See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing makes a man so adventurous as an empty pocket.” – ― Victor Hugo, The Hunchback of Notre Dame

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are higher this morning, with the S&P 500 indicated to open 0.4% higher while the Nasdaq, driven by strong earnings from Taiwan Semiconductor (TSM), looks to open up nearly 1%. After weak reactions to earnings from the major banks over the last two days, Goldman Sachs (GS) and Morgan Stanley (MS) reported better-than-expected results but are experiencing muted to modestly negative reactions in their stocks.

Treasury yields are little changed, but at 4.14%, the 10-year yield is very well behaved. After surging above $62 per barrel yesterday as a strike on Iran seemed like a certainty, WTI is down over 4% and back below $60 this morning. Gold and other precious metals are also pulling back, but by much more modest amounts.

In Europe this morning, the STOXX 600 is up 0.5% as shares of ASML rallied more than 5% and saw their market cap exceed half a trillion dollars. Asian stocks were mixed overnight, with the Nikkei falling 0.4% (it can’t go up every day) while China was down a more modest 0.3%. South Korea, however, bucked the trend and rallied 1.6% (apparently, it can seemingly rally every day).

We just got a flurry of economic data, and the results were all stronger than expected. Both the Philly Fed and Empire Manufacturing reports topped expectations, and jobless claims were lower than expected on both an initial and continuing basis. Initial claims were even below 200K. The only fly in the ointment was Import Prices, which rose 0.1% m/m versus forecasts for a decline of 0.2%. In reaction the reports, yields ticked a little higher, and equity futures improved modestly.

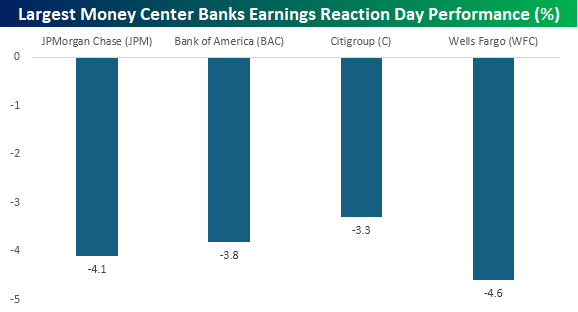

While large brokerage/investment banking-centric firms like Goldman Sachs (GS) and Morgan Stanley (MS) are seeing modest reactions to earnings, the same can’t be said for the largest money center banks, which reported this week. Bank of America (BAC), Citigroup (C), JPMorgan Chase (JPM), and Wells Fargo (WFC) all traded down at least 3% on their reaction days this week. For most, it was their worst earnings reaction day performance in over a year, and for BAC, it was the worst since October 2020!

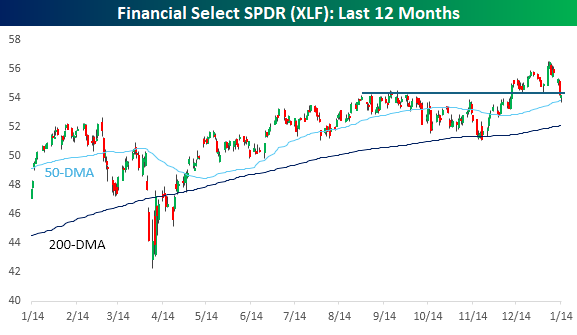

The weakness in the stocks has been a disappointment and a drag on the market this week, but keep in mind that these stocks were trading at record highs last week. They’ve also had to contend with the President’s call for a 10% cap on credit card interest rates. After the initial weakness yesterday, the Financial sector found some support at its 50-day moving average and ended up finishing the day right near the prior highs from last Fall. Provided the weakness eases from here, it’s nothing more than some consolidation.

The major banks are the first companies to report earnings every quarter, so their results and how their stocks react tend to get a lot of investor focus. Therefore, with all four reacting negatively to earnings, it raises the question of whether it’s a flock of canaries warning of bigger problems ahead.

The chart below shows the performance of the SPDR Financial Sector ETF (XLF) since 2000, and the blue dots indicate every time that all four money center banks declined on their earnings reaction days in the same earnings season, while the red dots indicate each time all four stocks declined at least 1%. There have been 14 other times that all four stocks declined on their earnings reaction day in the same earnings season, but there have only been three earnings seasons when all three declined 1%. Of those three, the only time all four stocks declined more than 3% was in April 2020 when the economy was shutdown from Covid! So, it’s uncommon to see all four stocks simultaneously react so poorly to earnings.