See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I can’t believe it, but it looks as though television has betrayed me.” – Bart Simpson, Episode 1, The Simpsons

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you think the seven-month winning streak in the Nasdaq has been impressive, think of this: today marks the 36th anniversary of the first episode of The Simpsons, when the longshot Santa’s Little Helper first cancelled Christmas for the Simpson family by losing his race at the dog track and then saved it when he was kicked to the curb and adopted by the Simpson family. Everyone who watched that first episode has aged quite a bit, but Homer, Marge, Lisa, Bart, and Maggie haven’t aged a bit, and Barney Gumble is still drunk down at Moe’s!

After a busy day for data yesterday, the calendar goes dark again this morning, but there is some Fedspeak to fill the void. Fed Governor Waller is speaking now in New York, and then NY Fed President Williams will speak just after 9 AM. Williams bailed out the bulls late last month, and the way markets have been trading over the last couple of weeks, they could use some market-friendly comments from him this morning. After these two morning speeches, the only other Fed speaker on the calendar is Atlanta Fed President Bostic at 12:30 Eastern.

Futures suggest a positive open for the market this morning, with the S&P 500 and Nasdaq both indicated to open about 0.4% higher. Treasury yields are giving back some of yesterday’s declines as the 10-year yield is back to 4.18%, and crude oil and gold are both trading higher. The same can’t be said for the crypto space, though, as Bitcoin and Ether are both down about 1%.

It took until Wednesday, but Asian stocks finally had a positive session with the Nikkei rallying 0.3%, China rallying over 1%, and South Korea’s Kospi rising 1.4%. In Japan, Machinery Orders for October unexpectedly increased 7.0% versus forecasts for a decline of 1.8%, and November export orders also rose at the fastest pace in nine months (+6.1%).

European stocks got off to more of a mixed start this morning. The STOXX 600 is up 0.3%, but Germany and France are both trading lower as Italy, Spain, and the UK gain. Investors got some good news on the inflation front as November CPI declined 0.3% m/m, which was in line with expectations, but the y/y reading increased slightly less than expected at 2.1% compared to forecasts for an increase of 2.2%. That weaker print all but green-lights a rate cut at tomorrow’s ECB meeting.

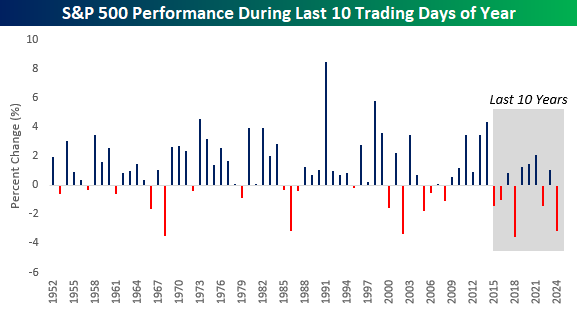

It’s time to let the countdowns begin as there are now just ten trading days left in 2025 (and five until Christmas!). December has historically been a strong month for the S&P 500, and while there has been a lull in the seasonal tailwinds, there’s still time left for them to blow. December has historically been a back-end-loaded month in terms of when the gains occur.

The chart below shows the S&P 500’s performance in the last ten trading days of the year for every year since 1952 (when the five-day trading week in its current form started). Just looking at the chart, it’s easy to see that positive ends to the year outnumber negative ones. It’s also much more common to have a solid gain to end the year than a sharply negative one. While there have only been five years when the S&P 500 declined 3%+ in the last ten trading days of the year, there have been thirteen when it rallied more than 3%, including gains of 8.5% and 5.8% in 1991 and 1998, respectively.