See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“While any number of risks continue, we are bullish on the U.S. economy in 2026.” -Brian Moynihan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey appeared on Making Money with Charles Payne yesterday to discuss the markets in the post-Covid world and what to expect in 2026. To view the segment, click on the image below.

After a modestly negative Tuesday, futures are trading on the back foot once again this morning. S&P 500 futures are down 0.36% while the Nasdaq is even weaker, indicated to open down by 0.5%. Oil prices are higher as traders eye the simmering tensions in Iran and anticipate a possible disruption to supplies from the country. That’s also translated to a flight to safety trade in gold and other precious metals. Gold is up 1%, silver is up over 5%, while platinum is up 3%. A few weeks ago, a lot of traders thought these moves were getting long in the tooth, but those teeth now look like fangs. Even crypto assets have caught a bid in recent days as Bitcoin is back above $95K and Ether is up near 3,300.

After yesterday’s tame CPI, we just got PPI along with Retail Sales. PPI was a strange report as the m/m numbers were either inline with or weaker than expected, but the y/y readings came in much higher than expected at 3% compared to forecasts for 2.7%. These are hotter than expected inflation readings, but PPI is a volatile report. Retail Sales, also released at 8:30, were better than expected. The only other report on the calendar is Existing Home Sales at 10 AM, and given the lower mortgage rates recently, we could see some strength in that report.

The pace of earnings is also starting to pick up as Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC) all reported results this morning. All three companies exceeded bottom-line forecasts, while WFC was the only one to report weaker sales. As a result of its revenue miss, WFC is trading down about 2% while the other two stocks are hugging the flat line.

In Asia overnight, it was a mixed session. Japan extended its streak of 1%+ daily moves to seven with a gain of 1.5%. China was down modestly (-0.3%), while South Korea was up 0.7%. In Europe, there’s been little movement so far this morning. The STOXX 600 is basically unchanged as most major benchmarks in the region are marginally higher, but modest weakness in Germany weighs.

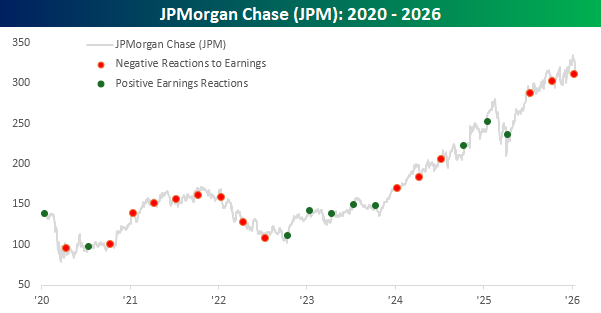

Yesterday’s 4%+ decline in shares of JPM ranked as the eighth most negative reaction to earnings for the stock since at least 2001 and the weakest since April 2024. The stock’s negative reaction to earnings raised some concerns surrounding the stock as well as the broader market, but as we noted in yesterday’s COTD, JPM’s reaction to earnings isn’t exactly a great bellwether for broad market. They’re not even a great bellwether for the stock’s future performance.

The chart below shows the stock’s performance since the start of 2020, and the red and green dots represent each of the company’s earnings reports since then. Red dots indicate days when the stock had a negative one-day reaction to earnings, while green dots indicate positive reactions. Yesterday was the third straight quarter that JPM had a negative reaction to earnings, but as the chart illustrates, the prior two weak reactions weren’t an especially ominous signal as the stock hit new all-time highs following each of them. JPM had a similar streak in 2024, and once again, between each of them, the stock hit all-time highs. From late 2020 through mid-2022, there was another extended streak of eight straight negative reactions, and while the stock held up well early on in that streak, towards the later stretch of that streak, the stock finally rolled over. All in all, though, a weak one-day reaction has tended to be a weak one-day reaction and nothing more.

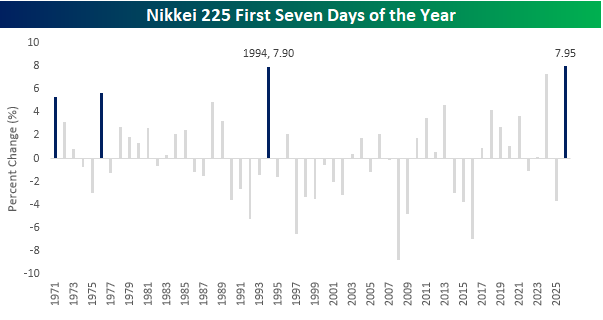

Moving on from JPM to Japan, last night’s rally in the Nikkei extended an impressive run to start the year. After just seven days of trading, the Nikkei is up 7.95%, which ranks as the best start to a year for that index since at least 1971. Before this year, the record was in 1994 when it rallied 7.9% in the first seven trading days. Besides 1994, the only other years that the Nikkei rallied more than 5% in the first seven trading days of the year were 1971, 1976, and, most recently, in 2024.