See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I got my start by giving myself a start.” – Madam C. J. Walker

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you thought it was time to start slowing down for the Christmas and New Year’s holiday, you may want to wait a little longer. Between a backlog of economic data and various agencies looking to get a jump on the holidays, there’s a lot of economic data on the calendar this morning. At 8:30, we’ll get the first read of Q3 GDP, Personal Consumption, GDP Price Index, Core PCE, and Durable Goods. Then at 9:15, we’ll get Industrial Production and Capacity Utilization. At 10 AM Eastern, the Richmond Fed will release its monthly update on business activity in the region for December, and the Conference Board will release its monthly Consumer Confidence. Finally, at 1 PM, we’ll get the weekly Baker Hughes Rig Count, which is normally a Friday report – on a Tuesday.

Ahead of the data deluge, equity futures are little changed but with a positive bias. Treasury yields are lower, with the 10-year yield down 2 bps and just under 4.15%. For all the concerns that the latest round of rate cuts would push longer-term rates higher, it really hasn’t happened. In the commodities space, crude oil and natural gas are trading fractionally higher, while metals prices are all up by at least 1% yet again. Finally, Bitcoin, which was once the asset that just couldn’t go down, has turned into the one asset class that can’t get out of its way as it trades down by about 1% in the low $87,000 range.

In Asia overnight, major averages were little changed, and the Nikkei was up just 2 bps. Other major indices weren’t much more volatile, as South Korea was the big mover with a gain of 0.3%. In Europe, it’s a similar story as the STOXX 600 is up 0.2% as those markets are already slowing down for the Christmas holiday.

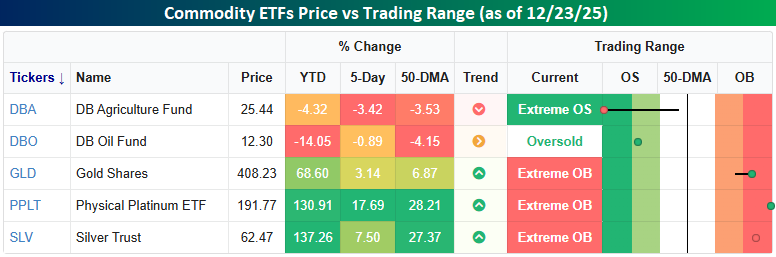

As mentioned above, metal prices are leading the gains in commodity prices this morning, which has essentially been the case all year. As shown in the snapshot from our Trend Analyzer below, anything commodity-related that doesn’t hurt when it’s dropped on your head hasn’t had much of a year in 2025. The DB Agriculture Fund is down 3.4% in the last week, taking its YTD decline to 4.3% and putting it in extreme oversold territory. Oil prices have also declined over the last week and are down over 10% on the year. Metals prices have gone parabolic, though. While gold is ‘only’ up 69%, Platinum (PPLT) and Silver (SLV) are up pretty much twice that!

Below we show one-year charts of each of the five ETFs highlighted in the snapshot above. Starting with the soft commodities, DBA and DBO are both testing 52-week lows as we close out the year, although the weakness in DBA is a bit overstated, as yesterday’s decline was due to the ETF trading ex a 91-cent return of capital dividend. In any event, it hasn’t been a good year.

While the soft commodity ETFs are testing downside support, GLD broke above potential resistance at its late October high yesterday. Platinum and Silver were at similar junctures in the last few weeks, and once they finally broke out, they were off to the races. Will Gold follow?