See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Sometimes reality is too complex. Stories give it form.” – Jean Luc Godard

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view this morning’s Squawk Box interview, please click the image below.

Yesterday was a true turnaround Tuesday as the S&P 500, Nasdaq, and even Bitcoin erased most, if not all, of Monday’s declines. This morning, risk assets continued to move higher as the S&P 500 and Nasdaq both look to open 0.2% higher while Bitcoin tests $93K. Gold and other metals are also up 0.5% to 1%, and even crude oil is up 1% and back above $59 per barrel. Treasury yields are also moving lower for the second day in a row, with the 10-year yield back down to 4.06%.

After being starved of economic data for several weeks, this morning we’ll get ADP Employment and PMI readings for the services sector, both current reports. In addition, the backlog of data will continue to ease as September reports covering Import Prices (8:30), Industrial Production (9:15), and Capacity Utilization (9:15) will also hit the tape.

In Asia overnight, the Nikkei rallied over 1% as Hong Kong fell 1% while South Korea added on another 1.0% after Q3 GDP came in higher than expected (1.3% vs 1.2% q/q). In Europe, the picture is more muted as the STOXX 600 gains 0.2%, and the only other countries moving up or down 0.2% or more are Italy (+0.5%) and Spain (+1.5%). Europe’s gains come as PMI reading for the services sector generally surprised to the upside. The only exception was Spain, which ironically is also the country with the largest gain on the day so far.

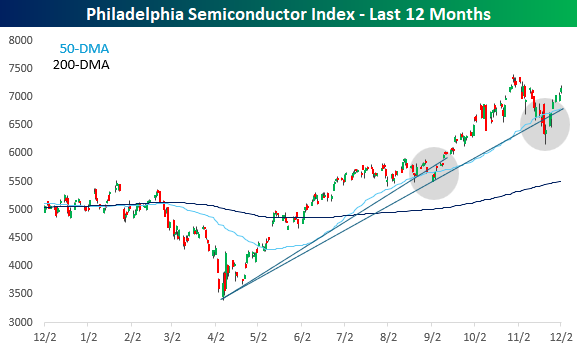

In last night’s Closer, we highlighted multiple equity baskets, which shed some light on how the economy is doing, and their performance is especially important given the lack of official economic data. Another index we follow closely as a gauge of the economy is semiconductors, which, many years ago, we branded the transports of the 21st century. When semis rally and outperform the market, it usually serves as a confirmation of a rally in the broader market and economy. Conversely, when semis falter and underperform, it serves as a red flag.

As shown in the chart below, the Philadelphia Semiconductor Index (SOX) has performed extremely well since the April low. In retrospect, it’s been a smooth ride higher, although there were two speed bumps – in September and just recently – where the trend higher and the 50-DMA was briefly violated. In the moment, both pullbacks felt concerning, but as semis recovered, the selloffs were chalked up to consolidation. The SOX isn’t out of the woods yet, but through yesterday’s close, it was less than 3% from a new high.

On a relative strength basis, semis have also bounced back nicely. In late October and early November, the relative strength of the SOX briefly made a new high, and now just seven trading days after the recent low, it’s back within a 3% range of that high.

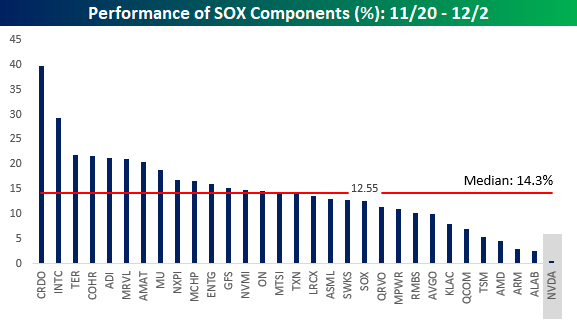

What really stands out about the rally in the SOX off the closing low on 11/20 is the breadth. Since the low, every stock in the index has traded higher, and the median gain has been 14.3%. What’s most impressive, though, is that Nvidia (NVDA) has sat out the rally with a gain of just 0.45% making it the worst-performing stock in the index. NVDA is the largest stock in both the SOX (by a wide margin) and the S&P 500, and during a period when it has essentially been flat, the two indices rallied 12.55% and 4.44%, respectively. It looks like the market can, in fact, rally without NVDA.