See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Maintain a firm grasp of the obvious at all times.” – Jeff Bezos

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As of early Sunday afternoon, it looked as though the news surrounding the anti-regime protests in Iran or the President’s call for a one-year cap on credit card interest rates at 10% would be the major news catalysts for trading to kick off the week. Then, last night, news broke that the Department of Justice had opened a criminal investigation into Federal Reserve Chair Jerome Powell related to the $2.5 billion renovation of the Federal Reserve’s headquarters. Powell responded that the investigation was “a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President.” He went on to add that this investigation will determine “whether the Fed will be able to continue to set interest rates based on evidence and economic conditions — or whether instead monetary policy will be directed by political pressure or intimidation.”

The President (as you would expect) denied any involvement in the investigation, and while it obviously looks political, the reality is that, provided he did nothing wrong, which we have no reason to believe he did, Powell should have nothing to worry about. The bigger question, in our mind, is who in their right mind would ever want Powell’s job? If I’m one of the Kevins, or any of the other people that prediction markets have as succeeding Powell, I’d be cheering every time my odds went down!

S&P 500 futures are down 0.5% leading up to the opening bell, while the Nasdaq is down 0.75%. Treasury yields are slightly higher, with the 10-year yield up 2 bps to 4.19%, while the dollar is lower. Crude oil is fractionally lower while gold is surging more than 2.5%. All these moves suggest a possible return of the ‘sell America’ trade; at this point, the moves are much too modest to suggest that it is a real concern.

Despite the weakness in US futures, Asian stocks kicked off the week on a positive note. While Japan was closed for a holiday, both onshore and offshore Chinese stocks were up over 1% while South Korea rallied 0.8%. India and Australia were also higher by about 0.5%. South Korea export data showed that while overall exports in the first ten days of January were down 2.3% y/y, chip exports increased over 45%!

In Europe, equities have started the week in a more muted fashion than Asia. The STOXX 600 is slightly lower, while German stocks buck the trend with a gain of 0.5%. There hasn’t been a lot of news specific to the continent this morning, but Sentix Investor Confidence for January did come in less weak than expected.

Before the Powell headlines broke yesterday, news earlier in the weekend about the President calling for a one-year cap of 10% on credit card interest rates looked like it would be the biggest news story heading into the new week. While the President can’t directly force the credit card issuers to cap interest rates, he can make life difficult for them through the bully pulpit of his Truth Social account and the various regulatory agencies that the issuers fall under the purview of.

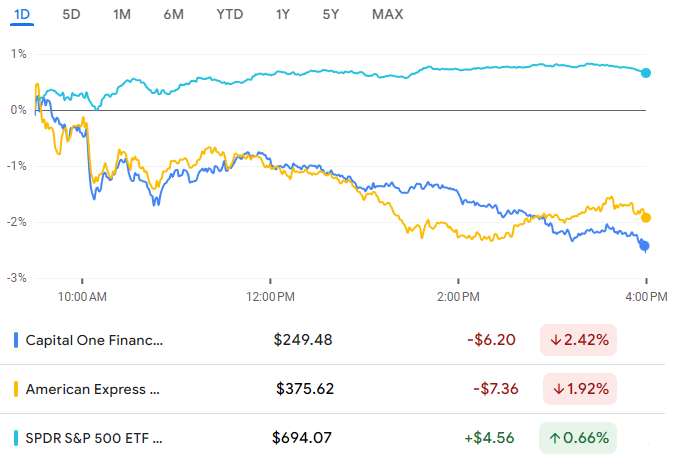

In response to the President’s comments over the weekend, American Express (AXP) and Capital One (COF), two of the biggest pure-play credit card issuers, are trading sharply lower. AXP is down over 4% while COF is down twice that, with a loss of over 8%. The Financial sector and banks, in general, are also weak today, but nowhere nearly as much as AXP or COF. The weakness in both stocks comes after they finished last week right near 52-week highs. Looking at the price charts of both stocks, though, you can see that they closed near their lows of the day last Friday (top two charts) while the S&P 500 finished the week right near its highs of the day.

The intraday performance of all three shows the divergence even more clearly. As the S&P 500 rallied intraday, both AXP and COF drifted lower all day. It’s hard to look at this chart and not think that someone knew something.