jordan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It may be Tuesday morning, but futures are in a Monday mood as the S&P 500 is indicated to open down by 0.40% while the Nasdaq is down double that. The main culprit is the software sector as iShares Expanded Tech Software ETF (IGV) is down 1% in the pre-market, continuing a trend that has been in place for weeks now.

Treasury yields are also lower as the 10-year trades below 4.03%. Will we see a 3-handle this week? While yields are lower, crude oil prices are rallying over 1% to nearly $64 per barrel as President Trump made comments over the weekend that regime change “would be the best thing that could happen” in Iran. Despite the higher oil prices on geo-political concerns, though, gold prices are down 2% and back below $5,000, while silver is down over 4%. Along with lower metals prices, Bitcoin and other crypto assets are also down about 1%.

It was a quiet session in Asia as most markets are closed for the Lunar New Year. Japan was open for trading, though, but with a drop of 0.4% in the Nikkei, maybe it should have stayed closed too!

In Europe, it’s been a more positive tone as the STOXX 600 is up fractionally, led by larger gains in Italy and Spain. Economic sentiment, as measured by ZEW, was significantly weaker than expected, which perhaps makes the odds of rate cuts more likely.

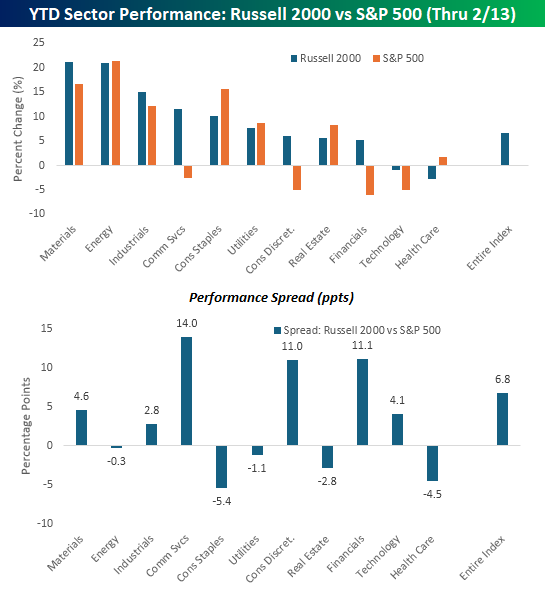

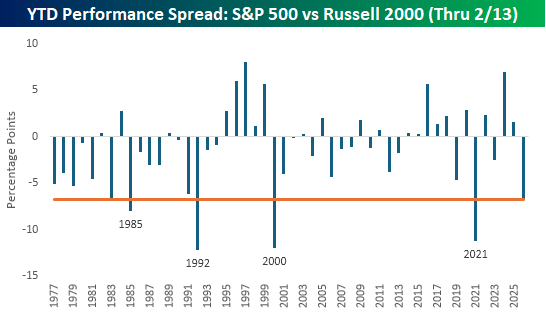

The S&P 500 went into the holiday weekend with a modest decline of 0.14% on a YTD basis, but the small-cap Russell 2000’s performance looks entirely different, as that index has already gained 6.64%. With 6.8 percentage points separating the two indices, small caps are off to their best start relative to large caps since 2021 and the fifth-best start to a year in the index’s history. The only other years besides 2021 when small caps got off to a better start were in 2000, 1992, and 1985.

For most sectors, the performance disparity between small and large-cap stocks has been narrower. The top chart below shows the YTD performance (through 2/13) of each sector in both the Russell 2000 and the S&P 500, and the lower chart shows the performance spread between the two. As shown, the only three sectors where the performance disparity is wider than it is at the index level are in Communication Services, Consumer Discretionary, and Financials, and in all three cases, the disparity is, like it is at the index level, in favor of small caps.

Looking in the other direction, there are actually five sectors where large caps are outperforming their small-cap peers. The widest disparities in favor of large caps are in Consumer Staples and Health Care, but large-cap Real Estate, Utilities, and Energy are also outperforming.