See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Wherever you come near the human race there’s layers and layers of nonsense.” – Thornton Wilder, Our Town

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss markets and precious metals. To view part of the segment, click on the image below.

Futures are modestly higher after investors look to pick up the pieces of yesterday’s rout in certain areas of the market. The S&P 500 is indicated to open 0.20% higher, while the Nasdaq is basically unchanged. AMD is the big loser this morning with a decline of 9% after the company reported better-than-expected earnings but raised sales guidance by less than some analysts had expected.

Outside of equities, treasury yields are little changed, and energy-related commodities are fractionally higher. Precious metals have been livelier in the early going as gold rallies back above $5,000, and silver pushes towards $90 with a gain of nearly 8%. The strength in those assets is once again not translating to the crypto space as Bitcoin is flat, and other secondary coins trade lower.

On the economic calendar today, we got ADP at 8:15, which showed positive job creation but at half the pace economists had expected (22K vs 45K). The ISM Services report hits the tape at 10 AM, and following Monday’s big surge in the manufacturing sector, the market will be looking to see how broad the rebound is. There’s another busy batch of earnings after the close, but Alphabet’s (GOOGL) report will likely have the largest market impact.

Despite the weakness in the US yesterday, Asian stocks mostly rallied overnight. The Nikkei was down 0.8%, but South Korea rallied more than 1.5% as PMI data for the Services sector topped expectations. In Europe, the STOXX 600 is also up over half a percent, and Germany is the only major benchmark trading lower. Unlike in Asia, where most PMIs for the services sector were better than expected, most European readings, except for France and Italy, were weaker than expected.

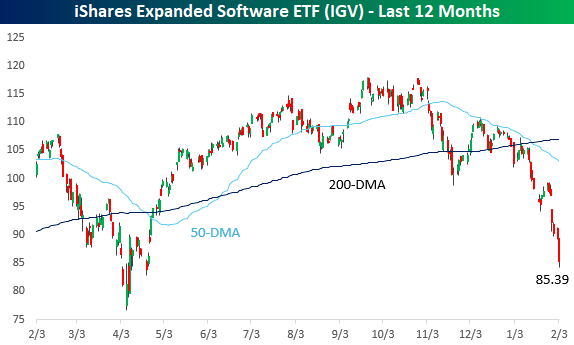

Yesterday was a rough day for the markets and especially technology, and with a decline of over 2%, it was easily the worst-performing sector on the day. Software stocks were especially hit hard as the iShares Expanded Software ETF (IGV) fell more than 4.5%, taking it down to levels not seen since the tariff-tantrum last April. Year-to-date, the ETF has already declined over 19%.

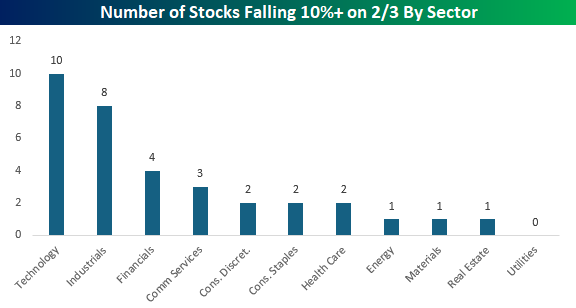

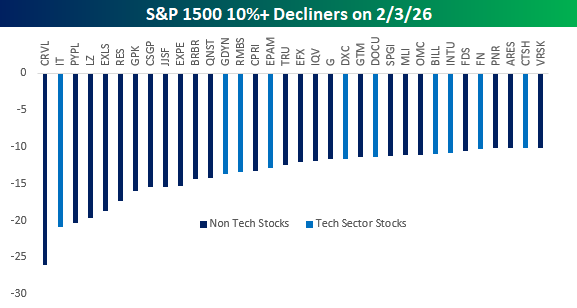

While tech stocks faced the brunt of the weakness, it was surprising to see that there weren’t more companies from the Technology sector on the list of worst performers yesterday. In the S&P 1500, 34 stocks fell more than 10%, and of those, 10 were from the Technology sector. Don’t get us wrong, ten is still a lot out of a universe of 34, but for a sell-off where attention was so focused on tech, other sectors weren’t immune. In the Industrials sector, you had stocks like Equifax (EFX), Transunion (TRU), and LegalZoom (LZ) all fall by double-digit percentages, while the Financials sector saw stocks like FactSet (FDS) and S&P Global (SPGI) experience major haircuts.

Remember, there are two sides to the growth of AI. In addition to the companies and sectors that will undoubtedly harness AI and benefit from it through increased productivity, there will also be those that have their entire business models upended and destroyed by AI. Apparently, it could happen faster than many investors think.

Finally, the chart below shows the sector breakdown of the 34 stocks that declined 10% or more yesterday. Tech obviously leads the list, but Industrials had eight stocks on the list, and Financials had four. In fact, the only sector not represented was Utilities.