See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“All the measures of the Government are directed to the purpose of making the rich richer and the poor poorer.” – William Henry Harrison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be appearing on Investopedia’s Express Live today at 10:00 AM Eastern. You can view the segment on YouTube or LinkedIn.

Whether it’s staying up late watching the Super Bowl last night or too much excitement from Friday’s rally that took the DJIA above 50K for the first time, US equity futures are subdued to kick off the week. The S&P 500 is on pace for a decline of 0.15% at the open, while the Nasdaq is down twice as much. Down, but nothing major.

Outside of equities, yields are higher with the 10-year yield up 4 bps to just under 4.25%. Crude oil is modestly higher, erasing earlier losses, while gold has bounced back above $5K per ounce and silver rallies 4% to get back above $80 per ounce. Crypto had a respite from selling on Friday and moved back above $70,000, but the bounce hasn’t lasted long. This morning, we’re not only back below $70K but barely hanging onto $69K.

There’s not a lot on the data calendar today, but we will hear from a few Fed officials. More importantly, December Retail Sales will be released tomorrow, the January Non-Farm Payrolls report will hit the tapes on Wednesday, and then on Friday, we’ll get CPI for January.

Asian markets took the cue from Dow 50K on Friday and kept the rally going to kick off the week. The Nikkei surged almost 4%, while South Korea rallied just over 4%. Snap elections in Japan were positive for PM Takaichi, giving her party a supermajority, which should pave the way for her to implement her high-spending growth agenda.

In Europe, the tone isn’t quite as exuberant this morning, but stocks are broadly higher. The STOXX 600 is up 0.3%, and the UK is the only major benchmark facing losses. The February Investor Confidence survey from Sentix came in higher than expected as it unexpectedly moved into positive territory.

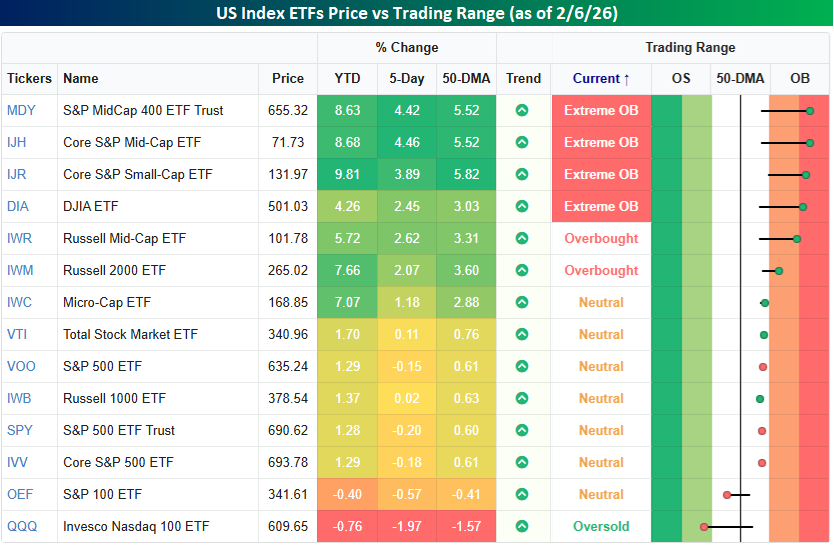

The diverging performance of small and large-cap stocks continued last week. The most overbought US index ETFs to close out the week are all generally smaller-cap and non-tech focused, while anything associated with mega-caps was down. In a week when the Dow (DIA) was up over 2% and closed at an all-time high, the Nasdaq 100 (QQQ), S&P 100 (OEF), and even the S&P 500 (SPY) were all lower. The Nasdaq 100’s 2% decline moves that index not only below its 50-DMA but also into oversold territory. At the other extreme, smaller and mid-cap indices, along with the Dow, are at various degrees of overbought levels.

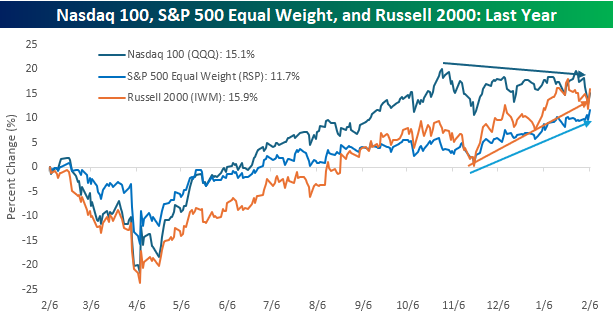

Looking at the performance of the Nasdaq 100, S&P 500 Equal Weight (RSP), and the Russell 2000 (IWM) ETFs over the last year shows an interesting shift. Since its peak last October, the Nasdaq 100 has been drifting lower while both the S&P 500 Equal Weight and Russell 2000 have rallied. The result is that the Russell 2000 is now outperforming the Nasdaq 100 over the last year, and the S&P 500 Equal Weight Index is rapidly closing the gap.

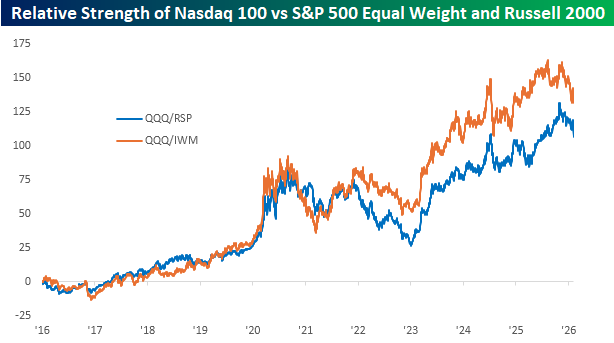

It’s been a rough three to four months for the mega-cap stocks relative to the rest of the market, but from a longer-term perspective, the recent underperformance of QQQ relative to RSP and IWM looks like much more benign as the longer-term trend remains intact. Whether that means this is just a temporary setback or that there’s much more mean reversion left in store remains to be seen, but for investors riding the mega-cap rally for the last several years are hanging on with white knuckles, hoping that, like the presidency of William Henry Harrison, this is a short stint.