See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest minds are capable of the greatest vices as well as of the greatest virtues.” – Rene Descartes

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Anticipation is the word of the morning, as markets waited for the delayed January jobs report. Heading into the report, S&P 500, Nasdaq, and Dow futures were all up a modest 0.10%. The 10-year yield was down a basis point to 4.13%, and crude oil was up over 2% and back above $65 per barrel. Precious metals are back in rally mode as gold rallies 1.5%, silver surges 6%, and Platinum rises 4%. Crypto, meanwhile, is struggling as Bitcoin pulls back 3% and trades back below $67. Metals rallying, crypto falling? Looks like things are getting back to normal!

The January payrolls report just hit the tape, and it was higher across the board. Non-Farm Payrolls were twice as much as expected (130K vs 65K), while the Unemployment Rate dropped to 4.3% 4.4% expected. Average hourly earnings and the average workweek were also both higher than expected. In response to the report, the 10-year yield ripped higher to just under 4.2% while equity futures added to their gains.

Japan was closed overnight, but most other major benchmarks in the region finished the session higher, with Australia rallying 1.6% while South Korea added another 1.0%. South Korea reported an 44.4% y/y increase in exports during the first ten days of February, aided by a 138% increase in chip exports. In China, January CPI came in weaker than expected, rising 0.2% versus an expected 0.3% increase.

In Europe, the STOXX 600 isn’t closed, but it’s unchanged on the session. The FTSE 100 is up nearly 1%, but every other major benchmark in the region is lower. It’s been a quiet session in terms of economic data, with Italian Industrial Production (better than expected) being the only major report on the calendar.

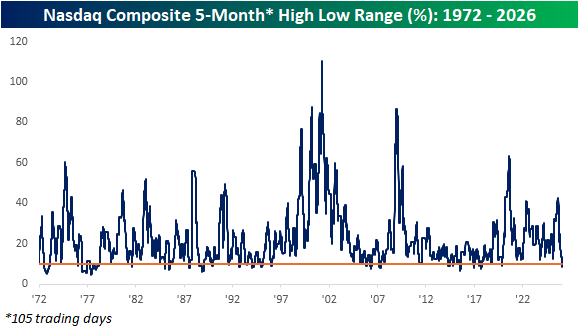

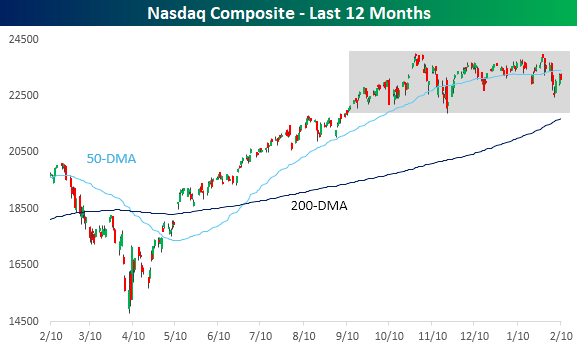

If I told you that software stocks had lost a third of their value over the last five months, you’d say the Nasdaq was in a deep correction, at minimum. Conversely, if I told you that the number of stocks hitting new 52-week highs was routinely at the highest levels in at least a year, you’d be asking when the Nasdaq crossed 25,000. Well, both trends outlined above have played out, but neither assumed result has played out for the Nasdaq, as both forces have essentially cancelled each other out, creating a period of stasis that has been going on for the last five months.

With the Nasdaq basically going nowhere since September, the spread between the index’s closing high and low recently dropped below 10%, and as of yesterday’s close, it was just 8.7%. That’s the first time that the five-month trading range dropped below 10% since 2019, and the narrowest range since October 2017. Back in the mid-teens, the Nasdaq’s five-month range was routinely below 10%, but since 1972, it has only occurred on less than 10% of all trading days.