See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Volatility obscures the future but does not necessarily determine the future.” – Peter Bernstein

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey appeared on CNBC’s Worldwide Exchange this morning to discuss AI disruption and other issues impacting the market. To view the segment, click on the image below.

US equity futures are higher across the board this morning, with gains ranging from 0.25% to 0.30%. Treasuries are also catching a bid with the 10-year yield falling 2 basis points to 4.16%. Oil prices are taking a rest and trading down fractionally, which is also the case for gold and silver. Crypto is catching a modest bid with Bitcoin prices inching up towards $68K.

In Asia, it was a mixed session. The Nikkei was down 0.02% after being closed for a holiday yesterday, but South Korean stocks were higher again as the KOSPI rallied 3.1%. Those types of moves for a major country benchmark were once considered out of the ordinary, but lately, multi-percentage point moves in the KOSPI (mostly to the upside) have become commonplace.

In Europe, stocks are trading higher across the board. The STOXX 600 is up 0.4%, and the German DAX is leading the gains with a rally of 1.3%. UK GDP for Q4 was weaker than expected, but outside of some individual earnings reports, it’s been a quiet session.

Here in the US, it’s also a quiet day for data. The main report will be jobless claims at 8:30, followed by Existing Home Sales at 10. Since it’s Thursday, the weekly individual investor sentiment survey from AAII showed that optimism towards the stock market fell for the second week in a row to 38.5%, its lowest level since Christmas. Bah humbug!

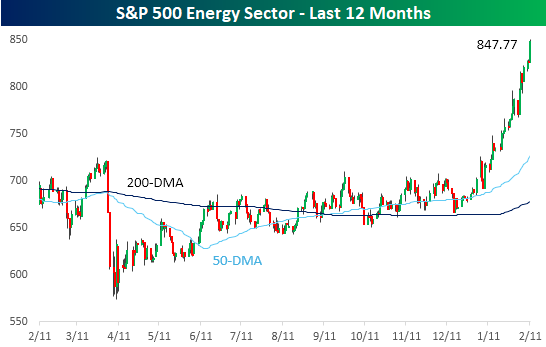

You need energy for a rocket to lift off, and boy, does the Energy sector have a lot of it! After essentially trading rangebound for the second half of 2025, the sector broke out in mid-January and has been gaining altitude ever since.

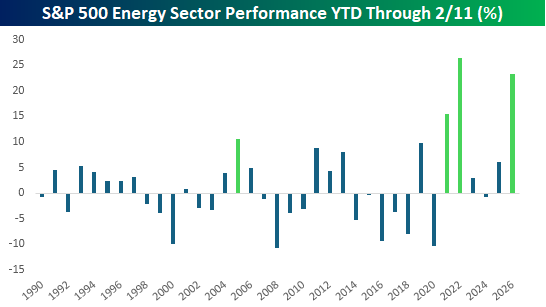

While most sectors have outperformed the S&P 500 YTD, none of them hold a candle to Energy’s gain of over 23%. Since sector data begins in 1990, this year’s gain ranks as the second-best start to a year through 2/11, trailing only the 26.5% gain to start 2022. That was a bit of a different situation, though, as the market was gearing up for Russia’s invasion of Ukraine. This year also now ranks as just the fourth year since 1990, that the Energy sector was up at least 10% YTD through 2/11. The others were 2021 and 2005.

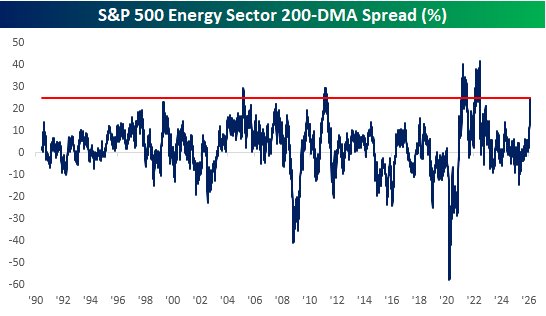

As the sector’s price has gone parabolic over the last few weeks, the spread between the Energy sector’s price and 200-DMA has ballooned to one of its highest levels on record. The only times it was wider were in 2005, 2011, 2021, and 2022.