See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Hi-yo, Silver! – The Lone Ranger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Warsh it is. After months of speculation in the horse race among potential candidates, President Trump announced his boardroom decision, and the winner of “The Apprentice: Federal Reserve” is Kevin Warsh. Futures initially sold off sharply when news of the nomination first hit the tape last night; they have since recovered much of those losses. The major averages are now looking at more modest declines of 0.50% or less. It remains to be seen how Kevin Warsh will act when he’s in the Chairman’s seat, and while he may be considered as more hawkish than some of the other nominees, he’s well respected by the street. Furthermore, all worries over Fed independence over the last six months can probably be put to rest.

It was a lower session to close the week in Asia, as major country benchmarks ended the week with mixed returns. Japan finished the week down 1% while China was down less than half that. On the upside, the Hang Seng had a much better week, rallying 2.4%, but couldn’t hold a candle to South Korea, which rallied 4.7%. Japanese yields pulled in a bit after Tokyo CPI decelerated from 2.0% to 1.5% y/y.

In Europe, it’s a much more positive tone this morning as the STOXX 600 is up nearly 1% with Spain’s 1.8% rally leading the way, although no major benchmark is up less than 0.5%. Banks are seeing some of the largest gains, but the rally has been broad-based with Energy and Materials being the only sectors in the red, while advancers outpace decliners at a 5-2 rate. In economic data, Eurozone GDP rose more than expected 0.3% while CPI in Spain declined more than expected (-0.4% m/m).

The only economic data on the calendar today in the US is PPI at 8:30 and Chicago PMI at 9:45, but the main area of focus will be the President’s nomination of Kevin Warsh to replace Powell. PPI came in much higher than expected on both a headline (0.7% vs 0.3%) and core level (0.5% vs 0.2%), so that has pushed futures down a bit again.

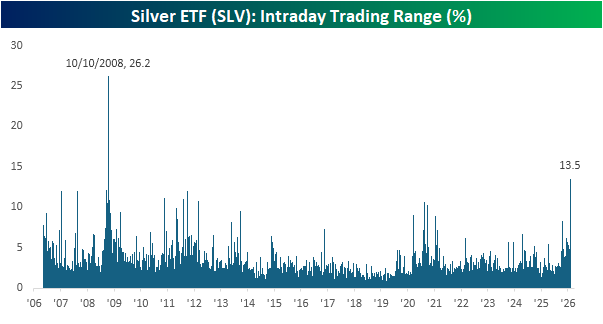

It seems fitting that on the anniversary of the Lone Ranger radio debut in 1933, we’re getting some historic moves in silver over the last 24 hours. Let’s start with the Silver ETF (SLV). In yesterday’s session, the ETF traded as high as $109.83 before cratering to $96.74 and then settling at $105.57. From its intraday high to its intraday low, though, SLV traded in a 13.5% range which was the second largest intraday range in the ETF’s history, trailing only the “marathon” 26.2% intraday range on 10/10/08 during the thick of the financial crisis.

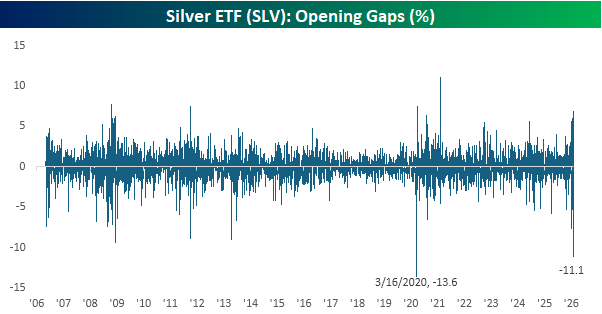

As if yesterday’s session wasn’t enough volatility for you, this morning, the SLV ETF is on pace to gap down 11.1%, which would be just the second time in its history that it opened down more than 10%. The only larger downside gap was a 13.6% decline on 3/16/20 during the heart of the Covid crash. In terms of yesterday’s range and today’s downside gap, recent activity in SLV is right up there with levels of volatility we saw during major market crises. What’s the issue this time around? The really amazing part about today’s downside gap in SLV, though, is that if current levels hold through the end of the day, it will still be up on the week!

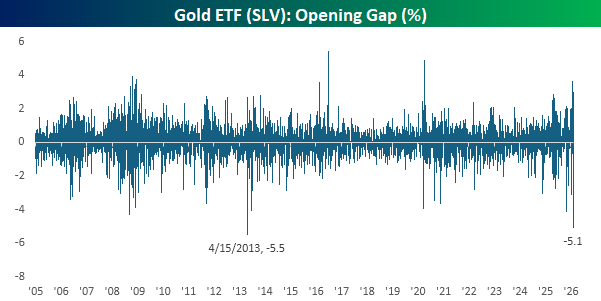

Not to be left out of the volatility party, gold is also poised for a rough start today. The Gold ETF (GLD) is on pace to gap down 5.1%, which would also be the second-largest downside gap in its 20+ year trading history. The only larger downside gap was on Tax Day in 2013, when GLD gapped down 5.5%. Like SLV, though, if current levels hold through the end of the trading day, GLD would also finish the week with a gain!