See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we obtain too cheap, we esteem too lightly: it is dearness only that gives every thing its value.” – Thomas Paine

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are limping into the last trading session of the week with the S&P 500 indicated up by a few basis points while the Nasdaq is indicated 0.15% higher. The 10-year yield is up 3 basis points, but still below 4.15%, and crude oil is up 1%, but still below $57 per barrel. Gold is essentially flat, putting it on pace for a gain of nearly 1% on the week, while Bitcoin is up over 3% as it attempts to erase some of the week’s sharp losses.

The only economic reports on the calendar this week are Existing Home Sales and UMich sentiment at 10 AM. While options expiration and a rebalancing in the S&P 500 could create some volatility, trading is likely to really slow down next week and into year-end

While it was a down week for stocks in Asia, they closed out the week on a positive note. The Nikkei rallied 1% but still finished down 2.6% for the week. China was up 0.4% and was unchanged on the week, while South Korea rallied 0.7% to soften its decline for the week to 3.5%. As expected, the BoJ raised rates 25 bps to 0.75%, which was the highest level in 30 years. While monetary policy in Japan is tightening, investors in China are speculating that the PBoC will loosen policy by lowering the reserve requirement early in the new year.

In Europe, the tone is less positive this morning as equity markets on the other side of the Atlantic snooze into the weekend. The STOXX 600 is down 0.1%, but still up over 1% for the week. Germany is poised to finish the week basically unchanged, while most other country benchmark indices are up over 1%. Inflation data in the region was mixed as German PPI for November was unchanged versus expectations for an increase of 0.1%, while French PPI increased 1.1%.

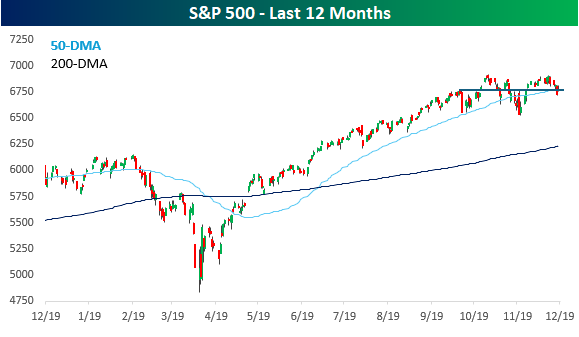

It’s hard to believe that the S&P 500 hit an all-time high a week ago yesterday, and yet as of yesterday’s close, it was barely above its 50-day moving average and essentially at the same levels it was at in early October. As Yogi Berra might say, the stock market is doing great. It’s just not going anywhere.

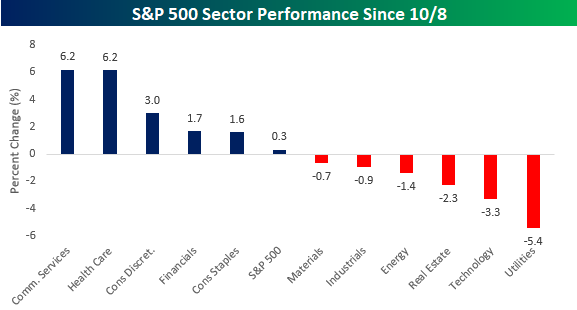

While the S&P 500 hasn’t really gone anywhere, sector performance has been disparate. Communication Services and Health Care are both up over 6%, and another three sectors have outperformed the S&P 500 gain of 0.3%. At the other end of the spectrum, Utilities is down over 5%, but right behind it, Technology has declined 3%. The fact that Technology, which makes up over a third of the S&P 500, has declined over 3%, and the market has treaded water, indicates a broadening of performance. It also illustrates how hard it is for the market to make headway without Technology participating.

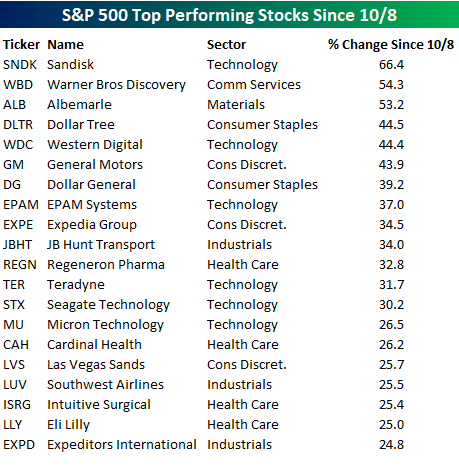

In terms of individual stock performance, of the twenty top-performing stocks in the S&P 500, 19 are up over 25%. Technology is the most heavily represented sector on the list with six, but the strength has been largely isolated to memory stocks, led by Sandisk (SNDK), which has rallied over 60% in just over two months! Besides Technology, six other sectors are represented, including Health Care with four, and Consumer Discretionary and Industrials with three each.