See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best way to keep something bad from happening is to see it ahead of time… and you can’t see it if you refuse to face the possibility.” – William S. Burroughs

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures have been weakening all morning. As we approach the open, the S&P 500 is on pace to open down by more than 0.5% while the Nasdaq is down 0.75% as a 3% decline in shares of Alphabet (GOOGL) drags down the tech sector, even though the 50% increase in its CapEx plans should be a boost for the AI infrastructure trade.

With weaker equities, treasuries are catching a bid, and the 10-year yield is back down near 4.25%. Energy prices are significantly lower, with WTI down over 2% and below $64 per barrel. Volatility is even greater in the precious metals space as gold falls more than 1%, and silver is down over 10%. While strength in the precious metals never seems to give crypto an excuse to rally, today’s weakness has Bitcoin and Ethereum both down over 5% as the former is now below 70K.

In Asia last night, most major averages were lower on the session as the Nikkei declined 0.9% while South Korea’s KOSPI plunged 3.9%. The only index in the region to trade higher was the Hang Seng with a gain of 0.1%. There were no Asia-specific catalysts for the decline, as the weakness was more related to the overall tech sector fatigue.

European equities may not have as much exposure to tech, but they’re weaker across the board in early trading. The STOXX 600 is down 0.4% as Spanish equities lead the losses with a decline of 1.2%. Retail Sales in the Eurozone fell 0.5%, which was more than the 0.2% expected decline, and defense contractor Rheinmetall gave weak guidance.

Tuesday’s JOLTS report and Friday’s Non Farm Payrolls report have been delayed due to the shutdown, but jobless claims hit the tape at 8:30, and initial claims came in significantly higher than expected at 231K versus estimates for 210K. Continuing claims, though, were slightly lower than expected. On the earnings front, we also have another busy afternoon in store, headlined by Amazon.com (AMZN) after the close.

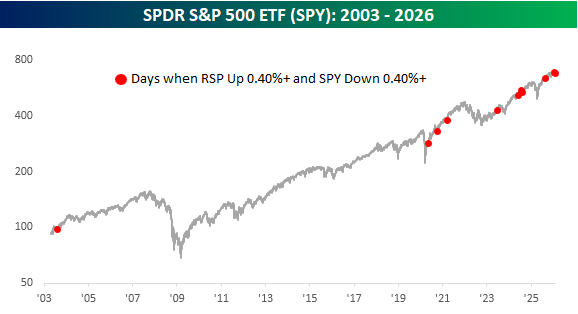

It’s only happened 11 times in the last 20+ years, but in the last three weeks, we’ve seen it occur twice. What is it? Yesterday, the SPDR S&P 500 ETF (SPY) fell 0.48% while the Invesco S&P 500 Equal Weight ETF (RSP) rallied 0.87%. That was just the 11th time since RSP’s inception in 2003 that SPY fell more than 0.4% while RSP rallied more than 0.4% on the same day. The most recent occurrence was in mid-January, and most have been in the last five years, as the top-heavy nature of the market has intensified, making disparities like yesterday less of an anomaly.

The chart below shows each occurrence on a chart of SPY. While it happened once in 2003, every other occurrence came after the Covid crash in 2020.

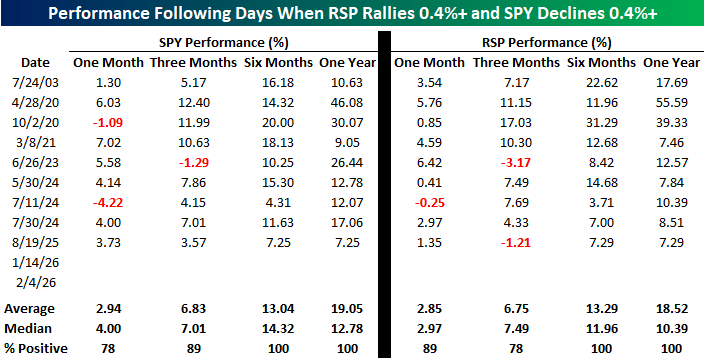

In the past, these types of performance disparities between the market cap and equal weight S&P 500 ETFs have been accompanied by ominous forecasts, suggesting that if the biggest stocks in the market were under pressure they would drag down everything else. The table below shows the opposite, though. Three months after the nine prior occurrences before this year, SPY was higher eight out of nine times, and RSP was up seven out of nine times. Six and twelve months later, they were both higher every time. We’re not sure how either ETF will trade in the months ahead, but past divergences like yesterday have been anything but an ominous pattern.

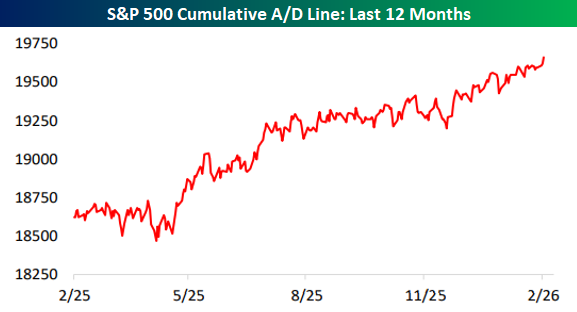

With RSP outperforming SPY yesterday, you can guess that breadth was positive, and that helped to push the S&P 500’s cumulative advance/decline line to a new all-time high. Certain heavily weighted sectors of the market have been under pressure recently, but overall breadth has been very strong.

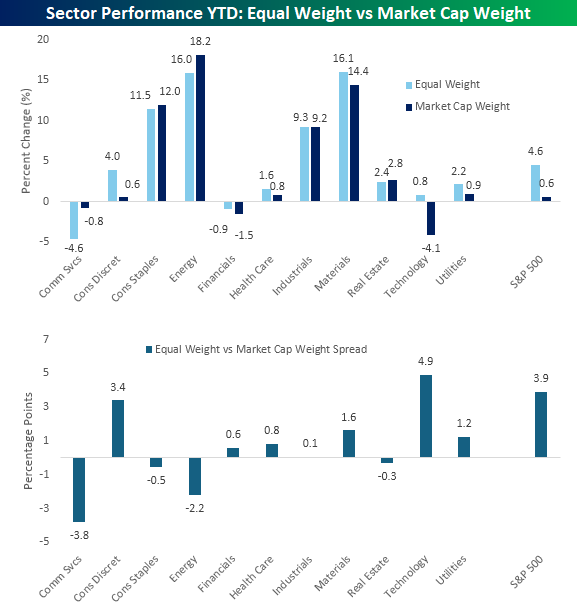

The trend of equal-weight outperforming market-cap weight this year hasn’t just been applicable at the index level. As shown below, the equal-weight version of seven different sectors are outperforming their market-cap weighted peers on a YTD basis. The biggest equal-weight outperformers have been Technology and Consumer Discretionary, while the cap-weighted versions of the Communication Services and Energy have been the biggest outperformers.